ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 26, 2020 | Bad Dog

Garth Turner

There was panic in the PR department over at Re/Max and Royal LePage last week. They might even had a picture of bad dog Evan Siddall on the wall, with a few bullet holes in it. (Okay, dart punctures, maybe.)

Used to be that the fed agency, CMHC, was just a big squishy, real estate-friendly fluffy media puppy for the major property floggers. For decades the people running it were industry veterans who saw their job as promoting housing. But no more. Mongrel Evan ended it all.

“Homeownership is like blood pressure,” he famously told MPs. “You can have too much of it.”

Yikes. Now everything changed. Says Re/Max spokesguy Chris Alexander: “A statement of this nature is panic-inducing and irresponsible.” In fact the company rushed out one of its famous ‘reports’ this week seeking to prove CMHC is full of fascists, malcontents, anarchists and yellow vesters who can no longer be trusted to make credible statements or forecasts. Like Re/Max.

What did Siddall do to inflame the realtors so?

He stated the obvious. We’re in a pandemic which is carving 30% from the economy, has swelled the jobless rate to 30%, put eight million people on the dole and could take a few years (if ever) to forget. Unemployed people living on pogey and unable to make rent or mortgage payments don’t buy houses, he said. Thus, there will be consequences. And he listed these:

- Household debt, now at 99% of the economy, will swell to 130% – enough to torpedo growth and job creation.

- Property values across the country could drop by up to 18%.

- A ‘deferral cliff’ is coming in September when mortgage payments have to resume and yet joblessness is still rampant, This is serious because…

- …by September 20% of all mortgage households will not be able (or willing) to pay their home loans.

So the CMHC boss indicated he’d be suggesting to the Trudeau gang that the minimum down payment be doubled to 10% and other lending practices be modified to reduce demand for homes and spare new buyers from falling into a trap. “We feel we need to avoid exposing young people to the amplified losses that result from falling house prices. Unless we act, a first time homebuyer purchasing a $300,000 home with a 5% down payment stands to lose over $45,000 on their $15,000 investment if prices fall by 10%.”

Poop, says Re/Max. Prices will not fall since, “sellers simply won’t accept that kind of discount on their listings.”

“CMHC doesn’t seem to understand the sheer number of sellers that would have to accept this kind of price reduction, in order for average housing prices to plummet to this degree in such a short time span.”

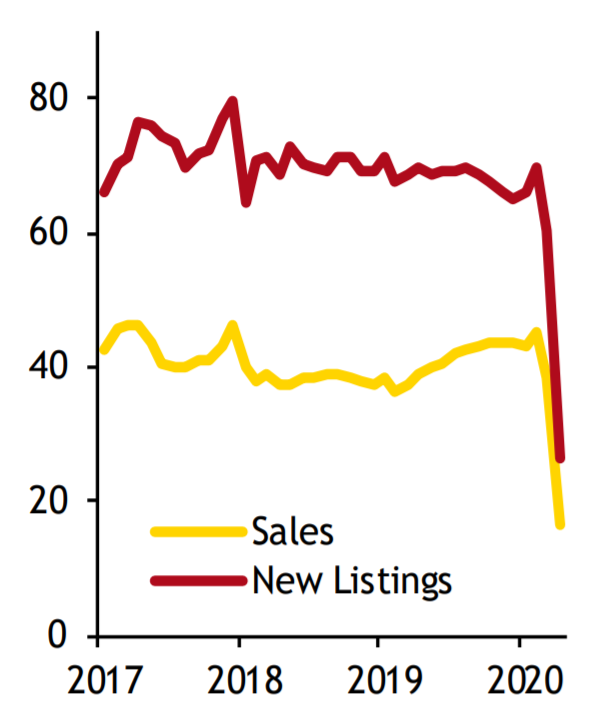

The company says there’s zero evidence of a declines in Toronto, for example, where multiple bids continue, demand is high, and offers continue to be made despite social distancing and the terrifying sight of realtors in pale blue spandex. So while sales activity has plunged by about 70%, prices have held firm. Thus, Re/Max concludes, it only gets better from here. Now Shaun Cathcart, senior economist at CREA, the national real estate outfit, agrees. Uppa, uppa.

Not so fast. Sales may have fallen, but so have listings – dramatically. Last April there were 17,600 new offerings in Toronto, and this year that crashed to 6,100. So fewer buyers were chasing diminished supply, which is why prices have held steady – despite a sick economy and galloping unemployment. What Siddall is saying is simple. Expect a change. When mortgage deferrals end (and people are still out of work) there could be a tsunami of new listings as indebted families bail.

And let’s not forget the Airbnb factor. When the pandemic came to town there were more than 21,000 short-term rentals in the GTA alone, a lot of them condos bought for exactly that purpose. No more. That business has collapsed. The company has spent $250 million to offset the losses of hosts due to a barrage of cancelations, cancelled its IPO and laid off a third of its staff. Just peruse the condo listings, and you can see the extent of the carnage. Many more of these ghost hotel units will be coming on stream as the year progresses.

There ya go. Logic says housing will be infected by the virus. But along comes new evidence showing sales in the first half of May were much stronger than the month before, even as the job situation deteriorated. So could it be that Re/Max logic will win? Are there enough greater fools roaming the streets to keep real estate alive until a vaccine arrives?

As always, buy a house if you need one and can afford it without gutting your finances, jeopardizing your retirement and family or enslaving you to debt. Alternatively, you can invest in rising financial assets, collect your CERB, rent a beautiful place for peanuts and stop paying your landlord. Tough choice.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Garth Turner May 26th, 2020

Posted In: The Greater Fool