ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

April 6, 2021 | Bank of Canada Now Owns 40% of Government of Canada Bonds. Fed a Saint in Comparison. Taper on the Table

Wolf Richter

The Economics and Strategy shop at the National Bank of Canada, the country’s sixth largest bank, sent a missive to clients today that would be hilarious if it weren’t pointing at such a serious and massive issue: It celebrated “40,” referencing a 40th birthday, but instead of a birthday, it referred to the Bank of Canada’s ballooning holdings of Government of Canada (GoC) bonds, which will hit a stunning 40% of all GoC bonds outstanding this Friday.

By comparison, the Fed holds 17.6% of all Treasury securities outstanding: It holds $4.94 trillion in Treasury securities, of $28.1 Trillion outstanding. We – that’s the universal “we,” meaning “a few of us” – complain about the Fed’s crazy buying of Treasury securities and all the distortion and craziness this causes. But compared to the Bank of Canada, the Fed looks like a saint.

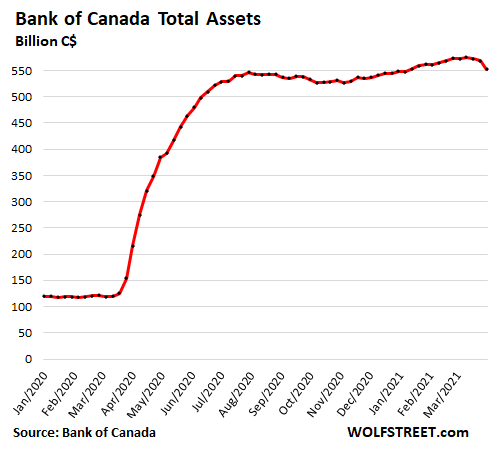

The Bank of Canada announced a couple of weeks ago, citing “moral hazard” associated with its central bank nuttiness, that it would unwind its crisis liquidity facilities, and that this would reduce its total assets by about C$100 billion, or by about 17%, from C$575 billion at the time, to C$475 billion by the end of April. In October, it had started a mini-tapering of its purchases of GoC bonds and is jabbering about tapering its GoC bond purchases further. And its total assets have started to drop over the past two weeks:

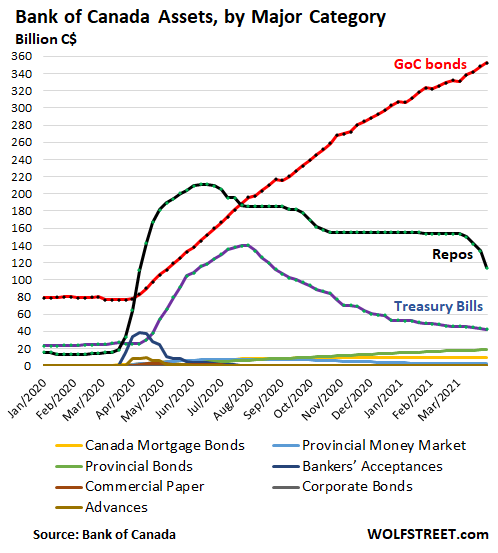

Its total assets are dropping because it is unwinding its liquidity facilities, including its term repos that are now maturing one after the other and rolling off the balance sheet without replacement (black line), and short-term Government of Canada Treasury bills that are also maturing and rolling off the balance sheet without replacement (purple line).

But it has continued adding to its pile of GoC bonds (red line), though at a slightly slower pace since October. The remaining asset categories – the colorful spaghetti at the bottom of the chart – have mostly been unwound or are minuscule. These GoC bonds are going to be the main issue going forward:

So here are Chief Rates and Public Sector Strategist Warren Lovely and Rates Strategist Taylor Schleich at Economics and Strategy at the National Bank of Canada in their note [comments in brackets are mine]:

“With the settlement of its latest tranche of Government of Canada bond purchases, the Bank of Canada today (April 6th) owns precisely C$343.8 billion of GoC bonds. At this moment, there are C$862.1 billion of domestic Canada bonds floating around, which means the BoC ownership share is now within a hair’s breadth of 40%. That psychological threshold looks to be technically breached Friday, April 9th.

“So this is 40, and we thought it appropriate to mark the milestone. We’re not really celebrating mind you, but that’s what tends to happen when your age (or in this case bond ownership share) gets elevated. So put the streamers and balloons away. [The authors added this image].

“Actually, it makes you wonder if there’s a potential mid-QE-life crisis taking shape in Ottawa. As in, when, where and how quickly to taper outsized bond purchases? How much unconventional support does the economy still need? How badly are bond purchases distorting the market? When and how fast will the Fed be tapering?

“These are but a few questions Tiff [BoC governor Richard Tiffany “Tiff” Macklem] and Company are presumably pondering.

“It’s taken just one year to radically transform GoC bond ownership. Pre-COVID, the central bank held a fairly constant ~13% of outstandings, a position accumulated via less-than-invasive/normal course auction participation.

“But since setting up its GBPP, BoC ownership has all-but-raced through key ownership milestones, surpassing 20% last May, breaching 30% last September and arriving this week at 40%.

“Of note, an October 2020 QE taper (from C$5 billion to C$4 billion per week), slowed but did not arrest the crowding out effect in the GoC bond market.

“With more and more term repos now rolling off, GoC bonds account for a larger share of total BoC assets (62% and rising).

“Looked at another way, central bank purchases offset 95% of what was overwhelmingly record net GoC bond issuance in the just completed 2020-21 fiscal year—an absorption rate that’s really hard to overemphasize.” [meaning, in the fiscal year, the BoC has monetized 95% of net issuance of GoC bonds; one of the resulting distortions is Canada’s spectacular house-price inflation].

“Strip out RRBs [inflation-adjusted Real Return Bonds], where the Bank owns less than 5%, and our central bank actually blew through 40% ownership of nominals some time ago.

“With issuance set to moderate, additional tapering moves (plural) are needed to halt the increase in BoC ownership.

“The way we see it, steady reductions in QE could cap the BoC’s share at just under 45%. The BoC has an opportunity to do what most people desire but are not physically capable of: stopping the clock. So after turning 40 on Friday, here’s hoping that’s the last major BoC milestone we need to recognize.”

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter April 6th, 2021

Posted In: Wolf Street

Next: What Gives Value to a Currency? »