ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

March 15, 2024 | Banks are Fighting Proposals for Tougher Regulatory Rules

Hilliard MacBeth

A battle is underway in the U.S. over new rules requiring higher equity capital for the banks. Enhanced equity capital protects the bank from insolvency in the event of a financial crisis.

Bank lobbyists are fighting hard to keep capital requirements at the lowest possible level while regulators would like higher capital given the historical record of bank failures in 2009 and 2023.

Will the lobbyists who toil in Washington, D.C., for the banks win the fight to avoid higher equity minimums?

There was a consensus among regulators and the public after 2009 that requirements for a minimum amount of equity capital were too weak, given the dozens of bank bailouts after the financial crisis. Then in March 2023 we saw more bank failures and in 2024 there is another bank in trouble, New York Community Bank, where the share price has fallen about 70 percent since January.

The Federal Reserve proposed in mid-2023 that minimum equity requirements would be increased by 20 percent. Lobbyists immediately shifted into high gear in badgering 535 members of Congress (there are 486 lobbyists) to get those proposals watered down so banks could continue to operate with the least amount of equity capital possible.

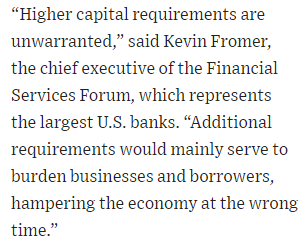

In the Wall Street Journal June 5, 2023, when the rule change was first proposed, a lobbyist replied:

This is the most quoted talking point from the industry; that higher equity requirements would hurt borrowers.

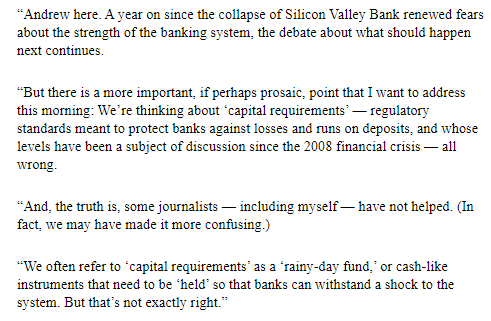

But one media personality admitted that he had misled them about bank capital:

Andrew Ross Sorkin, author of “Too Big to Fail” a top-selling book about the financial crisis in 2009, co-host of CNBC Squawk Box since 2011.

Stanford professor Anat R. Admati, co-author of “The Bankers’ New Clothes: What is wrong with Banking and What to do about It” tried to explain the benefits of higher minimum equity capital in a letter to the Federal Reserve with copies to the FDIC and the Office of the Comptroller of the Currency.

Enhanced capital as common equity has many benefits to the public, customers, and the resilience of the system. The more common equity capital the better it is for almost everyone. Admati argues that even shareholders are better off. And equity capital is not “held” as a “rainy day fund”.

But banks like a measure called “Return on Equity” (ROE). ROE is a ratio of profits or return (R) to equity (E). And the higher the E, the lower the ROE. More equity means a higher E, which hurts ROE but makes the bank stronger.

So, banks try to keep E small by paying out dividends to shareholders unless they are stopped by the regulators. Alternatively, equity can be increased by paying smaller dividends or by issuing more shares which would strengthen the bank’s balance sheet. But bankers hate to do that unless forced to by the regulator.

So, expect lobbyists to get the rules weakened so that banks can continue to operate with minimum equity on the balance sheet.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson Wealth is a member of Canadian Investor Protection Fund. Richardson Wealth is a trademark by its respective owners used under license by Richardson Wealth.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Hilliard MacBeth March 15th, 2024

Posted In: Hilliard's Weekend Notebook

Next: Soul of a Nation »