The year 2023 was supposed to be the year of the recession. It was the most anticipated recession ever, the most hoped-for recession. Starting in 2022 with the initial rate hikes, the “Leading Economic Index” predicted a recession for late 2022; and when that didn’t come, for early 2023; and when that didn’t come, for mid-2023, and then late 2023, and then early 2024… (we’ve shredded the LEI’s predictions here). A year ago, even the Fed staff predicted a recession for late 2023. You get the drift: the Recession that Didn’t Come.

It didn’t come because our Drunken Sailors got together and partied – consumers, governments, and even businesses. They didn’t want to have any part of this recession.

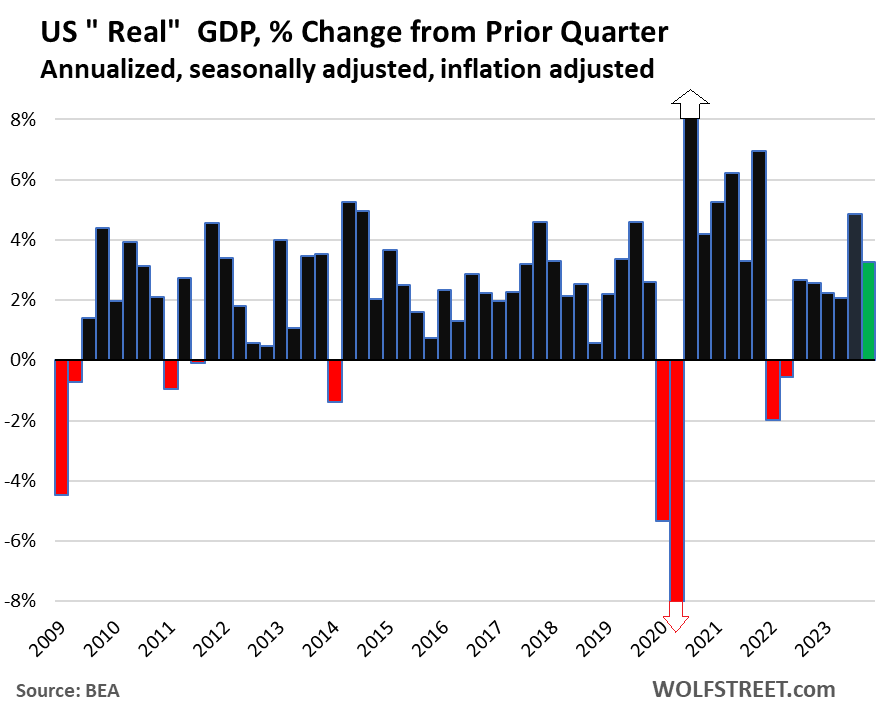

“Real GDP” in Q4 (adjusted for inflation via 2017 dollars) jumped by an annualized rate of 3.3% from Q3, after the 4.9% jump in Q3, according to the Bureau of Economic Analysis today.

All major categories pulled in the right direction (adjusted for inflation):

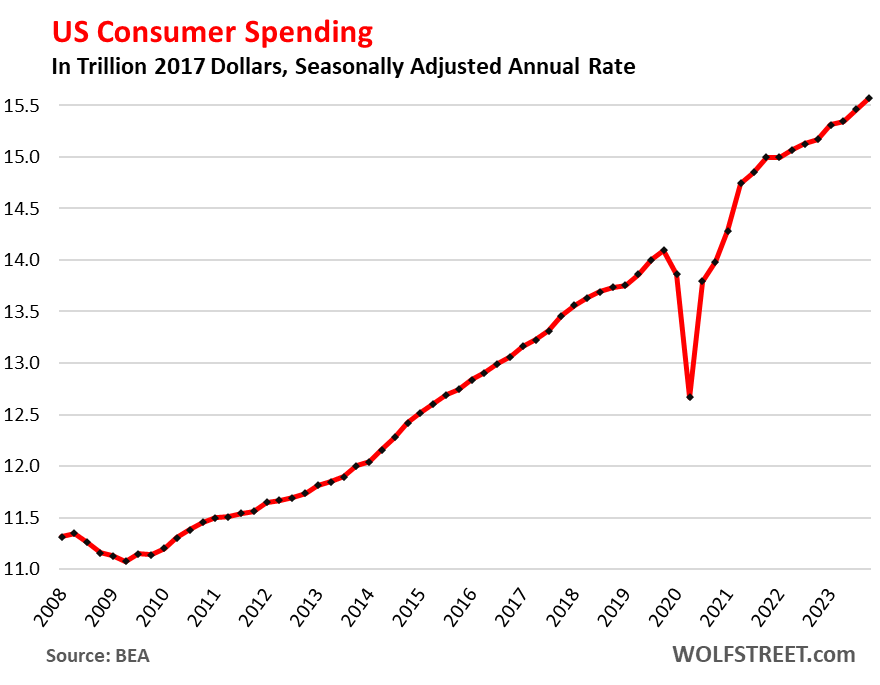

- Consumer spending (69% of GDP): +2.8%.

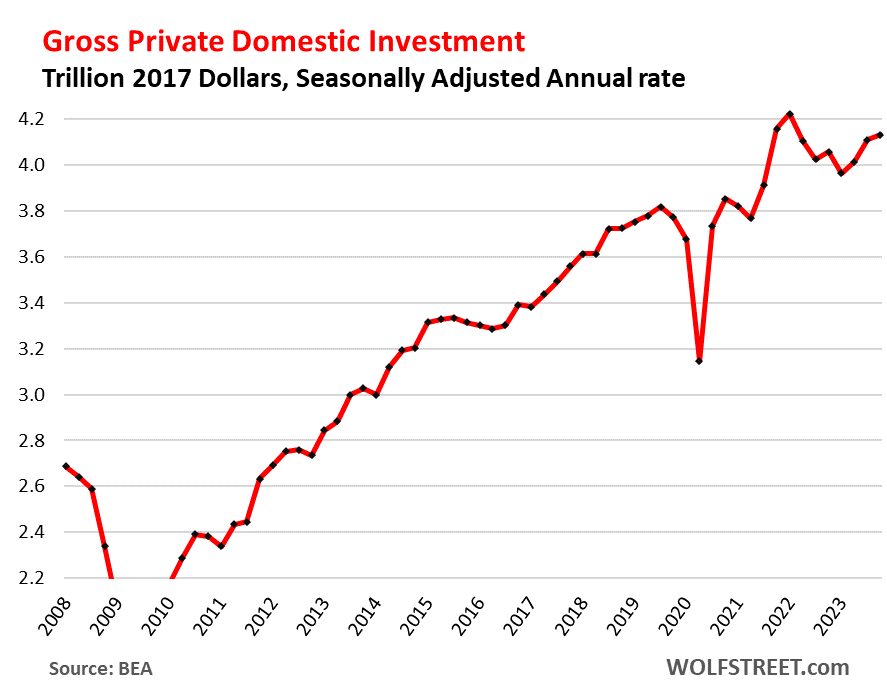

- Gross private investment (18% of GDP): +2.1%.

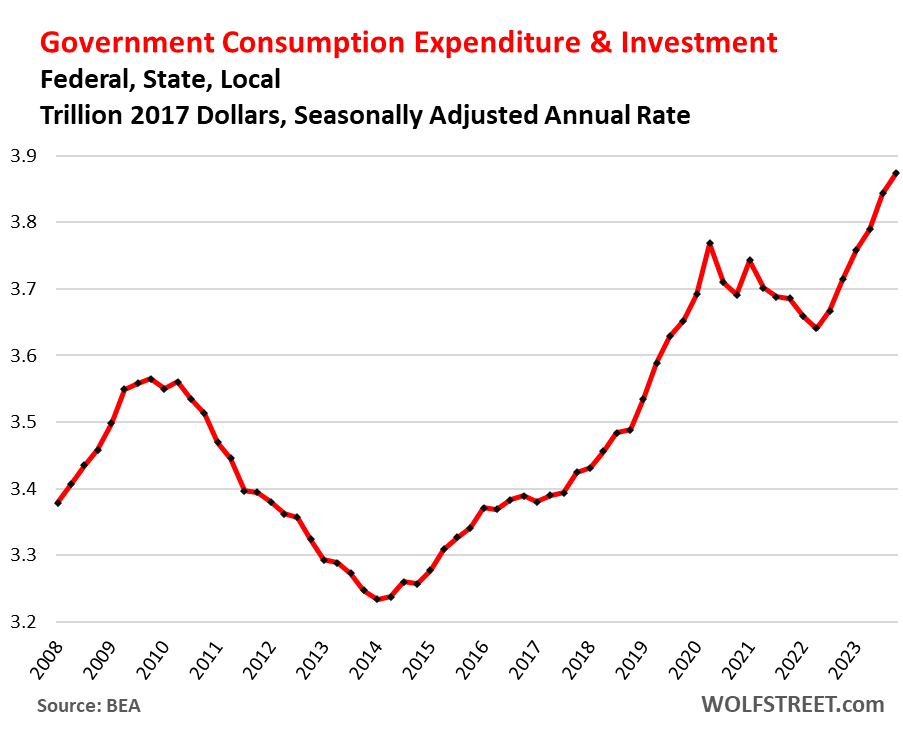

- Government consumption and investment (17% of GDP): +3.3%.

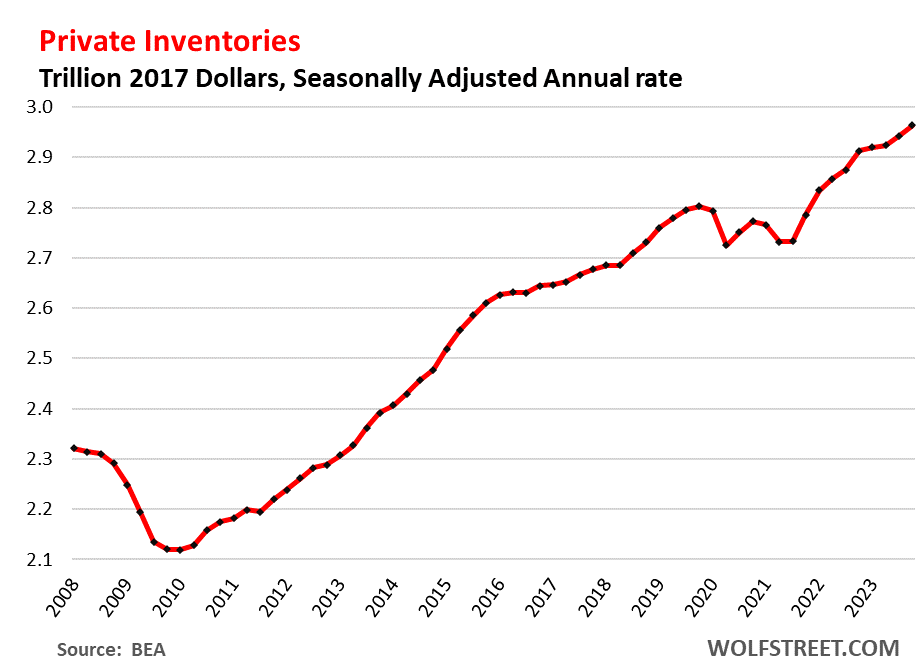

- Private inventory investment increased faster and added to GDP.

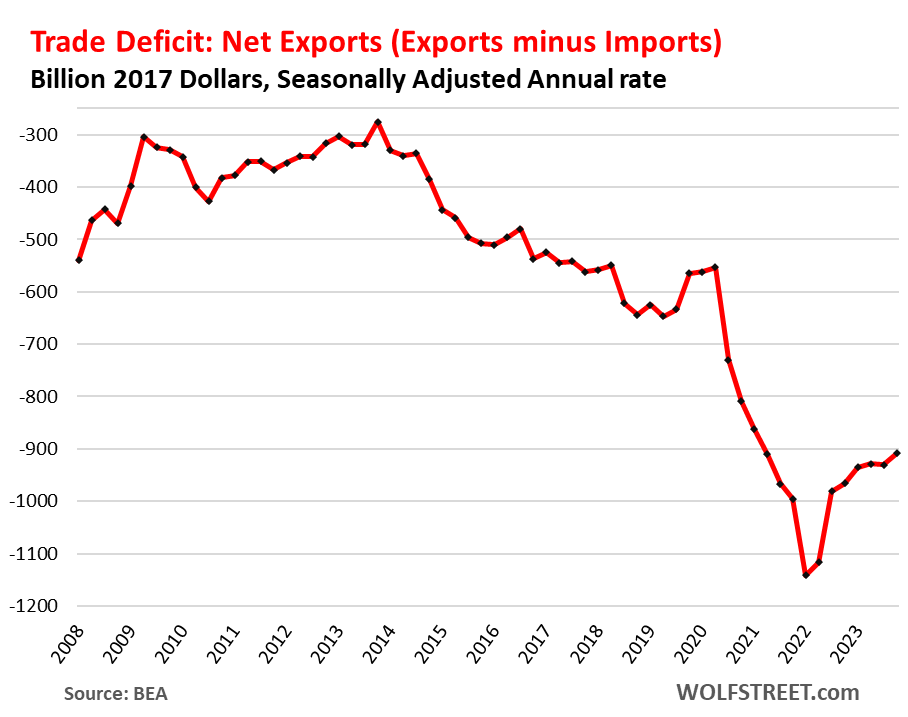

- The trade deficit (“net exports”) got less horrible and was a smaller drag on GDP.

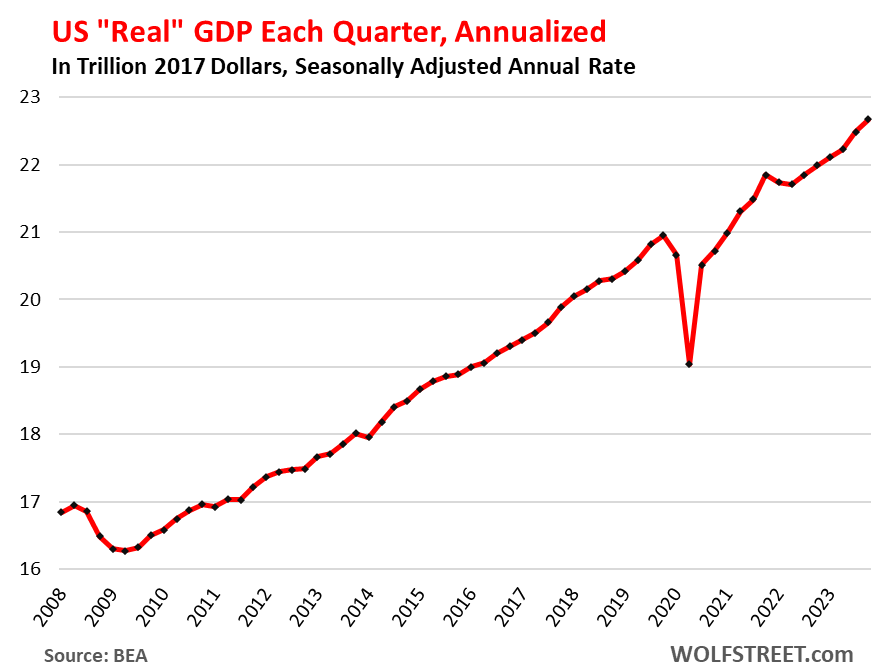

“Real” GDP in dollar terms, adjusted for inflation and expressed in 2017 dollars, was $22.7 trillion annualized.

“Current-dollar” GDP (“nominal” GDP, not adjusted for inflation and expressed in current dollars) jumped by 4.8%, to $27.9 trillion annualized. This $27.9 trillion represents the actual size of the US economy, measured in today’s dollars.

Annual “real” GDP (adjusted for inflation) grew by 2.5% in 2023, right in the range before the pandemic and a tad above the 10-year average before the pandemic (2.3%):

Consumer spending on goods and services rose by 2.8% in Q4 from Q3, annualized and adjusted for inflation.

- Spending on goods rose by 3.8%, including 4.6% for durable goods, which we’ve seen in the surge in motor vehicle sales).

- Spending on services rose by 2.4%.

Gross private domestic investment rose by 2.1%, after the 10% spike in Q3. Of which:

Fixed investment (part of gross private domestic investment): +1.7%, of which:

- Residential fixed investment: +1.1%.

- Nonresidential fixed investments: +1.9%:

- Structures: +3.2%.

- Equipment: -+1.0%%.

- Intellectual property products (software, movies, etc.): +2.1%.

Government consumption and investment rose by 3.3%, the sixth quarter in a row of steep increases. This does not include transfer payments and other direct payments to consumers (stimulus payments, unemployment payments, Social Security payments, etc.), which are counted in GDP when consumers and businesses spend or invest these funds.

The most reckless drunken sailor, the federal government, is blowing vast sums in every direction, relentlessly running up gigantic deficits and piling them on its $34 trillion mountain of debt.

- Federal government: +2.5% (national defense +0.9%, nondefense +4.6%), on top of the 7.1% spike in Q3

- State and local governments: +3.7%.

The Trade Deficit (“net exports”) in goods & services got a little less horrible:

- Exports: +6.3%.

- Imports: +1.9%.

Exports add to GDP. Imports subtract from GDP. Exports are much smaller in dollars than imports (hence the trade deficit, or negative “net exports”).

The stimulus-driven buying binge of goods in the US during the pandemic and the lack of foreign tourism during the travel bans (considered “exports” as money from foreign sources is paid to US businesses) caused the trade deficit to totally blow out. It has since recovered some, but remains far worse than in 2019:

Change in private inventories added 0.07 percentage points to GDP growth. Increases in inventories count as a business investment. Inventories rose by 2.8% annualized in Q4 from Q3. This growth rate was a hair faster than the growth rate in Q3 from Q2 (+2.7%), hence a small contribution to GDP growth. Note the period of inventory shortages during the pandemic.

So in 2023, all our drunken sailors – especially consumers and governments – did their part to keep the spending party going. The recession watch for 2023 is over. The recession didn’t come. Now the recession watch is on for 2024, and recessions are already being predicted to start ASAP.