ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 3, 2023 | Powell Swats Down Rate Cut in 2023, Purposefully Leaves in Doubt a “Pause” for June Meeting

Wolf Richter

Fed chair Powell was bombarded by essentially the same question over and over again today during the press conference after the FOMC hiked its policy rates to 5.25% at the top of the range. Reporters were trying to nail him down: Has a decision been made about “pausing” the rate hikes in June? And he was asked if there will be “rate cuts” this year?

Over and over again, he refused to lock in a pause for the June meeting – “A decision on a pause was not made today,” he started out with. Over and over again, he said that a pause would depend on the incoming data.

And he brushed off the rate-cut question – “If our forecast is broadly right, it would not be appropriate to cut rates; we won’t cut rates,” he said.

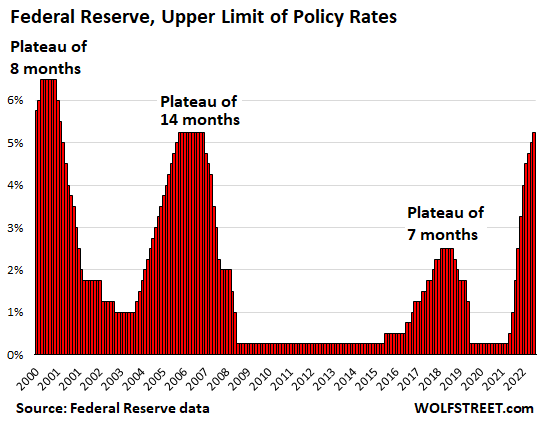

Timing for a rate cut this year is getting tight. First comes the pause, and then, later, comes the rate cut. Over the past 22 years – the prior three tightening cycles – the pauses lasted between seven months (2019) and 14 months (2006-2007). If the Fed pauses the rate hikes in June, there are only six months left in the year.

But this time, the tightening cycle is dealing with the worst bout of inflation in 40 years. And Powell has once again expressed the Fed’s leeriness about inflation’s nasty habit of resurging: “We have seen inflation come down and move back up two or three times since March of 2021,” he said. And in this inflationary environment, a rate cut just isn’t appropriate, he said.

Here are the prior three tightening cycles and their plateaus. If the Fed pauses in June and does one rate cut before year-end, it would be the quickest rate cut of any of them, in the most inflationary environment of all of them:

What Powell said about a “pause” in June.

“A decision on a pause was not made today. You will notice in the statement for March we had a sentence that said ‘the committee anticipates that some additional policy firming may be appropriate.’ That sentence is not in the statement anymore. We took that out. Instead we are saying that ‘in determining the extent to which additional policy firming may be appropriate,’ the committee will take in to account certain factors. So that’s a meaningful change that we we’re no longer saying that we ‘anticipate.’ And so we will be driven by incoming data meeting by meeting and we will approach that question at the June meeting.”

“The assessment of the extent to which additional policy firming may be appropriate is going to be an ongoing one, meeting by meeting. And we’re going to be looking at the factors that I mentioned that are listed in the statement, the obvious factors. That’s the way we’re going to be thinking about it.”

“There is a sense that we’re much closer to the end of this than to the beginning. If you add up all the tightening that’s going on through various channels, we feel like we’re getting close or maybe even there. But then again that’s going to be an ongoing assessment. And we’re going to be looking at those factors that we listed to determine whether there is more to do.”

Why it was necessary to raise rates today...

“With our monetary policy, we’re trying to reach and then stay for an extended period at a policy stance that’s sufficiently restrictive to bring inflation down 2% over time. That’s what we are trying to do with our tool. I think slowing down was the right move. I think it has enabled us to see more data, and it will continue to do so.

“We always have to balance the risk of not doing enough, and not getting inflation under control against the risk of maybe slowing down economic activity too much. And we thought that this rate hike along with the meaningful change in our policy statement was the right way to balance that.

“We have seen inflation come down and move back up two or three times since March of 2021. So I think you’re going to want to see that a few months of data will persuade you that you have got this right.”

Markets are pricing in rate cuts by year-end. Do you rule that out?

“So we on the committee have a view that inflation is going to come down not so quickly. It will take some time. And in that world, if that forecast is broadly right, it would not be appropriate to cut rates; we won’t cut rates.

“If you have a different forecast, and markets have from time to time been pricing in quite rapid reductions in inflation, we would factor that. But that’s not our forecast.

“If you look at non-housing services, inflation really hasn’t moved much. It’s quite stable. And so we think demand will have to weaken a little bit, and labor market conditions will have to soften a bit more, to begin to see progress there. In that world it wouldn’t be appropriate for us to cut rates.”

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter May 3rd, 2023

Posted In: Wolf Street