Hoisington’s First Quarter 2024 Review and Outlook is available here. Always a rich and enlightening economic lesson.

For those who think the impacts of the 2022-23 monetary tightening cycle are over, this concise review is worth a look.

U.S. dollar world liquidity (MWDL) dropped by a record 9% year over year in February as the U.S. Fed’s monetary restraint intensified globally. A deceleration of this nature preceded every recession since 1976.

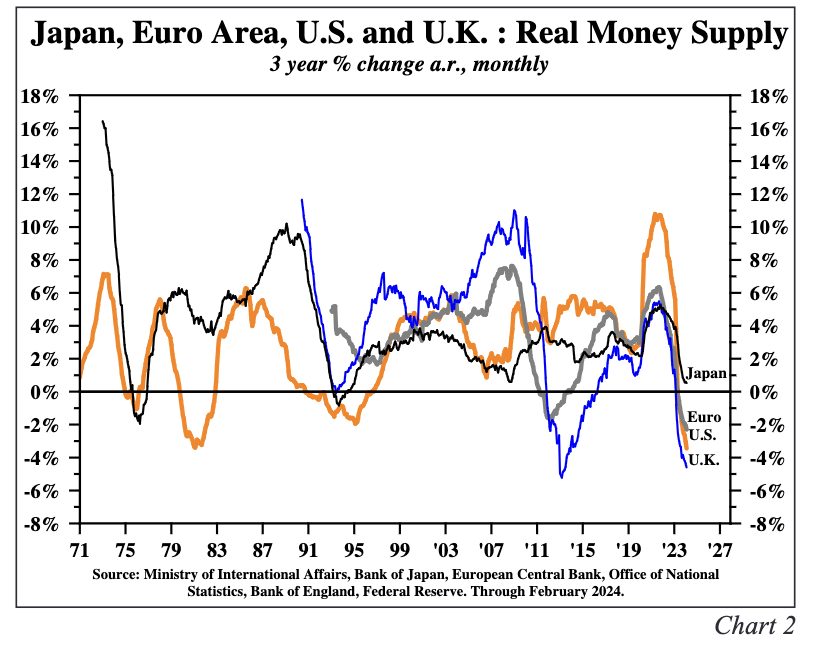

For the first time since at least 1970, the three-year percentage change in real monthly money supply is negative in the Euro area, the U.S., and the U.K., while Japan is experiencing the slowest growth in 12 years (Chart below) and China is in deflation.

High debt levels and negative Net National Savings (NNS) are reducing rather than boosting economic growth prospects from here:

The contractionary effects of monetary policy and the de-facto negative NNS policy stance of fiscal policy will serve to place increasing downward pressure on inflation and growth.

A sharp 7% rate of decline in vehicle sales in the first quarter is a sign that the deflationary trend in big-ticket consumer goods prices is more likely to gather speed than reverse. The inflation rate will likely undershoot the Fed’s target, and the unemployment rate will move higher than anticipated by the Fed. Inflation and unemployment are lagging indicators, and much of their cyclicality occurs after, not before, recessions end. This declining inflation environment will continue to bring down inflationary expectations and long-term Treasury bond yields.