ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

April 7, 2024 | Bank of Canada Balance Sheet QT Sheds 64% of Pandemic QE Assets, Indicates QT Might End in September 2025

Wolf Richter

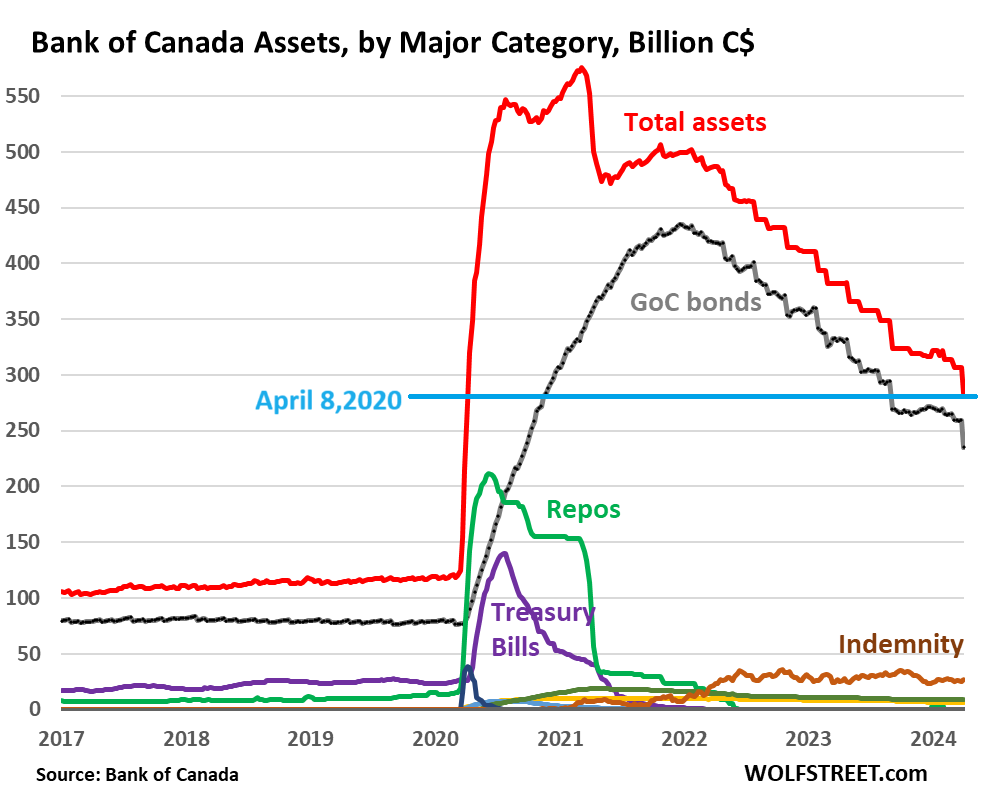

The Bank of Canada, in its quantitative tightening program, does not cap the roll-off. Whenever Government of Canada bonds in its portfolio mature, the BoC gets paid for them at face value and doesn’t replace them. That’s the roll-off. There are months when nothing in the BoC’s portfolio matures, and there are months when a big bond issue matures. GoC bonds mature on the first day of the month. There were no maturities in December and January; $3.6 billion matured on February 1; $6.6 billion matured on March 1, and on April 1, $23.3 billion matured.

So, in latest weekly balance sheet, released Friday afternoon, total assets dropped by $23.3 billion, to $283.5 billion, the lowest since April 8, 2020.

In terms of pandemic QE: -64%. The BoC has now shed 64% of the assets it had loaded up during pandemic QE (gray line). In terms of GoC bonds alone, the BoC has shed 56% of the GoC bonds it had added during pandemic QE. The BoC already shed its entire pandemic holdings of Canadian Treasury bills (purple) and repos (green).

“Indemnity” of $26.9 billion (brown in the chart above) is the value of the indemnity agreements between the federal government and the BoC that represents the unrealized losses on the bond holdings, if the BoC ever sold the bonds outright today at today’s market prices.

The BoC and the government have a deal that requires the government to reimburse (indemnify) the BoC for those losses on the GoC bonds, if the BoC actually sells those bonds and thereby realizes the losses. But if the BoC holds them to maturity, it will get paid face value, and those losses vanish.

The BoC doesn’t sell bonds, but sheds them when they mature, which is when the BoC gets paid face value for them. So as the remaining bonds mature over the years, this “indemnity” account will slowly go to zero.

What QT looks like going forward:

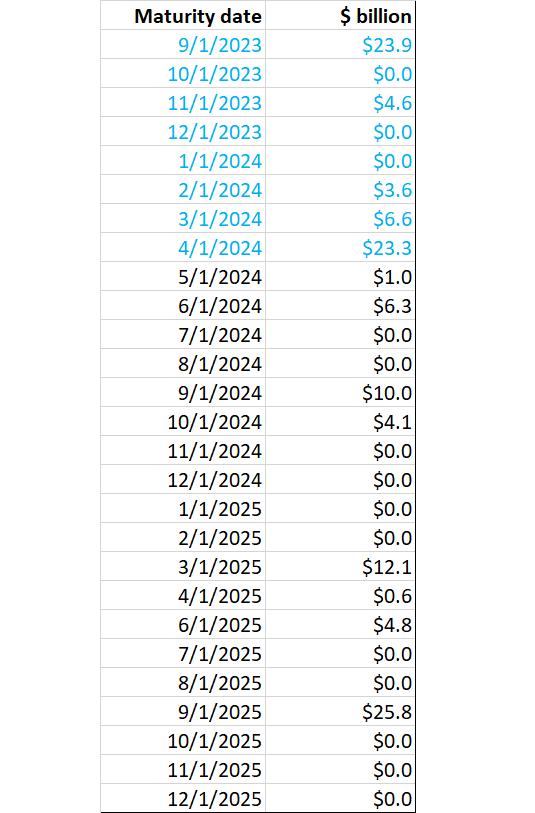

Below is the maturity schedule of the BoC’s holdings of GoC bonds. For illustration purposes, we have included the last 8 months (blue figures); those bonds are already gone.

The future maturities in GoC bonds through 2025 (black figures) amount to $65 billion at face value. The last maturity in 2025 is on September 1. There are no maturities in October, November, and December 2025. In other words, if QT continues through September 1, 2025, another $65 billion in GoC bonds will roll off. We’ll get to that in a moment because the Bank of Canada has started discussing it.

When will the Bank of Canada’s QT end and what will come afterwards?

The Fed has also started talking about this issue of how low the balance sheet might go – withdrawing liquidity can get very tricky because liquidity doesn’t always smoothly and quickly flow to where it’s needed, and that could turn into a mess – and we dove into it most recently here: The Fed’s Liabilities: How Far Can QT Go? What’s the Lowest Possible Level of the Balance Sheet without Blowing Stuff Up?

During QE, a balance sheet level is driven by assets that the central bank purchases in large quantities, and liabilities come up in equal measure (always: assets = liabilities + capital). If assets go up, liabilities must go up in equal measure.

During QT, when a central bank sheds assets, liabilities must decline in equal measure.

The BoC’s big three liabilities.

Bank notes: The largest liability during normal times is currency in circulation (“bank notes in circulation,” as the BoC calls them), and they’re demand driven. When you withdraw $500 from an ATM, you expect the ATM to have the $500, and it’s the banking system’s job to get enough bank notes from the central bank and have them ready for customers.

The BoC has a liability of $115 billion for bank notes in circulation, which have continued to grow over the years. And they’re market driven.

Government deposits. The BoC is also the checking account provider for the government of Canada, and the deposits of the government are determined by the government, not the BoC. The deposits currently amount to $32 billion.

So already, there are $147 billion in liabilities that the BoC does not control. And they must be balanced with $147 billion in assets.

Bank settlement balances. The other large liability represents cash that banks put on deposit at the Bank of Canada, $127 billion on the current balance sheet. But two weeks earlier, they’d been at $105 billion. They have fluctuated in that range for months.

Settlement balances are similar to the “reserves” at the Fed. They represent liquidity in the banking system. Banks use these settlement balances to pay each other via the BoC. And they use them to keep extra liquidity at the BoC.

Settlement balances ballooned during QE and are now shrinking during QT. If they shrink too far under the current setup, the banking system and the broader financial system may run into liquidity issues.

Other liabilities. The BoC has some other liabilities, including reverse repos, but the amounts are small.

Settlement balances determine when QT ends: September 2025?

Deputy governor Toni Gravelle outlined this process on March 21. In his speech, he said: “The right amount of settlement balances to supply the system is uncertain. The bottom line is we will lean toward holding them at the minimum level needed to effectively implement monetary policy in a floor system.”

So what’s that minimum level? He said the BoC expects settlement balances “to land in a range of $20 billion to $60 billion.”

And he added: “But we are aware there is a risk that we could be wrong about the $20 billion to $60 billion range. There is uncertainty because it is fundamentally difficult to assess the demand for settlement balances.”

Settlement balances were $127 billion on the current balance sheet, but were $105 billion weeks earlier. And they fluctuate a lot. So we’ll go with the $105 billion. To get into the $20-billion to $60-billion range, they would have to drop by $45 billion to $85 billion.

Looking that the maturity schedule above, we see that the maturities through June 2025 amount to $39 billion, which wouldn’t get settlement balances into the range Gravelle indicated; it might only get them to $66 billion ($105 minus $39), a little above the range.

Then there are no maturities until September 1, when $25.8 billion mature, and that’s the last maturity of the year. So with the September maturities, the total maturities amount to $65 billion, which might get the settlement balances to $40 billion ($105 minus $65), smack-dab in the middle of the $20-$60 billion range that Gravelle proposed.

QT and rate cuts are separate. Gravelle re-pointed out that any rate cuts and QT (“balance sheet normalization”) are separate. The BoC can cut rates and continue “normalizing” its balance sheet until the desired settlement balances are reached. The Fed is on the same program, as is the ECB, which may cut in June and continue with its massive QT.

After QT ends, short-term T-bills and term repos will replace GoC bonds that will continue to run off over a “multi-year transition period.” The balance sheet will then grow as before QE, driven by the liabilities, but for the multi-year transition period, the composition will change with short-term T-bills and short-term repos (both are now zero) growing and replacing longer-term GoC bonds. There have been similar discussions to that effect at the Fed.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter April 7th, 2024

Posted In: Wolf Street