ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 9, 2024 | Our Drunken Sailors’ Credit Card Balances, Burden, Delinquencies, and Available Credit

Wolf Richter

Credit cards are a measure of spending, not a measure of borrowing; they’re the dominant consumer payments method in the US, having largely replaced checks and cash. They’re used to pay for anything, from bar tabs to business trips that get reimbursed – and those can be large amounts. Credit cards were used for $5.8 trillion in transactions in 2022, according to the Nilsen Report. The new data, when it comes out, will show that consumers ran over $6 trillion through their credit cards in 2023 – very little of it got stuck as interest-bearing debt; most of it was paid off by due date with no interest due. And that’s what we’re seeing here.

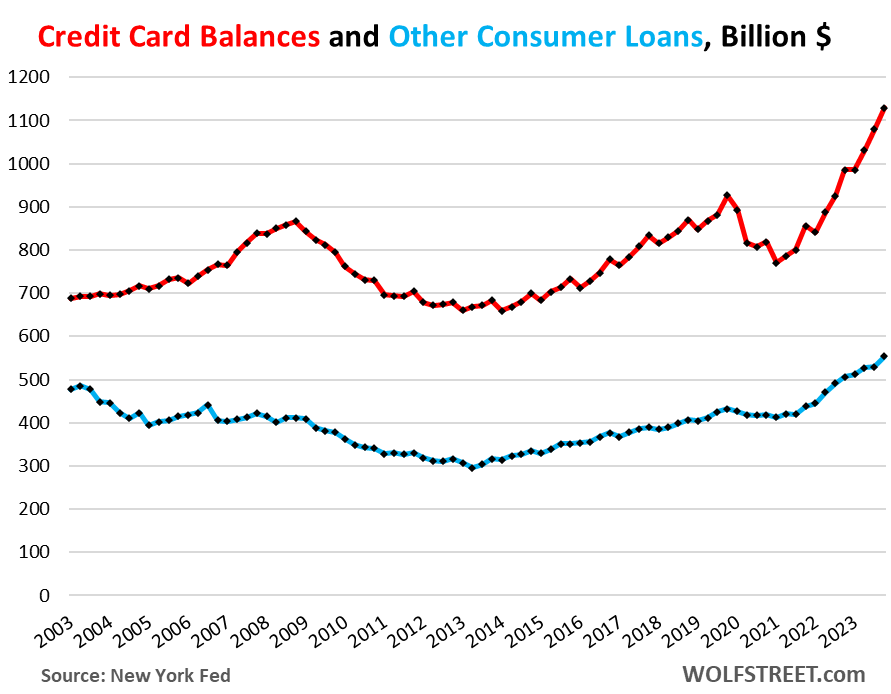

Credit card balances (red line in the chart below) – these are the statement balances before payments are made – rose by $50 billion in Q4 from Q3, to $1.13 trillion, according to the New York Fed’s Household Debt and Credit report. Year-over-year, credit card balances rose 14.3% on much higher spending on goods and services, including “revenge spending” on travels, restaurants, and entertainments – drunken sailors, we’ve come to call them lovingly and facetiously, but not so drunken because their income has risen even faster than their spending, and they were able to save a little.

“Other” consumer loans (blue line), such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, rose by $25 billion in Q4 from Q3, and by $47 billion, or 9.3% year-over-year. BNPL loans are short-term loans, subsidized by the merchant, that are interest-free for the customer; and the entire loan has to be paid off in four or five payments. They’ve been around forever; but they’ve gotten a lot more convenient. Note that balances have barely risen over the past 20 years, despite the growth of the population, income, and spending over the period:

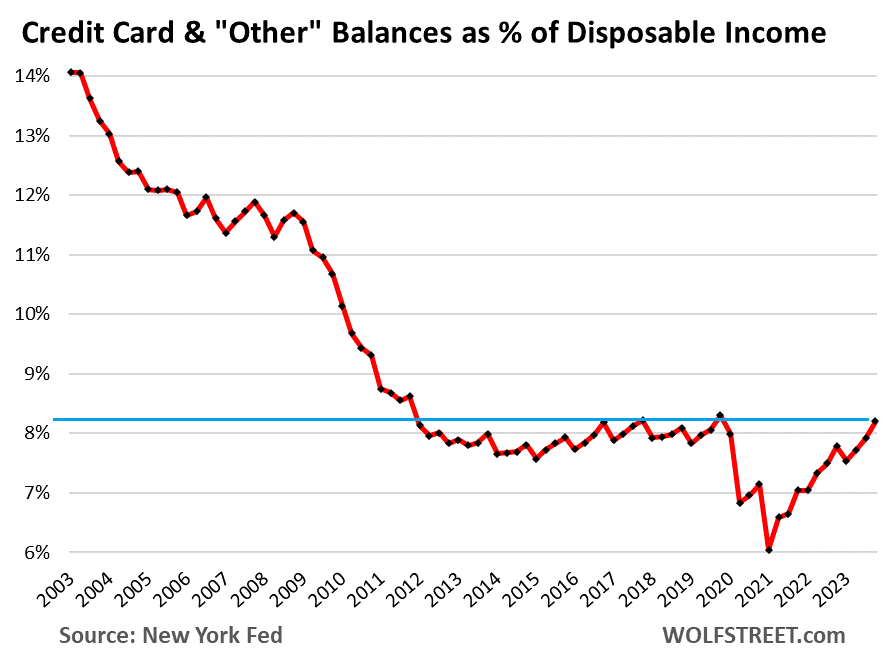

Credit-card balances to disposable income.

Credit card balances and “other” consumer debt combined, at $1.68 trillion, rose to 8.2% of disposable income (income from all sources except capital gains, minus taxes and social insurance payments; the income consumers have left over to spend).

This measure of the burden of credit card balances and other consumer loans, in relationship to disposable income, has come up from those free-money record lows and is in the range of the Good Times before the pandemic.

Note something else: 20 years ago, that ratio was 14%, and some consumers got in trouble with them during the Great Recession – it seems, some lessons were learned:

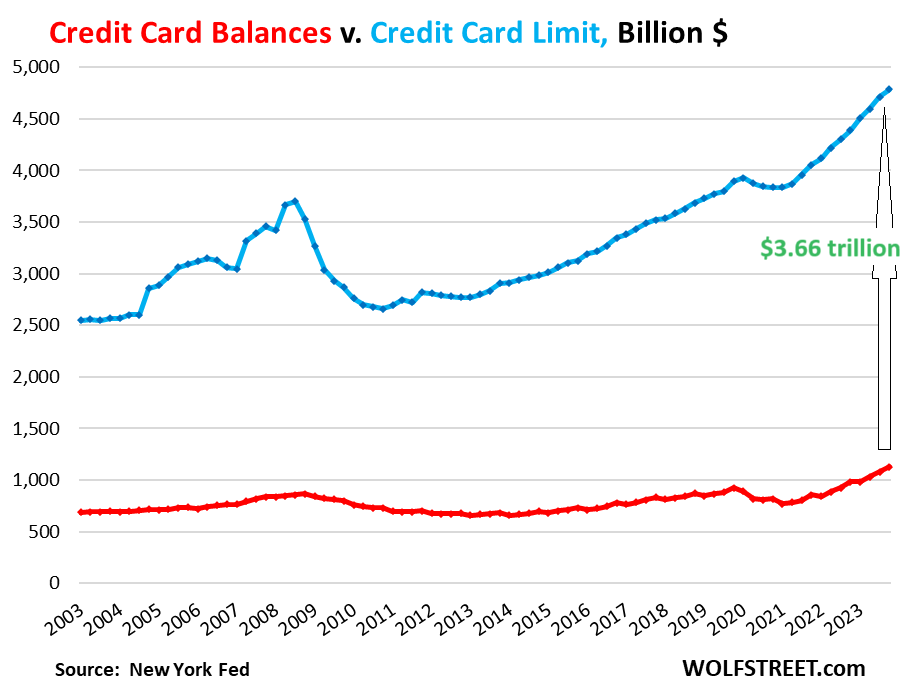

Credit is not tightening – except for subprime.

Despite all the hoopla last year about credit tightening for consumers – now forgotten, and even the Fed has axed this language from its January meeting statement – credit has not tightened in the arena of credit cards. Banks are trying as aggressively as ever to get people to set up new accounts, and they have raised the credit limits, and the aggregate credit limit has surged from record to record last year and in Q4 hit $4.79 trillion, while credit card balances ticked up to $1.23 trillion.

And the total available unused credit surged to a record $3.66 trillion. There was a credit crunch during and after the Great Recession, visible by the sharp drop in unused credit (blue line), as banks cut credit limits, closed accounts, and licked their wounds.

Subprime is always in more or less trouble, which is why it’s subprime. And the subprime segment is tightening, which we’ve already seen with auto loans. But for everyone else: banks are eager to lend them money:

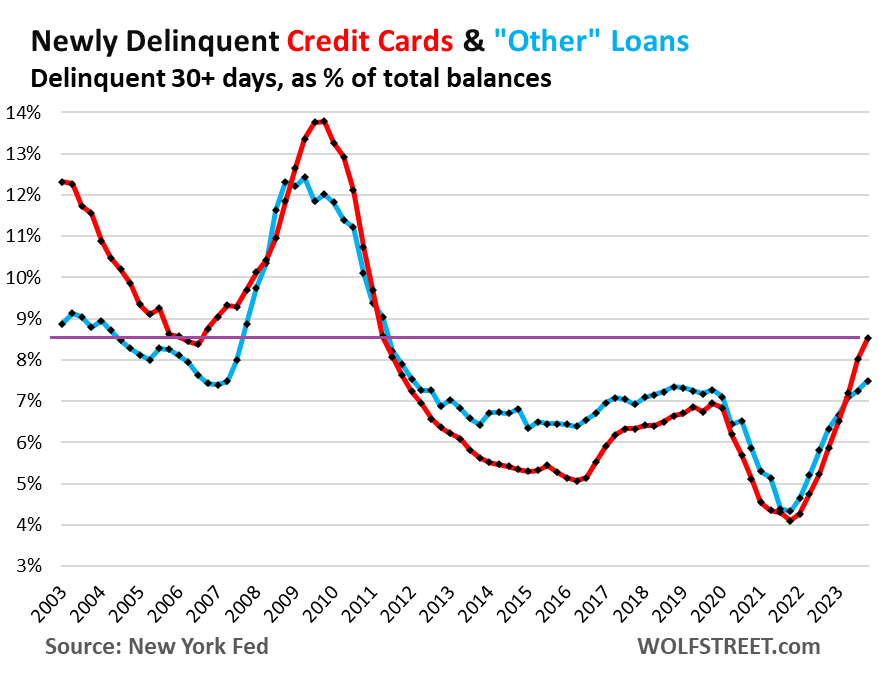

Delinquencies left the free-money trough behind.

Reality is setting in for some people. Credit card balances that are 30 days or more past due – that transitioned into delinquency at the end of the quarter – rose to 8.5% in Q4. In 2019, the rate was about 7.0%. Before the Great Recession, 8.5% was around the record low (red line).

“Other” consumer credit transitioning into delinquency – including BNPL – rose to 7.5%, just a hair above where it was in 2018 and 2019 (blue).

How many adult Americans are behind on their credit cards?

The New York Fed’s study in November, based on Equifax data and its own Consumer Credit Panel data, found that only 2% of credit-card holders were 30-plus days delinquent. So 98% of credit-card holders were current. But those are cardholders.

Only about 166 million adult Americans had credit cards, that’s 64% of the 260 million adults (18 and over) had credit cards, according to TransUnion (Feb 2023 report). The remaining 36% of adults didn’t have credit cards; they had only debit cards (the second biggest payment method) or no card at all. And those Americans cannot be behind on their credit cards because they don’t have one.

So the percentage of adults – not “cardholders” – who are 30-plus days delinquent on credit card balances is around 1.7%. That may be tough for the 1.7%, but not for the economy.

We already discussed our drunken sailors’ mortgages, delinquencies, and foreclosures: Here Come the HELOCs: Mortgage Balances, Delinquencies, and Foreclosures. And their auto loans and delinquencies: Auto Loan Balances, Subprime, Delinquencies, and Income: Who Are those Drunken Sailors?

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter February 9th, 2024

Posted In: Wolf Street