ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

July 14, 2023 | Honey, the Dollar’s Collapsing Again: USD against Yen, Euro, Peso, Other Currencies amid Inflation, Rate Hikes, and QT (or Lack Thereof)

Wolf Richter

The dollar-collapse and dollar-crash folks are out in force. “The dollar crashed to its lowest in more than a year on Wednesday after data showed the rise in U.S. consumer prices moderated in June, suggesting the Federal Reserve may have to raise interest rates only one more time this year,” Reuters said, which put one of those lopsided dry grins on my face.

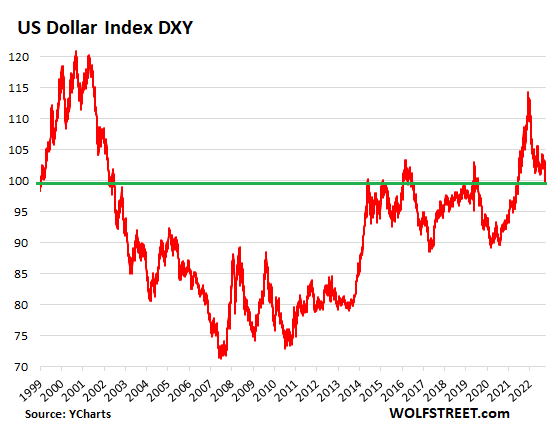

And the dollar has dropped a bunch, but since September last year, off a majestic spike and two-decade high against a basket of other currencies, tracked by the Dollar Index (DXY), which is dominated by the euro and the yen. And that spike had worried a lot of people, companies, and governments around the world because all heck breaks loose when the dollar gets strong – especially in emerging markets.

So after this fearsome plunge, the dollar is now back where it was at the high in April 2020 and at the highs in the years 2015-2017, and it’s back where it had been in 1999. And it was a LOT lower in between. In other words, the dollar is back at the higher end of the normal range over the past 20 years (data via YCharts):

Both the euro and the yen had been plunging through October 2022: The Fed had been hiking rates since March 2022 and cranking up QT since July 2022, and in 12 months hiked by 5 percentage points, while the ECB just started hiking rates out of the negative in July, and it only announced QT in October, as inflation was already raging; and while the Bank of Japan was – and is to this day – still clinging to its negative-interest-rate absurdity and its yield curve control even as inflation is spiraling higher. So the dollar battered their currencies last year.

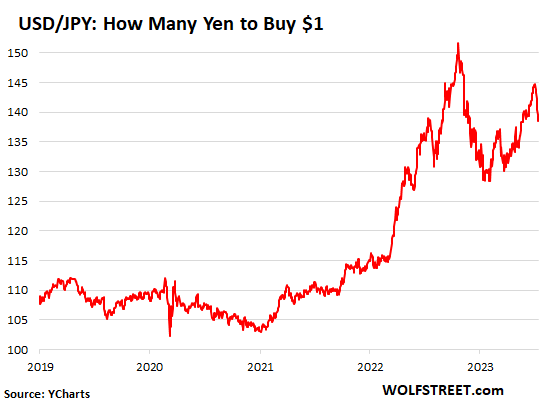

The yen has become a sloppy mess.

Last year, the yen dropped in a huge slide, from ¥110 per dollar in 2021, to ¥151 per dollar by October 2022, triggering verbal and finally actual interventions in the currency markets by the Ministry of Finance, which blew $68 billion in USD assets to buy YEN, spread over three days, which caused the yen to recover some before losing more ground again this year. By June, when the yen pushed again over the 140-line, there was more talk of interventions by the MoF (data via YCharts):

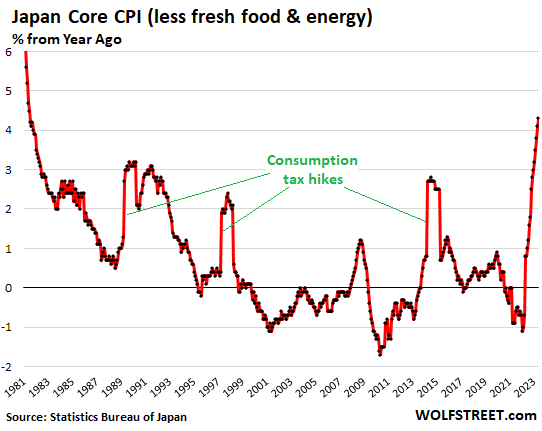

The problem for the yen is the toxic mix of inflation and the Bank of Japan’s decision to let inflation rip. Japan’s core CPI spiked to 4.3% year-over-year, the worst since 1981. Month-to-month, the three-month moving average of core CPI spiked to an annualized rate of 6.6%. Food inflation spiked to 8.6% year-over-year, the worst since 1976.

And yet, the Bank of Japan decided to keep its short-term policy rate in the negative, and to keep repressing long-term rates via its yield curve control, capping the 10-year yield at 0.5%, though it had raised the cap from 0.25% late last year. Japan now has the worst negative real rates in the developed world.

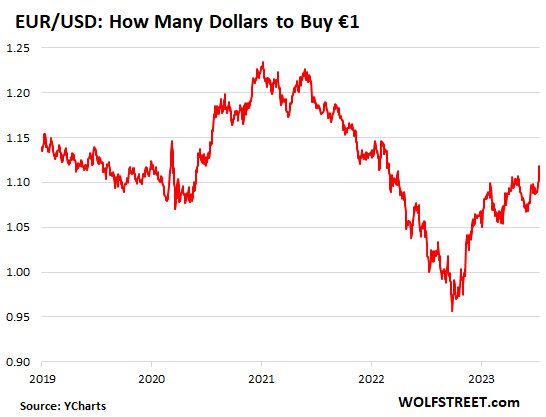

The euro recovered after the ECB began to tighten.

The euro had dropped as low as $0.96 by October 2022, from the $1.20 range in 2021, as raging inflation had broken out worse even than in the US. But by that time, the ECB became hawkish. It has by now hiked by 4 percentage points; and it has shed €1.6 trillion in assets from its gigantic balance sheet, and euro traders noticed. The euro has surged against the dollar, from $0.96 per euro in October 2022 to $1.12 today, and is now back in the historically normal range against the dollar:

Inflation in the US isn’t going to just vanish. What had pushed down overall CPI on Wednesday was mainly the plunge in energy prices. Core CPI came in at 4.8%, higher than overall CPI. The all-important core services CPI (without energy services) was a still red-hot 6.2%. And there are several factors in the second half that we already know today that will provide upward momentum to CPI, and we discussed this whole situation here.

So the idea was to enjoy these still bad CPI readings as long as we can, before they take another turn for the worse again? In terms of the dollar, any reason why it does whatever it does on a particular day is a good reason, but it’s now back where it sort of belongs, at the upper end of the normal 20-year range.

Central banks that were able to read the tea leaves correctly and front-ran the Fed with big rate hikes were able to protect their currencies while getting a handle on inflation – letting these two get away can lead to a currency crisis in emerging markets where governments and companies have debt that is denominated in dollars. A sinking local currency makes these debts devilishly hard to service. And a number of central banks managed this precarious situation reasonably well.

The Bank of Mexico stands out. It never did QE in the first place. It started hiking in mid-2021 and hiked relentlessly by 725 basis points to 11.25%. In May it paused. Core CPI has come down to 6.9%, though this is still very high, but down from the 8.5% range. And the peso has regained all the value against the dollar it had lost during the pandemic, plus some, and is back at 16.75 pesos to the dollar, where it last had been in 2015.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter July 14th, 2023

Posted In: Wolf Street