ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 7, 2023 | The Bank of Canada Un-Pauses, Hikes 25 Basis Points, Second Central Bank to Un-Pause on Resurging Inflation Fears

Wolf Richter

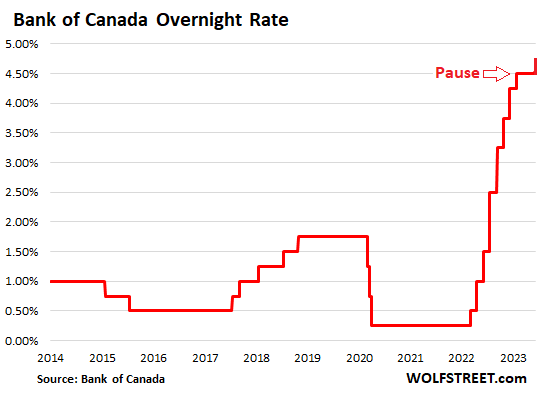

The Bank of Canada un-paused today, after having “paused” following the January hike. The pause had been widely ballyhooed as the end of the rate hikes and a pivot toward rate cuts. Those hopes have now been bitterly disappointed. Everyone is figuring out that this inflation isn’t just fading away on its own.

Today it hiked its policy rates again by 25 basis points, bringing its overnight rate to 4.75%, the highest in 22 years, in a move that surprised a lot of observers.

The Bank of Canada has now become the second central bank to pause and then un-pause, after the Reserve Bank of Australia, which had paused in April and un-paused in May, and hiked for the second time post-pause yesterday, on fears that inflation was getting entrenched via inflation expectations and surging labor costs that weren’t matched by productivity gains.

At its meeting in January, when the Bank of Canada hiked one more time and announced the pause, it stressed that it was a wait-and-see pause, not a pivot, though that message had been widely ignored. At the time, BOC Governor Tiff Macklem said in an interview, “the question really we’re asking ourselves is, ‘Have we done enough?’ We’re pausing to assess whether we’ve done enough.”

Turns out, it has not “done enough.”

The rate hike today reflects “our view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target,” it said in the statement today.

So, well, turns out, amid strong consumer spending, a tight labor market, and increased activity in the housing market, the Bank of Canada has not done enough. And it un-paused the ballyhooed pause.

The BOC pointed out that the “stubbornly high” underlying inflation rose for the first time in 10 months. The increases were broad-based across goods and services, “reflecting strong demand and a tight labor market,” it said in the statement.

The BOC is now seriously fretting about the resurgence of underlying inflation:

- “Overall, excess demand in the economy looks to be more persistent than anticipated.

- “The economy was stronger than expected” in Q1 with GDP growth of 3.1%

- “Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains.”

- “Demand for services continued to rebound.”

- “Spending on interest-sensitive goods increased and, more recently, housing market activity has picked up.”

- “The labor market remains tight: higher immigration and participation rates are expanding the supply of workers but new workers have been quickly hired, reflecting continued strong demand for labor.”

And it warned that, “with three-month measures of core inflation running in the 3.5-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.”

And the BOC put the possibility of more rate hikes on the table. It said, “We will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behavior are consistent with achieving the inflation target.”

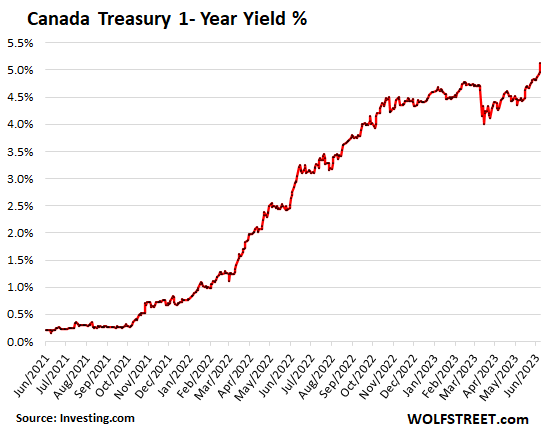

Yields jump on the move.

The Canadian bond market was surprised by the move and is now adjusting to it. The one-year yield jumped by 17 basis to 5.13% today, now expecting one more rate hike and no rate cuts within the 12-month period:

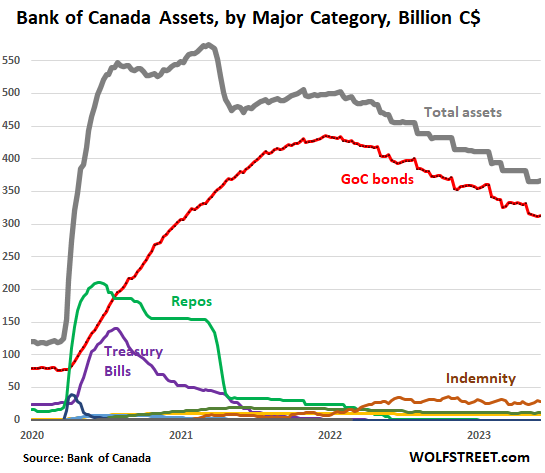

Quantitative tightening will continue.

“Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank’s balance sheet,” it said.

During its crazed QE starting in March 2020 through March 2021, the BOC piled on an additional C$455 billion in assets. As of the most recent balance sheet, it has now shed 46% of these pandemic QE assets, well ahead of the Fed and other central banks — though it’s behind the Fed on rate hikes, perhaps on the theory of faster QT and slower rate hikes.

It started early by starting to unload its repos and Treasury bills in 2020. It never seriously bought mortgage bonds and then stopped buying them altogether in late 2020. And it unwound most of its other small holdings.

Its largest remaining holdings today are Government of Canada (GoC) bonds: at C$313 billion they’re down by 27.4% (red) from the peak. The “Indemnity” reflects unrealized losses on its bond holdings, currently C$28 billion (brown), which it carries as an asset under an indemnity agreement with the Government of Canada, that, if it actually ever sold those bonds, rather than hold them to maturity, and thereby realized the losses, the government would indemnify the BOC for those losses.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter June 7th, 2023

Posted In: Wolf Street

Next: “Spitting Fucking Angry” »