ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 31, 2023 | That was Fast: Mortgage Rates Re-Spike to 7% Range as it Sinks in that the Fed Won’t Cut Rates “Anytime Soon,” Mortgage Applications Plunge to 1995 Levels. Even Investors Pull Out

Wolf Richter

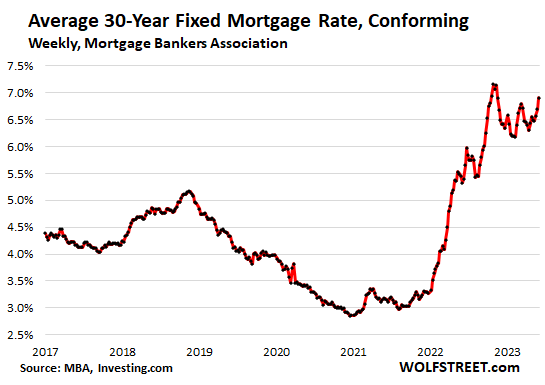

The 7% mortgages are back. The average interest rate on 30-year fixed-rate mortgages with conforming balances jumped to 6.91%, the highest since November, according to the weekly measure by the Mortgage Bankers Association today.

The daily measure by Mortgage News Daily already went over 7% a few days last week and earlier this week.

“Inflation is still running too high, and recent economic data is beginning to convince investors that the Federal Reserve will not be cutting rates anytime soon,” is how the Mortgage Bankers Association explained today what has been obvious to us here for months.

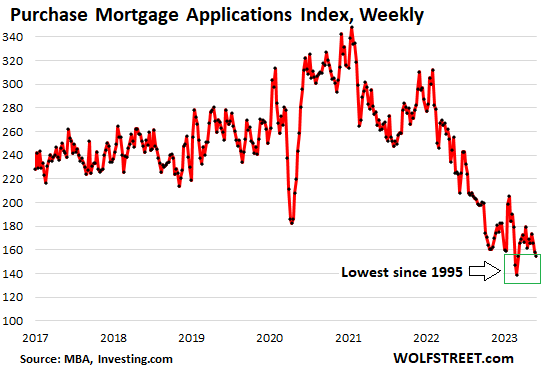

And so, with these kinds of mortgage rates, spring selling season – the time of the year when sales and prices nearly always rise from the dreary days of the winter – has turned into an amazing dud.

Applications for mortgages to purchase a home dropped for the third week in a row, from already low levels, to the third-lowest volume since 1995, the two lowest volume-weeks having been in late February this year, according to the MBA today.

Purchase mortgage applications plunged, compared to the same week in:

- 2022: -31%

- 2021: -41%

- 2019: -40%.

What comes next may get sloppy. Mortgage applications to purchase a home are a forward-looking indicator of where home sales as measured by closed deals are headed in a month or two. The 7% mortgages are indigestible at current home prices – something has to give, and it’s not going to be mortgage rates.

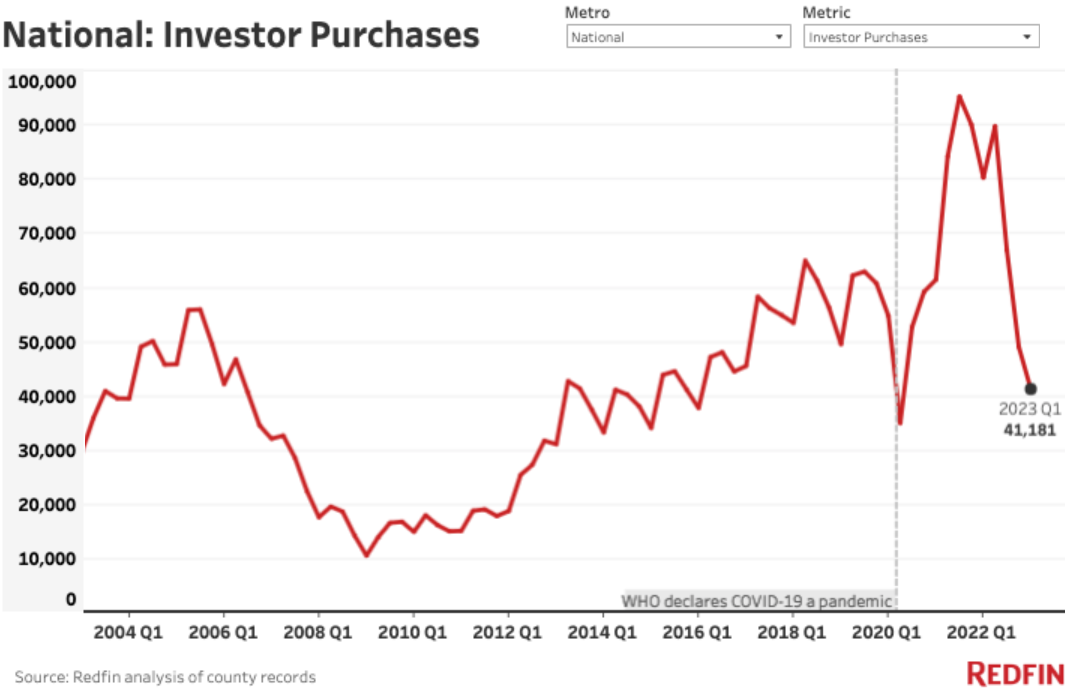

And the backward-looking data on sales volume, such as those by the National Association of Realtors, has already been lousy, amid rising supply, plunging volume, and increased days on the market, while even investors pulled out.

That investors pulled out of the housing market was confirmed by Redfin today: Purchases by investors plunged by 49% year-over-year in Q1 in the metros tracked by Redfin.

“Widespread economic uncertainty and recession fears are also prompting investors to pump the brakes. Some investors may be moving their money into other asset classes that offer better returns, such as stocks and bonds,” Redfin said.

The biggest year-over-year drops of purchases by investors:

- Nassau County, NY: -67.9%

- Atlanta, GA: -66%

- Charlotte, NC: -66%

- Phoenix, AZ: -64.2%

- Nashville, TN: -60.4%

- Las Vegas, NV: -60.2%

- Jacksonville, FL: -56.6%

- Philadelphia, PA: -56.5%

- Tampa, FL: -54.8%

- Orlando, FL: -54.7%

“Borrowing costs climbed even higher in May, meaning investors may pull back from the housing market further in the second quarter. Investor home purchases typically rise on a quarter-over-quarter basis in the spring, but we may see them fall flat or decline when second-quarter data comes in,” Redfin said.

So there goes that. The high mortgage rates had given rise to the theory that investors, who wouldn’t need a mortgage as they can finance at the institutional level, would just swoop in and pick up the pieces left behind by potential buyers staying out of the market. But that’s not happening. Investors don’t like to overpay for properties.

With the 7% mortgages now hammering the end of spring selling season, and investors pulling out on a large scale, home sales going into the summer could turn out to be dismal.

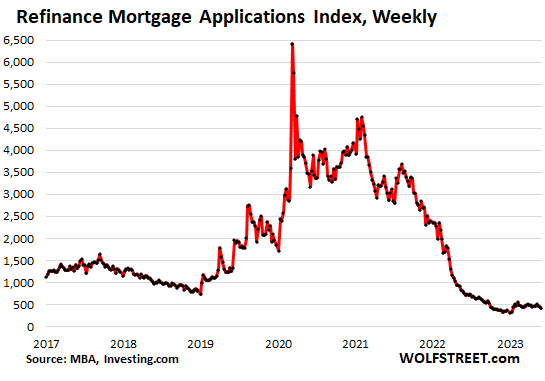

Applications to refinance existing mortgages collapsed in 2022, as mortgage rates surged, and have since then been wobbling along at the lowest volume since January 2000. The mortgage industry was among the first industries to announce mass layoffs in late 2021 and into 2022. Refinancing mortgages was a huge portion of the revenues for mortgage lenders and brokers, and it vanished.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter May 31st, 2023

Posted In: Wolf Street

Mr. Richter you failed to mention that recently 42% home purchases was by cash sell, no mortgage needed. I have been hearing about a Housing crash for the last year and half, just like we are going to have a bad recession. Gloom and Doomers are wrong the majority of the time. Ex: Dent, Hussman, Kaplan and Stanberry to name a few.