ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

December 29, 2022 | Federal Reserve & Misconception

Martin Armstrong

There is an onslaught of misinformation about the Federal Reserve from everything that it can go bankrupt, and the Treasury will become a second central bank, and of course, the Fed is really the cause of inflation and its balance sheet. The proposal by Janet Yellen to buy in long-term debt and swap it with short-term is not “creating” money for the Treasury has no such power. It was a proposal for a debt swap to shorten the yield curve since the long-end is volatile. The first proposition that the Fed can go bankrupt only suggests that people do not comprehend that the Fed is different entirely from the European Central Bank.

There is an onslaught of misinformation about the Federal Reserve from everything that it can go bankrupt, and the Treasury will become a second central bank, and of course, the Fed is really the cause of inflation and its balance sheet. The proposal by Janet Yellen to buy in long-term debt and swap it with short-term is not “creating” money for the Treasury has no such power. It was a proposal for a debt swap to shorten the yield curve since the long-end is volatile. The first proposition that the Fed can go bankrupt only suggests that people do not comprehend that the Fed is different entirely from the European Central Bank.

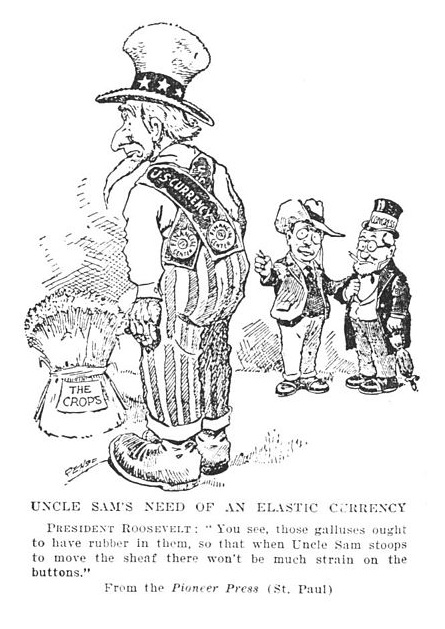

The Fed has the authority to create elastic money for it followed the very idea of J.P. Morgan and how he saved the economy during the Panic of 1907. The Fed can create money when there is a shortage due to economic contractions (hoarding), and it can then reduce its balance sheet reducing the money supply. When the Fed was created, it was established with branches around the country because the Panic of 1907 exposed that there were regional capital flow problems. The 1906 San Francisco Earthquake drained the cash from the East where all the insurance companies were.

The Fed has the authority to create elastic money for it followed the very idea of J.P. Morgan and how he saved the economy during the Panic of 1907. The Fed can create money when there is a shortage due to economic contractions (hoarding), and it can then reduce its balance sheet reducing the money supply. When the Fed was created, it was established with branches around the country because the Panic of 1907 exposed that there were regional capital flow problems. The 1906 San Francisco Earthquake drained the cash from the East where all the insurance companies were.

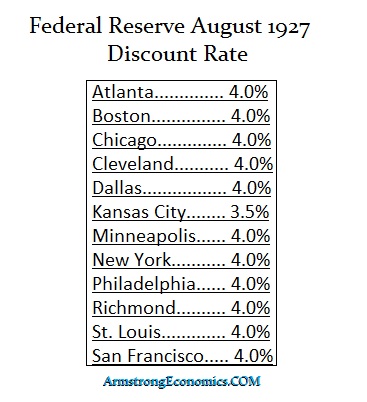

As we can see from this clip of rates in 1927, each branch was independent. There was an excess case in Kansas City so they lowered the interest rates there in hopes that capital would migrate to the other districts to earn more interest. All of that was eliminated by Franklin D. Roosevelt who wanted (1) to stack the Supreme Court to approve his Marxist agenda, which failed, and then he usurped all the power of the Federal Reserve and created the Washington headquarters and the President then was to appoint the head of the Federal Reserve and to illegally lobby him to ensure that his presidential agenda was to be the policy at the Federal Reserve. There was no more independence of the branches.

When Biden was running in 2020, he actually proposed requiring the Federal Reserve to regularly report on what they are doing to close economic gaps that exist along racial lines in the United States. Biden has viewed the Fed as a social tool and he has been making efforts to manipulate the Federal Reserve which will be extremely dangerous if they are carried out. Now, the Biden Administration is talking about closing branches of the Federal Reserve and replacing those board members with his hand-picked political cronies. In January 2022, he was pushing for black economists to be appointed to the Federal Reserve Board. My concern is that academics have ZERO experience and do not really understand the global economy trapped by domestic Keynesian Economics.

It was Paul Volcker who Chaired the Fed into the high in the interest rates back in 1981 who concluded in his Rediscovery of the Business Cycle that “it was not until the events of 1974 and 1975, when a recession sprung on an unsuspecting world with an intensity unmatched in the post-World War II period, that the lessons of the ‘New Economics’ were seriously challenged.” However, former Fed Chair Ben Bernanke has suggested that the Fed’s failure to contain inflation during the 1970s traced back to the political forces that shaped the Fed chairs in charge that he expressed in his book “21st Century Monetary Policy.” He wrote that the inflation of the ’70s puzzled economists relying on the 1958-ventage Phillips Curve, which would have predicted high inflation only in combination with extremely low unemployment rates. Bernanke admitted that the Phillips curve had “broken down” during the 1970s.

The critical problem with the entire way we view inflation rests on the QTM (Quantity Theory of Money) and the assumption that a mere increase in supply must produce inflation. There is absolutely nothing in the economic data that supports these old theories that were based upon (1) fixed exchange rates, and (2) the supply & demand theory dates back to the days of coinage. It was John Law who came up with the supply/demand theory that everyone else plagiarized, including Adam Smith. John Law’s writings influenced many, although they would never admit it. He was clearly the FIRST to use the term DEMAND and he was certainly the FIRST to join it with the word SUPPLY, for only a trader could have seen this connection in the price movements of anything.

The critical problem with the entire way we view inflation rests on the QTM (Quantity Theory of Money) and the assumption that a mere increase in supply must produce inflation. There is absolutely nothing in the economic data that supports these old theories that were based upon (1) fixed exchange rates, and (2) the supply & demand theory dates back to the days of coinage. It was John Law who came up with the supply/demand theory that everyone else plagiarized, including Adam Smith. John Law’s writings influenced many, although they would never admit it. He was clearly the FIRST to use the term DEMAND and he was certainly the FIRST to join it with the word SUPPLY, for only a trader could have seen this connection in the price movements of anything.

The greatest fallacy of Keynesian Economics, Supply v Demand, and the Phillips Curve is that they have ALL failed because the US dollar is the reserve currency of the world and by default, the Federal Reserve has become the central bank of the world. With Biden desperate to get his hands around the neck of the Federal Reserve and force it to yield to his political agenda, threatens more than merely the US economy – but the entire world. Bernanke acknowledges in his book:

“Martin, my boys are dying in Vietnam, and you won’t print the money I need,” President Lyndon B. Johnson reportedly told then-Fed Chair William McChesney Martin Jr. at his Texas ranch after the central bank announced a half-point increase to its key discount rate over inflation fears, Bernanke writes. White House tapes, meanwhile, reveal President Richard Nixon frequently appealing to Fed Chair Arthur Burns’ Republican-party ties to clear the runway for more easy-money policies, with one call going as far as urging the Fed chair not to make any policy decisions that could “hurt us” in the November 1972 election.

I warned the Fed back then that buying in 30-year bonds during the 2007-2009 Financial Crisis, would NOT stimulate the domestic economy for one simple reason and this is why both the goldbugs and central bankers have been wrong. The domestic money supply DID NOT increase to stimulate when China was saying thank you very much and swapping their 30-year holdings for 10-year or less. The assumption that any central bank can control the domestic economy is absurd. The holdings of debt are global. Therefore, buying in 30-year bonds to reduce the supply in hopes of reducing the mortgage rates failed because the money did not stay in the USA. That is why the Fed then began to buy the mortgaged-backed securities because that was a more direct impact domestically.

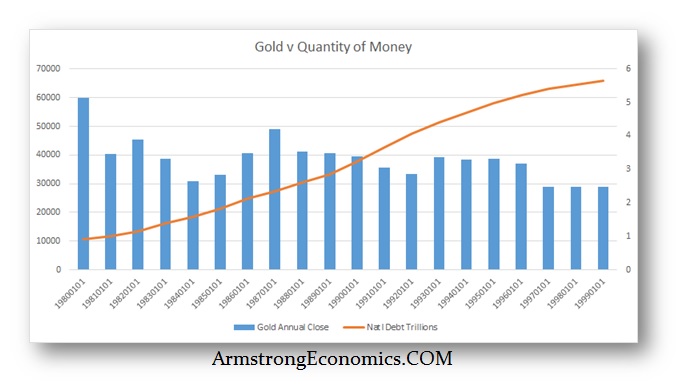

As the money supply increased and the national debt rose consistently, gold declined from 1980 into 1999 for 19 years. All the theories of inflation driving gold higher were simply wrong just as the central bankers relied on the very same theories.

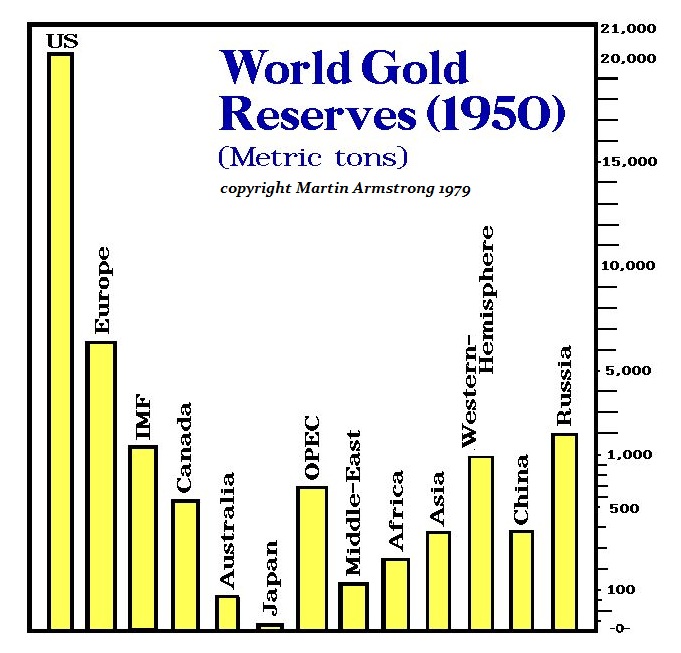

It was World War I and II that drove the gold to flee to the United States so by 1950, there was no choice but to make the dollar the reserve currency. Yet more significant was the realization that the factor which produced that result was ENTIRELY external to the domestic economy. Therefore, all the economic theories were bogus because they were all focused on domestic policy thanks to Karl Marx whose central theory was the government possessed the power to eliminate the business cycle by confiscating all private assets. That altered human nature and created economic stagnation. Nevertheless, Keynes and everyone else have sought to accomplish the very same authority that Marx maintained existed.

This focus on GDP (Gross Domestic Product) has reversed the GNP (Gross National Product), which was more global in its scope. If we attributed world trade to the flag the company flies rather than where it sets up a plant, then you would see that the United States has a trade surplus and not a trade deficit. This is also a backdrop to the reserve status of the dollar. Perhaps the greatest of all the wild proposals is that somehow Bitcoin will rise from the ashes and become the new Reserve Currency of the world. So all governments will issue debt in Bitcoin? Politicians will never be able to run for office and Socialism must collapse if there is a fixed amount of money. That is what the elastic money supply was to help – depressions and recessions.

Rather than betting on the power grid to survive if governments collapse, I think we will see the pre-1965 silver coins return for a medium of exchange and gold for larger transactions. I have said plenty of times, GOLD will NOT rise as a hedge against inflation, it is a hedge against the collapse in confidence of the government.

As I have written before, when the Japanese government lost the confidence of the people, they lost the ability to produce any money for 600 years. The people used the coins of China and bags of rice – no Japanese coins were ever acceptable for 600 years, which was the same time interval it took to reestablish gold in Europe following the fall of the Roman Empire.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Martin Armstrong December 29th, 2022

Posted In: Armstrong Economics