ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

November 7, 2023 | Mortgage & HELOC Balances, Delinquencies, Foreclosures: How Are our Drunken Sailors Holding Up?

Wolf Richter

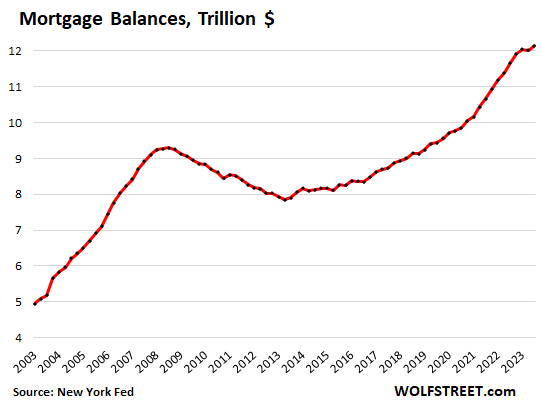

Mortgage balances outstanding ticked up 1.0% in Q3 from Q2, to a new record of $12.1 trillion, after having dipped in Q2, according to data from the New York Fed’s Household Debt and Credit Report. This increase is less than half the pace than the big jumps during the era of the 3% mortgages, when mortgage balances had soared quarter-to-quarter by as much as 2.8% in Q2 2021.

Year-over-year, mortgage balances rose 4.0%, down by over half from the year-over-year increases in 2021 and 2022 that had reached 10%. In a moment, we’ll look at what could cause an uptick in mortgage balances even as home sales have plunged and as mortgage applications to purchase a home have collapsed.

Mortgage balances rise or fall based on diverging dynamics, on the plus side and on the minus side.

What adds to mortgage balances:

- The growing total inventory of homes (it constantly increases due to new construction) owned by a growing population.

- Prices rise over the years (newly purchased homes are financed with bigger mortgages). Price soared in 2020-2022, dictating today’s big mortgages.

- A boom in cash-out refis (nope, not now).

What subtracts from mortgage balances:

- Regular mortgage principal payments.

- Mortgage payoffs — and people with 3% mortgages are clinging to them.

- Falling home prices mixed with a wave of foreclosures – which caused mortgage balances to fall during the housing bust.

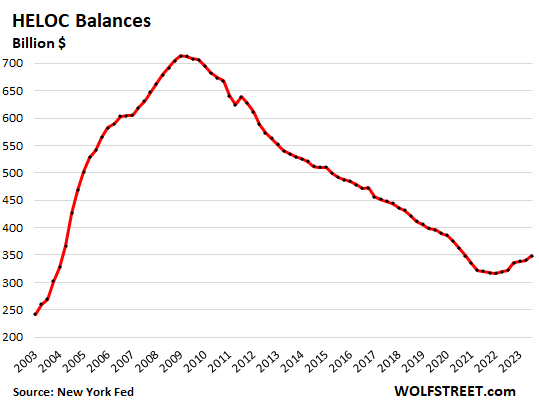

HELOC balances have been rising for four quarters from historic lows. Homeowners with 3% mortgages can no longer cash-out-refi their homes without causing a catastrophic increase of their mortgage payment, as the entire 3% mortgage would be replaced with a 7%-plus mortgage. A HELOC accomplishes the same thing but the 3% mortgage stays in place, and only the HELOC portion comes with a 7%-plus price tag.

HELOC balances rose by $9 billion, or by 2.6% in Q3 from Q2, to $349 billion. They remain extremely low, considering the increase in home prices over the 20-year period, as homeowners used refis, instead of HELOCs, to draw out cash over the past decade:

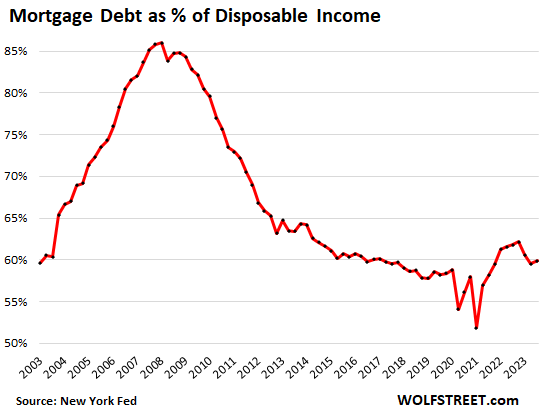

The burden of mortgage debt. Homes are lot more expensive today than they were 20 years ago, but consumers make a lot more money too, and there are lot more homes and a lot more consumers owning them. Turns out, after massive gyrations, overall mortgage debt as a percent of disposable income is roughly where it had been in 2003.

Disposable income is income from all sources except capital gains, minus taxes and social insurance payments. This is the cash that consumers have left to spend on housing, food, cars, etc.

Note the impact of the pandemic-era funds that consumers got (stimulus payments, PPP loans, etc.) that caused disposable income to spike, and therefore the burden ratio to fall. And note the impact in recent quarters of the biggest pay increases in 40 years, even as mortgage debt barely increased.

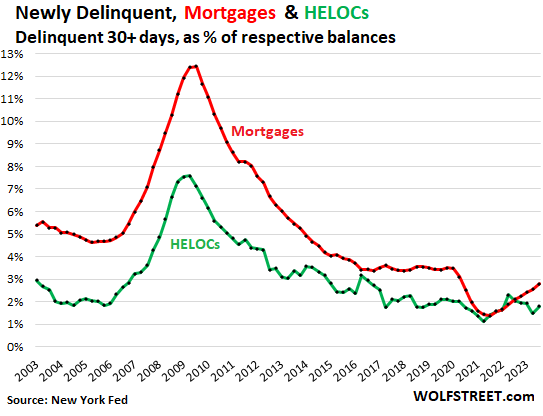

Transitioning into delinquency: 30+ days. Mortgage balances that were newly delinquent by 30 days or more at the end of the quarter ticked up to 2.8% of total balances, which is still lower than anytime before the pandemic and down from the 3.5% range during the Good Times in 2017-2019 (red line in the chart below).

For HELOCs, the 30-plus-day delinquency rate rose to 1.8% in Q3, after having dropped to 1.5% in the prior quarter and remains ultra-low (green line).

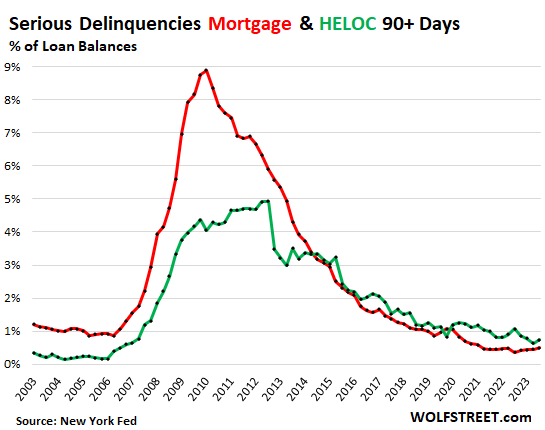

Serious delinquency: 90+ days. Mortgage balances that were 90 days or more delinquent by the end of the quarter edged up to 0.50% in Q3 from 0.46% in the prior quarter, about half the rate from the Good Times before the pandemic and from the Good Times before the housing bust (red line in the chart below).

For HELOCs, the 90+ day delinquency rate inched up to 0.74% in Q3, from 0.64% in the prior quarter, which had been the lowest since before the Housing Bust (green line).

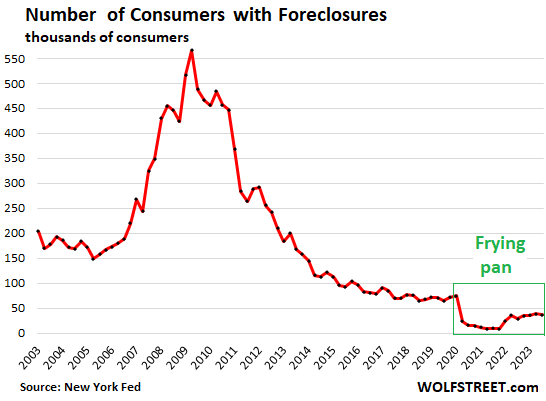

Foreclosures in a frying-pan pattern. The number of consumers with foreclosures fell by 7% quarter-to-quarter to 36,100 in Q3, down by about 45% from the Good Times before the pandemic in 2017-2019, and down by 75% from the Good Times in 2003-2004 when the housing market was approaching the peak of the prior housing bubble.

The fiscal and monetary excesses during the pandemic, the forbearance programs, and foreclosure bans reduced foreclosures to near zero. Now they’ve come up a little from these lows but remain ultra-low.

So sure, someone clever could come up with a clickbait-title about foreclosures “exploding by 345%,” OMG, from Q2 2021. And we’ll just laugh about it and move on.

Note the frying-pan pattern, as I call it, of which we’re going to see more as things normalize from the crazy times:

Where’s the hangover from the party? In terms of financial stress that households have with mortgages, a massive hangover doesn’t set in until home prices decline substantially and homeowners are losing their jobs in large numbers.

Homeowners are at risk of foreclosure if they lose their income and can’t make their mortgage payments and if at the same time the market value of their house drops substantially below the loan value of the mortgage.

A homeowner that cannot make the payment, but can sell the home for the loan value or more, can just sell the home and move on, perhaps with some cash to go.

But when the net proceeds from the sale fall below the loan balance, homeowners who lost their jobs would have to come up with extra cash to pay off the mortgages, and that’s where the problems arise.

Homeowners who bought over the past two years in some markets where home prices have dropped and who skimped on the down-payment could fall into trouble if they lose their jobs for long enough. For now, the job market is strong, so this fate would be limited to a small number of homeowners, which is why delinquency rates and foreclosures are still extremely low. But a substantial rise in unemployment combined with a substantial decline in home prices across many big markets would increase the delinquency rates and foreclosure rates.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter November 7th, 2023

Posted In: Wolf Street

Next: Dash for Cash Intensifying »