ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

September 10, 2023 | Mortgage-Rate Buydowns by Homebuilders Are Now All the Rage to Prop Up Sales, Lowering Effective House Prices in a Big Way, but Don’t Get Picked Up by House Price Data

Wolf Richter

Homebuilders don’t have the luxury of outwaiting the market, or waiting for the Fed to slash rates, or whatever, they must build and sell homes, that’s their business, no matter what the conditions in the market.

And the market is struggling with 7%-plus 30-year fixed mortgage rates and sky-high prices, after a ridiculous free-money spike during the pandemic. Sales of existing homes have plunged by about 25% from the same period in 2018 and 2019, and by about 32% from the same period in 2021, because buyers have pulled back, and the people with 3% mortgages have left the housing market altogether, not putting their homes on the market and not buying homes either, not even looking at homes.

That plunge in sales might be OK with potential home sellers, thinking that this too shall pass, but it’s not OK with homebuilders, and they’ve been adjusting to this market by cutting prices, building at lower price points, buying down mortgage rates, and offering incentives, such as free upgrades.

The latter two – buying down mortgage rates and piling on incentives – don’t show up in the prices of the homes they sell. So the pricing data that we have from the Census Bureau about sales of new single-family houses do not include the costs of mortgage-rate buydowns and incentives.

The duration of the buydown can be for a few years, which effectively turns it into a teaser rate that can cause problems when the rate jumps to normal.

Or the rate-buydown can be for the entire term of the mortgage (“permanent”).

The big homebuilders have mortgage-lender subsidiaries that originate the mortgage for their customers and then sell the mortgage to Government Sponsored Enterprises, such as Fannie Mae, which will securitize the mortgages into MBS. For example, the mortgage-lender subsidiary of D.R. Horton is DHI Mortgage Company.

Having their own mortgage lender makes rate buydowns a lot simpler for homebuilders. This is similar to the “captive” auto lenders, such as Ford Credit offering 0% 36-month financing for F-150 XLTs at the moment.

The costs of the mortgage-rate buy-downs can be big, because the home prices are big, and buydowns effectively lower the sales price of the home.

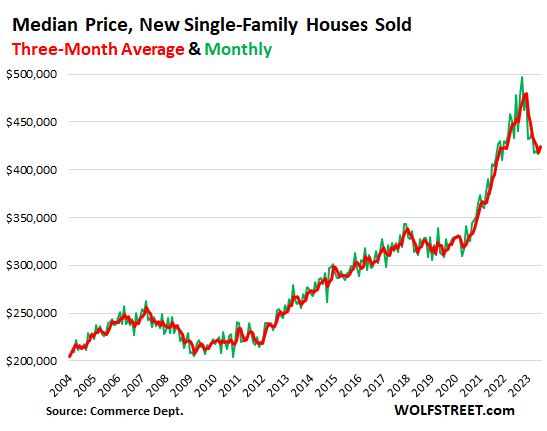

But the costs of buydowns don’t show up in the national median price of new houses sold. The numbers only show the contract prices. July’s median price (green) and the three-month-moving average of the median price (red) of signed contracts dropped by roughly 12% from the peak in late 2022, according to Census Bureau data. Now figure in the cost of rate buydowns, and the prices would have dropped a lot lower:

Concerning the mortgage-rate buydowns, John Burns Research and Consulting, which among other things regularly surveys homebuilders, came out with an interesting note about mortgage-rate buydowns by homebuilders in Florida, based on its regular surveys of homebuilders, phone calls, community visits, etc., plus this time, to supplement the data: “our survey team visited 13 home builders, three land brokers, and a regional developer in Jacksonville and Orlando.”

John Burns chose Jacksonville and Orlando because they’re “more rate sensitive than other Florida markets that attract a higher percentage of retirees who pay all cash and don’t need rate buydowns.”

In a prior note, John Burns said that 5.5% seems to be the “magic number” that makes home sales happen for homebuilders. This is what the survey found:

“Permanent buydown: Buying the 30-year fixed mortgage rate down permanently to 5.25% to 5.75% is making a positive difference in allowing home buyers to qualify for the home purchase.”

“Sub 5%: Builders will even buy the current rate down to 4.75% to 4.99% for inventory homes they want to sell quickly.

“Prepaying for even lower rates: Using a forward commitment, a builder’s mortgage company can originate FHA (Federal Housing Administration) or conforming mortgages at a below-market rate. Often, these buckets of money must be used within 60–90 days, so they work best when builders have nearly completed inventory.

“Temporary buydowns: A couple of Florida builders are using 2-1 temporary rate buydowns (a mortgage rate that is -2% lower in year one and -1% lower in year two) as part of a flex-cash program, allowing buyers to spend the dollars on closing costs, design center options, or a longer rate buydown. A move-up builder sees buyers accepting current elevated rates and planning to refinance when rates drop. This article explains temporary rate buydowns.

“Managing cancelation risk: One builder requires a 20% down payment from buyers receiving a 30-year rate buydown.

“Good to be big: Smaller production builders may struggle to compete for sales due to limited access or high costs of capital that curb their ability to provide inventory homes and rate buydowns.”

What about profit margins and appraisal issues?

“Builders did not express concerns regarding their margins, even though 30-year rate buydowns are expensive,” John Burns said.

“We have not heard of appraisal issues that could potentially stem from the heavy incentives offered but are monitoring for potential risk,” John Burns said.

And they’re hidden from the national house price data.

In the auto industry, rate buydowns are in lieu of cash incentives, such as rebates or dealer cash, and the customer chooses: either 0% financing or the cash incentives. The cash incentives translate into an explicit lower selling price that the customer sees in the sales contract and that then becomes part of the national data, such as the Average Transaction Price, new vehicle CPI, etc., and ultimately it percolates through to used vehicle values.

John Burns did not say, and I’m not aware of a similar pricing transparency among homebuilders where customers could choose, for example: on a $500,000 house, either a 5.5% 30-year fixed rate mortgage or a $100,000 discount on a deal funded with a 7.3% mortgage. Or maybe a $50,000 discount since few homeowners keep a mortgage for 30 years (the average length of a 30-year mortgage is about 10 years before it gets paid off).

But the effective price difference due to the rate-buydown doesn’t show up in the numbers. And we don’t know just how far the effective prices of new houses have dropped; and appraisers – according to John Burns – have not yet caught on to it either.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter September 10th, 2023

Posted In: Wolf Street