ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

April 6, 2023 | Fed’s Balance Sheet Plunges by $101 Billion in Two Weeks, as QT Continues and Bank Liquidity Support Begins to Unwind

Wolf Richter

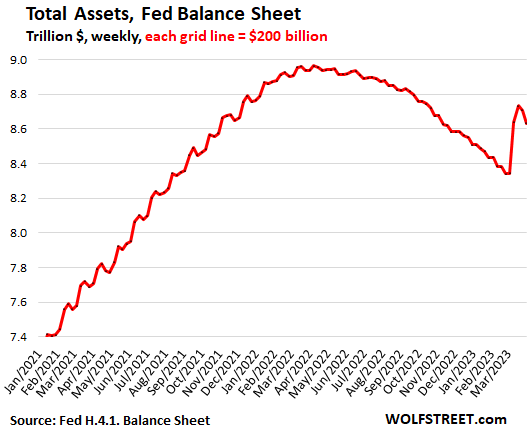

The Federal Reserve’s balance sheet plunged by $101 billion in two weeks – by $74 billion in the current week and by $27 billion in the prior week – as quantitative tightening (QT) continued at the normal pace and as banks have started paying back the liquidity support offered by the Fed when Silicon Valley Bank and Signature Bank collapsed, and a week later when, under pressure from Suisse regulators, Credit Suisse was taken under by UBS.

During the last post-meeting press conference, Powell explained this new regime – the distinction between ongoing tightening and brief liquidity support for the banks, and that both can run simultaneously.

Looking at it with a magnifying glass to see the details of the past four weeks:

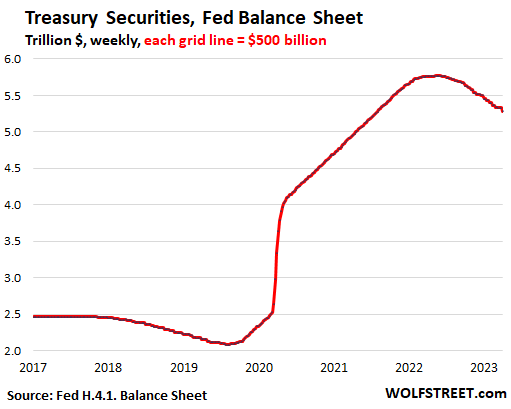

QT continued with Treasury securities: -$56 billion in four weeks, -$491 billion from peak, to $5.28 trillion, the lowest since August, 2021.

Treasury notes and bonds “roll off” the balance sheet when they mature, which is when the Fed gets paid face value for the maturing Treasury securities. Maturity dates fall either on the middle of the month or at the end of the month.

The cap for the monthly roll-off is $60 billion; in February, the Fed exceeded the cap by a hair, in March, it was a hair short.

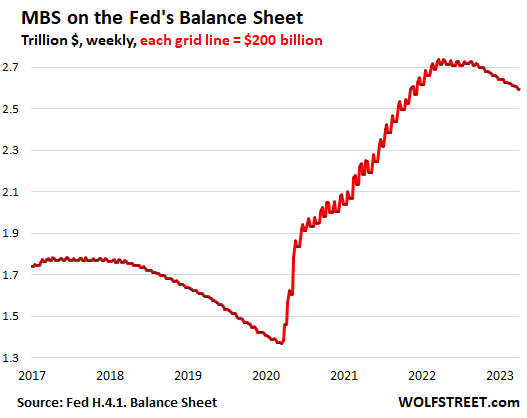

QT continued with MBS: -$16 billion in four weeks, -$146 billion from peak, to $2.59 trillion.

The Fed only holds “Agency MBS” which are all backed by the US government, and the taxpayer carries the credit risk.

Mortgage-backed securities roll off the balance sheet primarily through the pass-through principal payments that all holders receive when mortgages are paid off, such as when mortgaged homes are sold or mortgages are refinanced, and when regular mortgage payments are made.

The cap for the monthly roll-off is $35 billion. The roll off has been below the cap as home sales have plunged and as refis have collapsed.

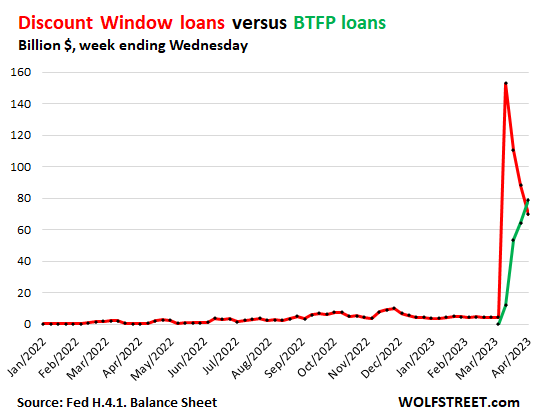

Liquidity support begins to unwind and shift.

The Discount Window (“Primary Credit”) has been available for banks for a long time. Being lender of last resort to the banks during a bank panic is one of the Fed’s functions. But this is expensive money for banks. After the rate hikes on March 22, the Fed charges banks 5.0% to borrow at the Discount Window. In addition, they have to post collateral valued at “fair market value.” So after the initial spike on the March 15 balance sheet, the banks that had borrowed at this facility started paying down their loans quickly.

It seems – we don’t get names – some banks are paying down their discount window loans with funds they borrowed under the new liquidity program, the Bank Term Funding Program (BTFP), that the Fed rolled out on March 13.

Under the BTFP, banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. This rate is currently somewhat lower than the 5% discount window rate. Banks also have to post collateral, but valued only “at par.”

To be eligible for the BTFP, per term sheet, the collateral has to be “owned by the borrower as of March 12, 2023,” and banks cannot buy securities at market price and post them as collateral at par.

For banks, the BTFP is still expensive money – though less expensive than the Discount Window – because they have to post collateral, when they could normally borrow from depositors or unsecured bondholders without having to post any collateral.

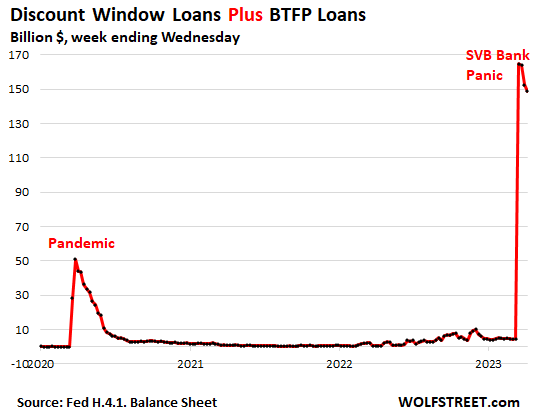

Discount Window: -$18 billion in the week, -$83 billion in three weeks, to $70 billion (from the peak of $153 billion three weeks ago).

Bank Term Funding Program (BTFP): +$15 billion in the week, to $79 billion.

This chart shows both, the loans at the Discount Window (red) and the loans at the BTFP (green):

Discount Window plus BTFP added together: -$4 billion in the week, -$16 billion in three weeks, to $149 billion.

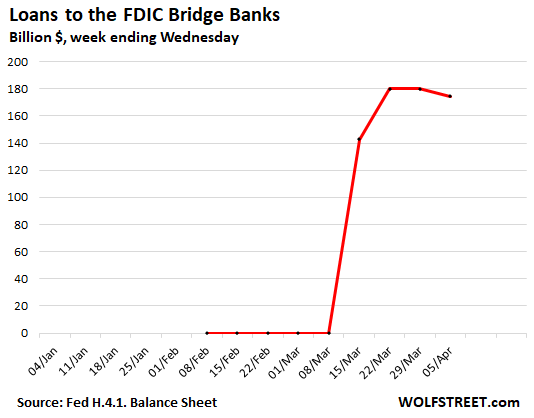

Loans to the two FDIC bridge banks: -$5 billion in the week, to $175 billion. These “Other credit extensions,” as they’re called on the Fed’s balance sheet, are loans to the FDIC-owned bridge banks that hold the assets and liabilities of the collapsed Silicon Valley Bank and Signature Bank. This facility is part of what the Fed announced on March 13.

The FDIC is in the process of selling some of the assets and transferring the deposits to other banks. In addition, it announced today that it has selected the world’s biggest bond-fund manager, BlackRock, to sell the MBS and Treasury securities that SVB and Signature Bank had held. It estimated earlier that its total loss, after everything is sold off, will be $22 billion, to be paid for by the FDIC-insured banks.

As those sales close, the FDIC will use the proceeds to pay down the advances from the Fed, and this balance will eventually go to zero.

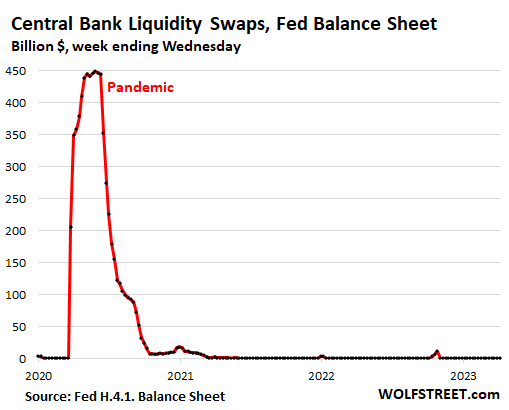

Central Bank Liquidity Swaps: No activity. These swap lines have been open for many years, and the Swiss National Bank has been one of the central banks on the other side. But the SNB did not use this facility to obtain dollar liquidity during the Credit Suisse panic, when Suisse regulators forced UBS to take Credit Suisse under. It likely used repos instead (see below).

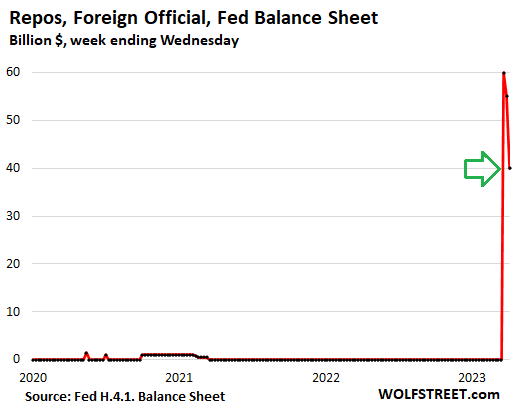

Repos with “foreign official” counterparties: -$15 billion in the week, -$20 billion in two weeks, to $40 billion. The Fed has for years offered repurchase agreements to foreign central banks, where they can get short-term dollar liquidity against collateral of eligible US securities, such as Treasury securities that they’re holding.

This is likely where the SNB got $60 billion in dollar-liquidity two weeks ago to support the CS takeunder, instead of using the central bank liquidity swap lines, and then paid down the balance by $20 billion:

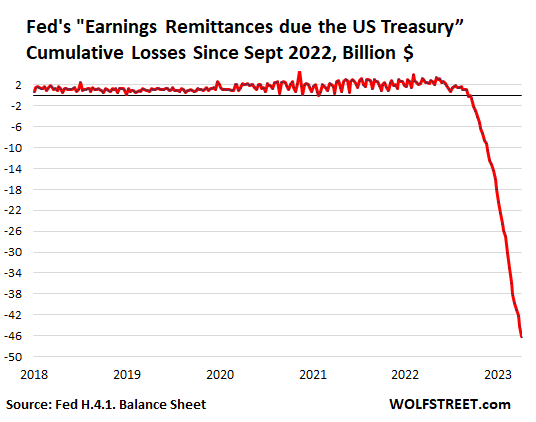

Other balance-sheet stuff: Fed’s cumulative operating loss since Sep 2022 = $46 billion.

These are not “unrealized losses” from the Fed’s portfolio of securities, but actual operating losses where it paid out more in interest to banks on their deposits at the Fed (“reserves”) and to money-market funds on reverse repurchase agreements (RRPs), than it takes in interest from its bond holdings.

From September 2022, when the Fed first started making operating losses, through today’s balance sheet, the Fed lost $46 billion.

In 2022 up to September, the Fed still had made an operating profit of $78 billion, which it remitted to the Treasury Department, as it is required to do – a sort of 100% income tax. Since 2001, the Fed has remitted $1.36 trillion to the Treasury. This ended in September with the operating losses.

The Fed tracks the operating losses in the same liability account, “Earnings remittances due to the U.S. Treasury” (chart below).

At some point, either as QT shrinks reserves and RRPs enough, or if the Fed changes its interest rate policy, or both, the interest expense begins to decline, and eventually, the Fed will make profits again. Those future profits will be taken against the cumulative losses in this account. The Fed will not remit any profits to the Treasury until the cumulative losses have all been covered, and the account starts having a positive balance again.

Just to be clear, losses don’t matter to a central bank that creates its own money because it can never run out of money, and therefore it can never run out of capital. The Fed’s capital is set by Congress and it has not fallen since the Fed started making operating losses.

But for the government’s budget deficit, the missing remittances from the Fed, that were taken against the deficit, are an additional burden.

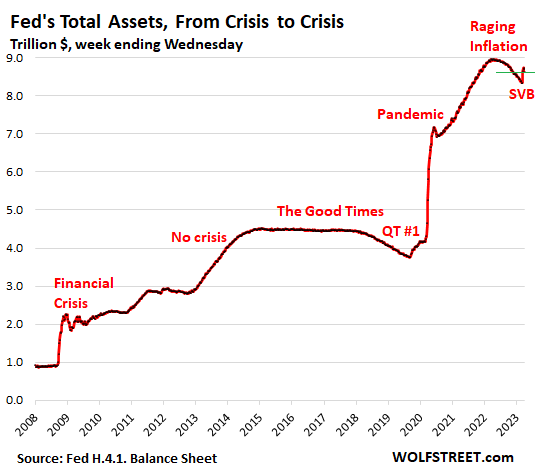

And here is the long-term chart of the Fed’s assets:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter April 6th, 2023

Posted In: Wolf Street