ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

August 27, 2022 | Your Inflation May Vary

John Mauldin

People who think about the economy are a non-random subset of the population. Most folks aren’t like us. Worse, we aren’t always like us. Hence the endless arguments.

Currently our subset is debating whether we face inflation or recession. In my view, it’s not an either/or question: We can have inflation and recession. That’s why I keep talking about “stagflation,” an economy afflicted with both problems.

Of the two, I think inflation is the more serious threat. I don’t minimize the pain many will feel from recessionary conditions. The difference is recessions have a lower limit. The economy can only shrink so much, then recessions end. Periods of inflation, if allowed to persist, can get infinitely worse and last a long time.

Everyone’s inflation experience is unique. We all have our particular spending patterns, so our experience will feel worse if inflation is more severe in the goods and services we normally buy. Or we might not notice it as much as others do. For example, if you already own your own home, you don’t really worry about housing inflation (unless you want to sell).

Similarly, inflation varies among countries, even those with close economic connections, due to the underlying causes and local policies. Today we’ll explore some of this international variation, drawing on new research from the Chicago Federal Reserve Bank, and then end with quotes from Jerome Powell at Jackson Hole, sounding like Paul Volcker.

Bottom line: Inflation as we see it in the US really is different.

Push & Pull

The idea that inflation comes in different flavors isn’t new. Keynesian theory recognizes “cost-push” inflation and “demand-pull” inflation as distinct phenomena. And while I find the Keynesian school lacking in other areas, those are useful concepts right now.

Cost-push inflation means rising input costs are making producers raise the price of their goods and services. Higher energy costs, for instance, reduce profitability for energy-intensive manufacturing and shipping. They don’t necessarily have to raise prices; they can choose to accept lower margins for competitive reasons. But when every producer’s costs are rising, customers eventually feel it—as they are now due to the effects of both COVID and the Russia-Ukraine War.

Conversely, demand-pull inflation happens when aggregate demand rises faster than supply. Or it could be that supply shrinks while demand holds steady. In either case, lower supply relative to demand means higher prices. We’ve seen this recently as COVID changed consumer preferences. People suddenly wanted more home-based food, entertainment, and other amenities than producers could provide. Then, as restrictions eased, people wanted more travel and restaurant meals. These aren’t insurmountable problems but adapting takes time across a large economy.

Cost-push and demand-pull inflation aren’t mutually exclusive. Both can occur at the same time in different goods and services. However, one or the other tends to predominate. In 2021, the inflation we had in the US was mostly of the demand-pull variety. That continued into this year, with the war adding cost-push energy and food inflation to the mix.

The interesting part is how other economies are seeing different patterns. Inflation varies much more than many observers think.

| A 2008 Rerun… Only Worse? Top economists say we’re headed for a deep recession—perhaps worse than the one following the Great Financial Crisis.Click here and find out how to protect yourself. (From our partners.) |

New to Us

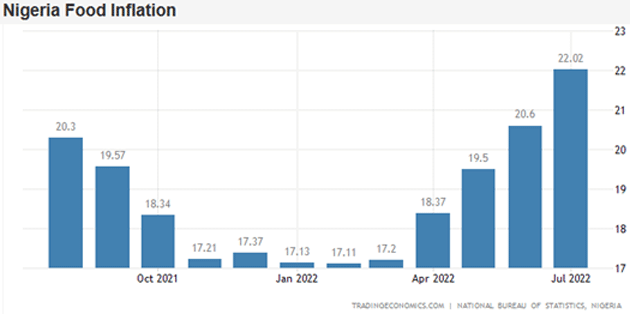

Let’s look at a seemingly obscure data point, one I sent to Over My Shoulder members two weeks ago (which you should join, by the way. It’s our lowest-priced letter but it gives you cream-of-the-crop articles and essays from my wide circle of friends and sources—material unlikely to cross your path. You are literally reading over my shoulder!). It shows year-over-year food price inflation in Nigeria.

Source: Trading Economics

As of July, food prices in Nigeria were up 22% from the same point in 2021. The comparable US change (CPI food category) was “only” 10.9%. Americans have it bad, but not like Nigerians. And many developing countries are in even worse shape.

Note, however, the chart’s y-axis is truncated at 17%. That makes pre-war food inflation look mild when it definitely wasn’t. The war simply aggravated Nigeria’s already-bad situation. Food prices there have been increasing at 10% or higher annual rates since 2016.

I show this to illustrate how the inflation we Americans find so troublesome isn’t new. It is new to us, or at least to those under age 55‒60. For a wide variety of reasons, global food supply has been lagging global food demand for some time, causing prices to rise. (Thankfully, the food exists, just at higher prices. The kind of famines that were so common a century ago are rare now. That’s progress.)

Would this inflation have reached the US if not for the pandemic and war? We can’t say for sure. I think it probably would have, though maybe not at the same magnitude. That’s an important point: Inflation isn’t hitting the world via a single on/off switch. It’s more like multiple sets of dimmer switches. An invisible hand is dialing them up and down, for reasons not always clear to us.

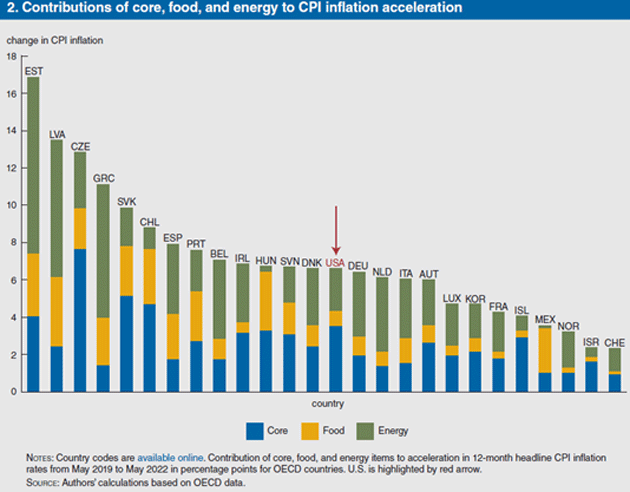

A recent Chicago Fed paper made some interesting comparisons in that regard. It looked at the change in inflation in various countries both pre-pandemic (May 2019) and the most recent available, which was May 2022. Note this shows the change between those two periods, not the actual inflation rate. The idea is to measure how much inflation rose, and why.

Source: The Federal Reserve Bank of Chicago

Each bar represents an OECD country (you can see the country codes here). The colors show how much of the change came from food, energy, and “core” inflation (i.e., everything except food and energy).

What you should notice is how much the impact varied between countries. The green (energy) portions of the bars range from tiny to huge. We hear that energy is a global market. Price changes should be broadly similar everywhere. Yet they are clearly not. The yellow food price contribution and blue core inflation change also vary tremendously between countries.

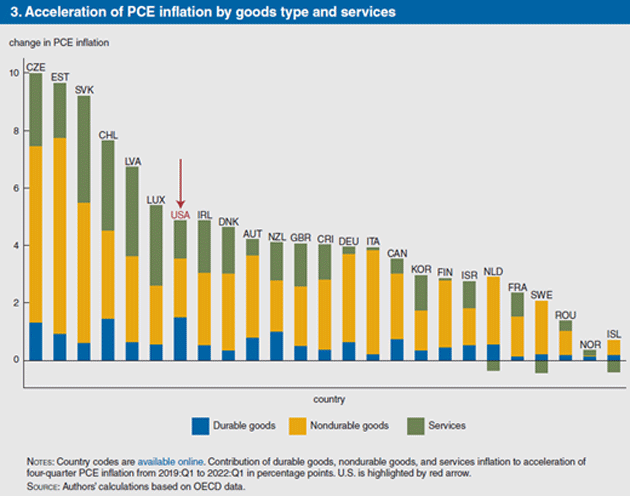

Here’s a different look, this time breaking down the core inflation change by durable goods, non-durable goods, and services. (Note this is PCE, not CPI.)

Source: The Federal Reserve Bank of Chicago

Note how the USA bar has the largest blue (durable goods) contribution. We’ll come back to that in a minute. The important point: Once you get past the noise, it seems there are two categories—countries where food and energy prices are driving inflation up, and countries where something else is the primary culprit.

Relative Impact

You’ll notice in both those bar charts the US is neither best nor worst. Our inflation is middle-of-the-pack compared to other developed countries. But this wasn’t always the case. Early in the pandemic, US inflation was running well above most of those same countries.

But looking at headline inflation obscures a lot of detail. The Chicago Fed researchers observed how food and energy prices have played a much greater role in Europe.

Unlike many European countries, the US is notable in that core items are responsible for more than half of its inflation acceleration, while food and energy play a comparatively minor role. Commodities, such as food and oil, are frequently priced in US dollars. Due to the recent depreciation of most global currencies against the dollar, these countries face greater commodity price pressures than the US. Further, the impact of energy on inflation acceleration varies across the sample due to differences in energy intensity. That is, a country that consumes more energy as a share of its total household spending will experience a greater impact of energy prices on its inflation rate.

First, note that this makes a strong dollar important in the inflation story. And if the dollar weakens, that will usually and incrementally raise prices, making the task of fighting inflation harder.

Another important and often-overlooked difference: The US is a net energy exporter. That’s why we enjoy relatively low fuel prices compared to, say, France or Germany. Most other OECD countries spend more on energy, which means they spend less on other things. When energy prices rose, their inflation rates rose more than ours, and vice versa.

Again, that doesn’t mean energy (and food) inflation hasn’t struck the US. It certainly has. We’re looking at relative impact, and it shows US inflation is more rooted in the “core” categories—and specifically in durable goods prices.

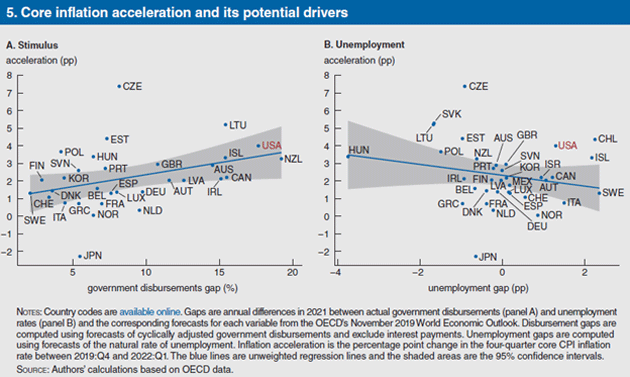

Here’s a very noisy chart I normally wouldn’t include, but it’s important. The left panel plots inflation’s change vs. the change in government disbursements over the same period. I’ll quote their explanation below the graph.

Source: The Federal Reserve Bank of Chicago

In panel A of figure 5, we plot the relationship between core inflation acceleration and fiscal stimulus. We see that countries with larger stimulus packages tended to experience greater inflation acceleration. Out of all countries that provide the relevant data, the U.S. enacted the second-largest fiscal stimulus with a disbursements gap of 17.6%, indicating that government spending and transfers increased sharply relative to pre-pandemic trends. This large fiscal stimulus may have driven the surge in US durables demand.

That supports what many of us expected: Huge injections of cash into the economy did what was intended, i.e., support consumer spending and employment. But they also had a cost, part of which we now see in the inflation rate.

The right panel of that graphic plots inflation vs. the change in employment (compared to pre-pandemic projections). Here’s the authors’ explanation.

In panel B of figure 5, we plot core inflation acceleration against the unemployment gap, or the difference between observed unemployment rates and pre-pandemic OECD forecasts for the 2021 natural rate of unemployment in each country. A positive unemployment gap implies that a country’s labor market has yet to recover from the pandemic recession. Across countries, the size of the inflation acceleration is negatively correlated with the unemployment gap, suggesting that differences in labor market slack account for a significant part of the cross-country variation in inflation acceleration. Panel B also reveals that the acceleration of inflation in the US is much higher than in other countries with similarly small but positive unemployment gaps. This suggests that, besides labor market conditions, other factors are also important in explaining the increase in inflation in the US.

“Differences in labor market slack” is a polite way of saying “unemployed people don’t spend as much.” But here the relationship is weaker, meaning other factors are also at work. What might those be?

Well, monetary policy should be high on the list. No central bank acted what I would call “responsibly” in this period, meaning they followed Bagehot’s Dictum and simply kept the banking system afloat. All, in various ways, sought to prop up their economies and protect locally powerful interests. Maybe that was appropriate in the initial COVID shock when we had no idea what we were facing. It quickly ceased being so, yet they continued pumping, none more so than the Federal Reserve. That’s why it now faces such a no-win choice between inflation and recession.

This also complicates investment strategy. Even if every central bank acts rationally, which they won’t, their responses will vary because their inflation situations vary. The global economy is both more interconnected and more fragmented than ever.

I think the economy will probably “muddle through” this time, enduring a lot of unnecessary pain but ultimately emerging (mostly) intact. But these are what my friend William White calls “complex systems.” I’ve called them “sandpiles,” prone to unpredictable but catastrophic breakdowns.

We don’t know what will happen, or where… which is why we must be ready for anything, anywhere.

Where Is US Inflation Headed?

The Commerce Department released its latest PCE inflation and consumer spending data this week. Essentially, consumer spending was flat for July. PCE inflation dropped to 6.3%, primarily on falling energy prices. Core PCE, excluding food and energy, was 4.6%, dropping from 4.8% the previous month. Note that the Fed prefers to look at PCE (personal consumption expenditures) rather than the CPI which generally shows higher inflation, mostly due to the heavier weighting of housing in CPI.

Bloomberg reported this on Thursday:

“Some of the world’s biggest bond investors say the market is wrong to expect central banks to score a long-term win in the war against inflation. There’s little doubt that interest rate hikes from policymakers in the US and Europe will pull consumer price increases down from the fastest pace in decades by slowing economic growth or setting off recessions.

“But the retreat of inflation from its peak isn’t likely to mark a return to the price stability of the recent past because of stark shifts in the world economy, according to a broad group of investors and strategists including firms from PIMCO, Capital Group and Union Investment.”

The participants in that conference, according to Bloomberg, think it will take a lot longer to get inflation back to 2%. These multi-trillion-dollar investors think that markets expecting a rate cut in 2023 will be sadly disappointed. And they are backed up by Fed officials, even those who are normally doves, giving increasingly hawkish speeches about the need to control inflation.

Bank Credit Analyst, one of my favorite sources which I have been reading for 30 years, is not entirely sanguine about the future. If inflation drops below 4% this year, they think a “Goldilocks” scenario of a soft landing is possible, but “the risk of a recession remains elevated.” Quoting:

“The disinflationary impulse from the July US CPI report is less compelling than it seems, in that it appears to have been mostly driven by declining energy prices. It is far from clear that energy prices will continue to decline over the coming months and are, in fact, likely to rise even if an Iranian deal takes place. This implies that investors may have jumped the gun in pricing in substantial disinflation and sharply higher odds of a Goldilocks economic outcome.”

BCA feels that energy prices over the longer term will rise as roughly 2 million barrels per day of Russian crude production stay off the market. Iran can’t replace the Russian exports even if a new nuclear agreement allows it.

There are clear disinflationary impulses in the markets. Supply chains are getting fixed, though some markets are better off than others. But as I have demonstrated in previous letters, inflation is likely to be at least over 5% by year-end and probably 6%. Over time, the year-over-year comparisons will begin to show lower annualized inflation, but still leave us with much higher prices than we had in 2019.

Living Longer with Mike Roizen

As long-time readers know, I go to the Executive Health Program at the Cleveland Clinic every few years. COVID interrupted that, so I finally went last week. They made up for lost time, doing a large number of rather intrusive tests.

Dr. Mike Roizen, who founded that program, has written 23 books that have sold about 28 million copies. Next month Mike will release what he feels is his most important book yet, The Great Age Reboot: Cracking the Longevity Code for a Younger Tomorrow. Go to Amazon or your bookstore and order an advance copy.

The new book goes into extraordinary detail on the latest research on postponing debilitating aging. He describes what you can do to actually reverse some of the effects of aging. He also explores how longer life spans will change our lives and our culture. This is the most comprehensive and forward-looking book on aging to date, showing readers how to prepare for the next major societal disruptor.

I have followed some of the researchers who worked with Mike on this book. The breadth of analysis is amazing. It’s a book you will definitely want to read.

First Jackson Hole Thoughts

As I wrap up this letter on Friday morning, I just saw Jerome Powell’s very hawkish Jackson Hole comments. I am simply going to quote some excerpts, while noting that he seems to want to bring on his inner Volcker (emphasis mine, quotes via Peter Boockvar and Axios).

“‘The FOMC’s overarching focus right now is to bring inflation back down to our 2% goal.’ He also implicitly critiques their own policy shift to inflation symmetry where they said they would tolerate a period of higher inflation above 2% to average out a period of below.”

“Our responsibility to deliver price stability is unconditional… There is clearly a job to do in moderating demand to better align with supply. We are committed to doing that job.”

“Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”

“…we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting.”

“Reducing inflation is likely to require a sustained period of below-trend growth,” Powell said, according to a prepared text. “Moreover, there will very likely be some softening of labor market conditions.”

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

“We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.”

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

John here again. That is the plan. Powell quoted his hero Paul Volcker who said in 1979, “Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”

He talks a good Volcker, but can he stick to it? If he does, kiss a soft-landing scenario goodbye. The Fed will raise rates until they break something.

British Columbia, Salmon Fishing, and Then?

Tomorrow I fly to British Columbia and stay at The West Coast Fishing Club. One of my personal bucket list wishes has always been fishing for big salmon in a remote resort-style fishing lodge. One of our clients, Jim Tosti, who has been going there for years, talked me into joining him and my friend and partner Steve Blumenthal for three days.

The only real problem is that getting to Vancouver is now much longer than traveling to Europe, basically taking 12 hours. I don’t seem to be able to sleep on planes, so I may have to catch up on the first day. And the weather forecasts a lot of rain. I don’t care, I just want that 50-pound Chinook salmon and maybe a halibut or two.

It is time to hit the send button. Because I will be in remote Canada, there will be no newsletter next week. It is Labor Day anyway and my extraordinarily hard-working and uniquely talented editorial staff deserves a break. You have a great week, and don’t forget to follow me on Twitter.

Your wondering what the next central bank policy error will be analyst,

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

John Mauldin August 27th, 2022

Posted In: Thoughts from the Front Line