Portfolio Manager and President of Venable Park Investment Counsel (www.venablepark.com) Ms Park is a financial analyst, attorney, finance author and regular guest on North American media. She is also the author of the best-selling myth-busting book "Juggling Dynamite: An insider's wisdom on money management, markets and wealth that lasts," and a popular daily financial blog: www.jugglingdynamite.com

Venture capital, private equity firms, and hedge funds (traditionally more hubris than hedged) used to be fringe players working with the high-risk pieces of ultra-wealthy portfolios.

However, as traditional investment yields (net rental, dividends and interest) tumbled through years of aggressive monetary intervention (zero interest rate policies and QE), individuals and institutions sought ‘alternatives’ for help. The money business ballooned on the opportunity to roll out increasingly complex, opaque products with rich rewards for sponsors and operators.

Venture (VC) and private equity (PE) groups typically direct capital into high-risk start-ups and private companies aimed at getting them to the next stage of funding and ultimately selling to a conglomerate or initial public offering (IPO). The timeline is typically years, and the long-run success rate for a company in their portfolio is maybe one in ten. For this reason, investor capital is illiquid, locked in for an uncertain duration and outcome.

On the other hand, hedge funds have traditionally directed their capital into more liquid publicly-traded securities that enabled their investors monthly or quarterly withdrawals. Over the last decade of low yields, their allocation choices shifted. In 2021 alone, hedge funds nearly quadrupled the annual number of private companies they invested in between 2010 and 2015, according to research by Goldman Sachs.

Many borrowed to increase leverage and magnify predicted gains. In a doomed daisy chain, they each allocated capital to many of the same entities, and funds were marketed to the general public.

As asset markets now tumble, liquidity evaporates, and the boondoggle is coming to a predictable close. Redemption requests are just starting to rise. The need for liquidity will drive the urge to sell what they can at inopportune timing. See Hedge Fund D1 Borrowed Billions for Hot Bet Now Seen Melting Down:

Across Wall Street, billionaire investors and their advisers are urgently trying to figure out how much exposure they have to plunging values in Silicon Valley unicorns and other private ventures. They’re reviewing disclosures by some of the most active buyers of those assets, including D1, Tiger Global Management, Coatue Management, Lone Pine Capital and Viking Global Investors.

Clients had been giving their money managers more leeway to buy assets that can be hard to value and slow to sell. Some firms used leverage to boost returns.

Yet valuations of many closely-held companies are tumbling even harder than the technology stocks that slumped on public markets this year. That has left hedge fund investors trying to figure out whether their money managers might suspend withdrawals, face demands from lenders to post more collateral, or — in a worst-case scenario — have to start selling investments quickly enough to drive down asset prices in a chain reaction.

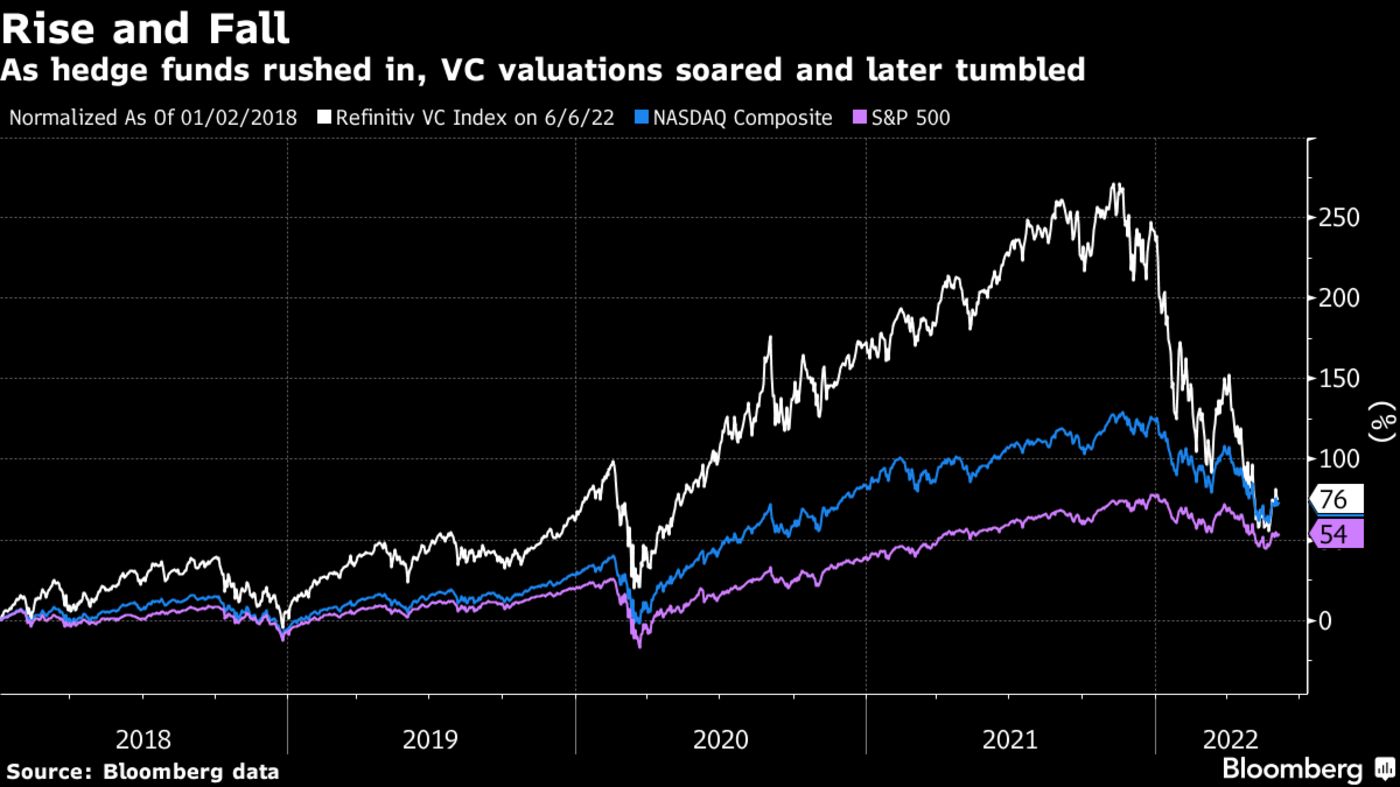

Valuation declines are starting to come into focus. Venture capital firms have watched their holdings slump enough to push the Refinitiv Venture Capital Index down 47% this year — more than double the 22% slide in the Nasdaq Composite Index of publicly traded stocks.

The recent acquisitions are part of a wave of increased activity from private-equity firms across the globe, as they search for new fields to generate yield by consolidating fragmented industries and extracting profits. In Canada, consolidators have spent billions in sectors as varied as waste management and legal software.

The approach has fuelled greater corporate concentration, which critics say will reduce consumer choice and drive up prices by driving down competition. And private-equity’s drive for efficiency could also affect the quality of care, for example by reducing the time a professional can spend on procedures.

Private-equity firms including Stockbridge Capital, Carlyle Group and Apollo Global Management have been rapidly buying up mobile home parks over the last decade, often using funding from government-sponsored lenders Fannie Mae and Freddie Mac. Once they take over, one of their first moves is to raise rent…”

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio

delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.