ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 17, 2022 | Soaring Rents Eat Americans’ Wage Increases – And Then Some

John Rubino

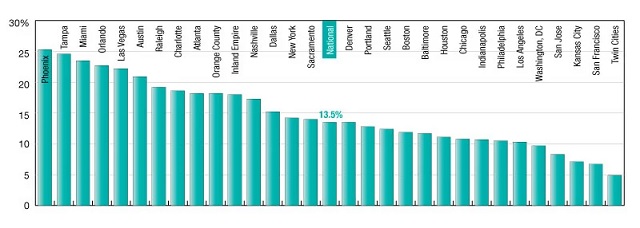

US headline inflation exceeded 7% in 2021. But rent increases put the Consumer Price Index to shame, soaring an average of 13.5%. And within that already-brutally-high average, there were some absolutely astounding outliers. Phoenix rents soared 25.3%, followed by Tampa, Miami, Orlando, Las Vegas, and Austin, all of which exceeded 20%.

That means an Austin barista could receive a 10% salary bump and have most of it wiped out just by an increase in their rent. Add in the soaring costs of food and gasoline, and our hypothetical worker is actually losing ground despite their double-digit pay raise.

A confluence of things

Rents do tend to rise a bit each year, with 3%-4% being typical. So how did 3% become 20%+ in so many markets? A confluence of factors, including:

Rent forbearance. State and federal programs designed to prevent evictions during the worst of the pandemic lockdowns hit landlords – who have loans of their own to pay off and can’t do so without rental income – especially hard. Many are now raising rents where they can to offset where, for over a year, they couldn’t.

General inflation. Pretty much everything required to manage rental properties – including construction materials, labor, and electricity – is up, in some cases dramatically. To stay solvent, landlords have to pass on at least some of these costs to tenants. So 7% headline inflation equals (at least) a comparable increase in rents.

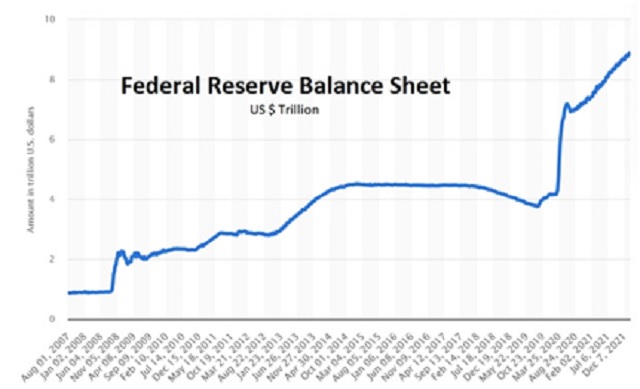

Soaring home prices. As the world tipped into pandemic-induced recession in 2020, governments responded with an epic money-printing binge. The Federal Reserve’s balance sheet – a proxy for the number of newly created dollars the central bank has created and dumped into the economy – has more than doubled since 2019. Expressed another way, 40% of all the dollars ever created came into being in the first two years of the pandemic.

Combine this tsunami of new money with artificially low mortgage rates – another side effect of QE – and the result is soaring home prices. This impacts the rental market in two ways: First, more expensive houses price ever more would-be buyers out of the market, thus increasing the pool of renters competing for a limited supply of available units. Second, a rental house bought at today’s higher price requires more monthly income to cover its costs, which ratchets up rents.

Wall Street. Private equity firms and investment banks developed a taste for rental property during the Great Recession, and now they’re back for the main course. The vast majority of apartments sold in recent years have been gobbled up by Wall Street:

From ProPublica’s When private equity becomes your landlord:

Private equity firms often act like a corporate version of a house flipper: They seek deals on apartment buildings, slash costs or hike rents to boost income, then unload the buildings at a higher price.

The companies’ size allows them to influence market rates and lobby against reforms that could dilute their power. And their goals — quickly hiking a building’s profits so they can sell it at a premium — are often at odds with those of the tenants who need to live in them. In contrast, so-called mom-and-pop landlords usually look for steady streams of rental income over time while their buildings grow in value.

And the sharks are still hungry:

The deal includes more than 40 rental apartment properties including 12,000 units in states including Florida, Tennessee and Georgia. Preferred Apartment also owns 54 grocery-anchored shopping centers anchored by grocery stores. About 70% of the deal’s value is in its rental apartments.

Blackstone has been aggressively ramping up its bet on U.S. rental housing. The firm has agreed to buy two other companies that own apartments in the past two months, building up its presence in states including Colorado, Texas, Arizona and Georgia.

Multifamily properties particularly in high-growth Sunbelt states have been one of the hottest commercial property types in recent years because businesses have been relocating to those regions. Owners have been able to raise rents well above the inflation rate throughout the Covid-19 pandemic.

Blackstone, the world’s largest commercial property owner and until recently America’s largest landlord after scooping up tens of thousands of single-family homes in the aftermath of the 2009 subprime mortgage crisis, has been feverishly working to regain the title by bidding up rental apartments for years. The firm is purchasing Preferred Apartment through its largest fund, Blackstone Real Estate Income Trust, which has raised more than $50 billion since it started five years ago and mostly targets individual investors

It’s a similar story in rental houses, where private equity firms have taken to swooping in and buying entire neighborhoods at above-market prices, then converting the houses to rentals at inflated rates.

The implication? With market power firmly on the side of our new corporate landlords, rents aren’t coming down anytime soon. Just the opposite.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

John Rubino February 17th, 2022

Posted In: John Rubino Substack