ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

November 14, 2021 | Live from New York, Etc.

John Mauldin

I am writing in the middle of a whirlwind week in New York. We are going to discuss what I’m learning, some takeaways from the conversations I’ve had, changes in my personal portfolio, and thoughts around the topic of the day: inflation. As well as a few random things that I have read this week. All delivered to you within my 3,000-word limit. Let’s jump in…

Changes in My Personal Portfolio

Recently I’ve mentioned some changes in my own investments. This generated questions from readers who want to know more. So now is a good time to elaborate.

Years ago, my partner in our money management business, Steve Blumenthal of CMG, and I developed what we called the 80/20 portfolio. Conceptually, that means 80% of your portfolio goes into core positions intended to grow to 100% of the original portfolio in five years. These are typically nonaggressive cash flow and similar products yielding somewhere in the 5% neighborhood.

We then position the other 20% to “explore” stocks and assets able to grow at a much faster pace, albeit with more risk. Think technology, certain real estate positions, etc. You spread your risk over multiple such positions, taking a longer-term view but watching them closely.

The 80/20 split is a guideline, not a hard and fast rule. The older and less risk tolerant you are, the more you allocate to core positions. Younger investors with good income might think more along 70/30 lines—realizing that your business and/or job is a key risk as well.

Now, this is a “do as I say not as I do” description. Five years ago, my own portfolio was probably more like 70/30. That was a bit aggressive for somebody then in his mid-60s, even though my income stream was comfortable. Given my personality and access to deal flow, it seemed quite reasonable.

Today, my portfolio is about 40/60, for good reasons. My explore portfolio has done very well over the past few years. It will come as no surprise to long-term readers that the bulk is in biotech. It’s where I somehow have access to deal flow, familiarity with the technology, and a really exceptional team of advisors/friends. I admire people like Cathie Wood and Ron Baron who can source and understand technology and businesses over a wide array of opportunities. I let managers like them source “explore” technologies in AI, robotics, etc. I’m enthusiastic about the entire space, but I simply don’t have the personal ability to drill down and figure out who’s going to be the winner. Everybody talks a good game, but only a few managers actually get the ball past the goal.

There is a school of thought that says I should rebalance. I could do so, but I simply have no real reason to, at least currently. Most of the companies I own are still in the growth stage. There’s one, still private but my largest single position, that I put a great deal of due diligence on. I believe in the management team and their technology. To the point that I have told Shane that if something untoward happens to me, don’t sell that stock until Steve Blumenthal does. Everything else is fair game but I think this is my personal bet on a long-term monster multiple. I think it is just on the cusp, even though we’ve already seen some very nice growth in the last few years.

If I were starting today, my portfolio would probably look closer to 80/20. My core allocation has averaged mid- to high single-digit returns for the last seven years. Much of it is in a variety of multi-strategy hedge funds, which may sound risky simply because of the word hedge fund, but are actually fairly boring mainstream fixed income substitutes. We have been able to track it as a portfolio since 2014. My worst year was -0.2% and my best year was, well let’s just say really good as everybody hit a homerun that year. I don’t expect to repeat that very often.

I do have one fairly aggressive hedge fund, whose manager I personally know very well. I told him recently that one of my biggest mistakes was not giving him more money. I knew when he launched his fund about five years ago it would be volatile, and it has been—40% drawdowns have been common. But the up years have been very, very good. That was less than a 2% position when it started. Now it’s closer to 7–8% and I actually think about rebalancing, but he is in a drawdown. I hate to take money from what I ultimately think is a very good winner and I like his current positioning. But at some point…? (By the way, he is closed to new money, and he is too volatile for me to recommend to clients. I don’t want to have to hold someone’s hand in a 40–50% drawdown. Some months I don’t even look at the monthly returns, trying to focus more on the quarterly and annual returns.)

My point is not to encourage taking more risk, especially at this point in the market, but to get you thinking about creating your own core positions so you can feel comfortable taking a few “explore” options. The key is having a core portfolio that is adequate to sustain Shane and me. If it weren’t, then the level of my current explore portfolio would be irresponsible. Yet my explore portfolio has grown to the size it has, position-wise, organically, for all sorts of good reasons. I should note that I certainly don’t hit 100% in my riskier choices. I’ve had my share of goose eggs, more than I want to think about. Which is why I’m a little bit pickier about my explore choices today.

Just food for thought as over the last few weeks I have been talking with the management of some of my explore choices and it is at the top of my mind right now.

Whither Inflation?

I have had numerous meetings and discussions about inflation over the past few weeks. It is clearly the hot topic. I’ve written about it a little bit over the last few months. I’ve also been able to talk with a number of analysts and researchers this week in New York.

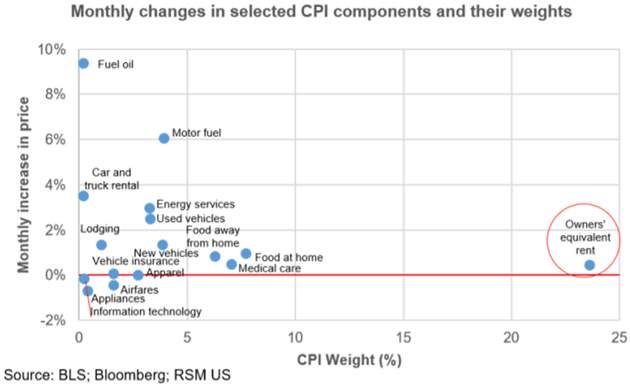

Let me go out on a limb and say the chance of an 8% handle on CPI inflation in the first quarter of 2022 is nontrivial. As my friend Peter Boockvar noted, it becomes harder in April and May 2022 to show high year-over-year inflation as it was already at 4% at those points in 2021. Here’s a chart and some thoughts by Joseph Brusuelas at RSM (which we shared with Over My Shoulder members this week).

“A deeper look at the data shows that the increase took place primarily in the sectors of the economy hardest hit by the pandemic, implying some relief ahead as supply-chain bottlenecks are undone. The Fed will not be so concerned about these factors, many of which will abate in the coming months.

Source: RSM

“But the second straight 0.4% increase in owners’ equivalent rent—up by 3.1% on a year-ago basis—requires scrutiny by policymakers. The inflation that flows through this component and the broader shelter sector tends to be more persistent than the increase in the volatile food and energy components and in the pandemic-impacted industrial supply space.”

Source: RSM

Note that inflation early last year was quite low. So the year-over-year comparisons give us the current 6.1% inflation we have today and could easily grow to 8% in January and February, especially if the OER (owner’s equivalent rent) is properly accounted for.

(Sidebar: OER as a measurement tool for inflation is simply broken. We need a better measure. Bad measurements end up in bad policy, as we saw with the Fed not reducing QE and raising rates earlier this year.)

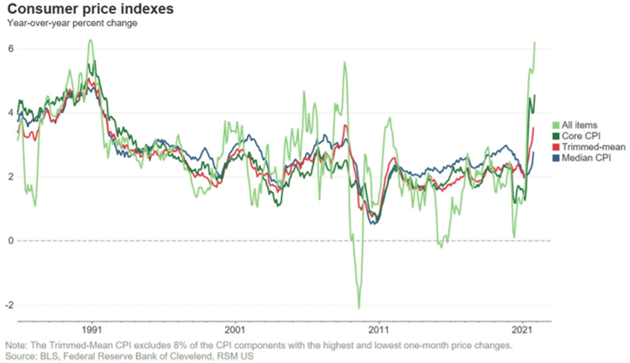

“So inflation is back to where it was in Oct/90 and July/08. Guess what? The economy was recession-bound both times, the Fed’s next move was not exactly to raise rates and Treasury bond yields plunged in the coming twelve months (and by a lot!). Bob Farrell’s Rule #9 reigns.”

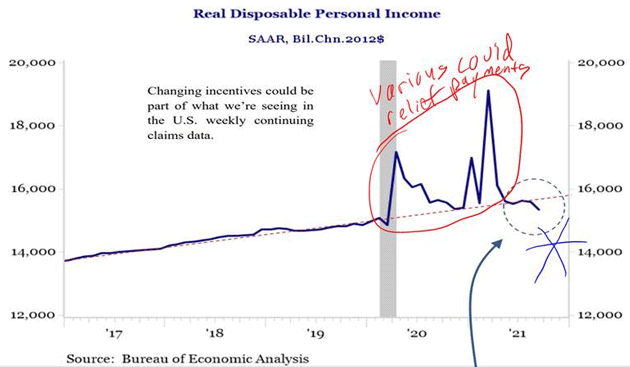

The economic growth we’ve seen came not from the Fed and quantitative easing but from the massive fiscal stimulus provided by Congress, leading to the current inflation. Now that it is mostly spent, future growth will be inhibited. My friend David Bahnsen sent this chart:

Source: David Bahnsen

This is not the stuff that 3% GDP dreams are made of. It should give us pause in our exuberance of hopefully being past the COVID crisis, that the real economy is still governed by supply and demand, and demand depends on income.

I think it is quite possible we will have a very low-growth 2022 accompanied by uncomfortably high inflation. Fed officials are way behind the curve. They have now painted themselves into a corner. How do you tighten to the extent needed when GDP growth is only 1–2%?

An entire generation of portfolio managers and investors have never dealt with inflation, except in the theoretical context of an economics book. Inflationary periods have often not been kind to stock market investors. I literally have no idea what Jerome Powell (assuming he is reappointed) will do. He will only have bad choices. Doing nothing is a bad choice. Reducing QE, let alone raising interest rates, will likely prove uncomfortable for markets, to say the least. I would have your hedges and portfolio positioned for a lot of volatility over the next 14 months.

There’s No Free Lunch

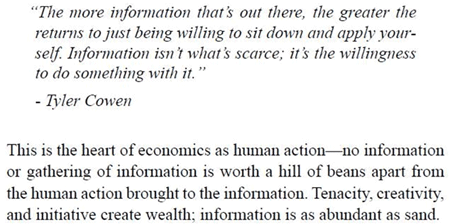

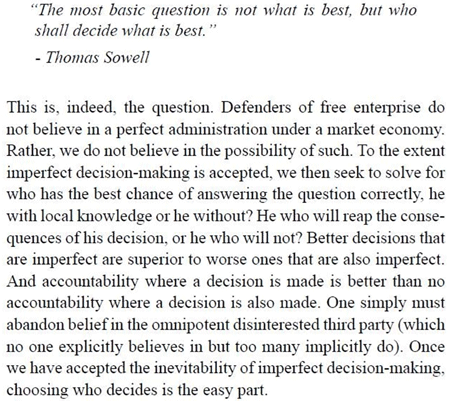

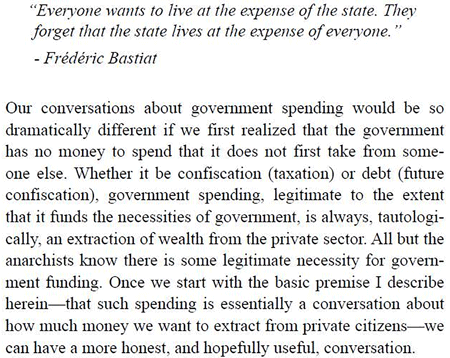

Speaking of David Bahnsen, Tuesday night I was at his book launch party. He’s written a brilliant collection of 250 quotable economic thoughts throughout the centuries, with his own commentary appended. The short quotes are all sound economic thinking in today’s world of very dangerous ideas. The book is called There’s No Free Lunch .

One of the quotes is actually mine.

Source: David Bahnsen

A few other samples:

Source: David Bahnsen

Source: David Bahnsen

Source: David Bahnsen

Some Interesting Data on Viruses

I read a wide variety of letters and research. Recently, Justin Stebbing pointed me to the fascinating question of whether viruses are actually “alive.” Can you put them somewhere on the tree of life? It’s a very complex and controversial subject. But this part really struck me:

“An estimated 10 nonillion (10 to the 31 st power) individual viruses exist on our planet, enough to assign one to every star in the universe 100 million times over…

“Yet, most of the time, our species manages to live in this virus-filled world relatively free of illness. The reason has less to do with the human body’s resilience to disease than the biological quirks of viruses themselves…

“These pathogens are extraordinarily picky about the cells they infect, and only an infinitesimally small fraction of the viruses that surround us actually pose any threat to humans.

“Still, as the ongoing COVID-19 pandemic clearly demonstrates, outbreaks of new human viruses do happen—and they aren’t as unexpected as they might seem.” ( National Geographic ).

That speaks to the fragility of life. But before you begin to obsessively wash your hands and decide to live in a clean room, here’s a bit of good news from two young Australians who write a rather quirky newsletter called Future Crunch . They highlight good news from around the world that you just don’t read about. I like reading them just to make myself feel good.

This week they had some rather good news on the virus front, which probably didn’t make it to your inbox:

“One of the four major flu viruses that circulate in humans [in Australia at least and maybe the world— JM ] might have gone extinct thanks to the COVID-19 pandemic. The Yamagata virus has not been detected since April 2020 anywhere in the world. Together with the Victoria virus, it used to be responsible for somewhere between 290,000 and 650,000 global deaths every year.” ( ABC )

Thanksgiving and More Travel

Shane and I will head to Dallas for Thanksgiving and I’m already starting to plan a return trip to New York and a few other cities. I really enjoyed this whirlwind week. Some thoughts on my trip:

New York’s crowds, traffic, tourists, and restaurants are finally back. And for me at least, it was good to find a lot of friends, both old and new, in the investment world to be able to share ideas with.

Sunday and Monday were filled with meetings. We closed out Monday evening with a client dinner at Bobby Van’s. One of our guests pointed out that JP Morgan’s bank vault was underneath Bobby Van’s. With a few polite questions, we were led outside and down to an extraordinarily large bank vault, with all the drawers and numerous side vaults, taking me back to what it was over 100 years ago, imagining what it would’ve been like to be in J.P. Morgan’s office during the Panic of 1907.

Source: John Mauldin

Tuesday was an all-day meeting with my partners Olivier Garret and Ed D’Agostino talking about Mauldin Economics. We have done much better than expected the past two years and we will launch some very exciting new programs in the next few quarters as well. One of the best decisions I’ve ever made was when I decided I am simply “talent” and should let management run the business. My life is so much better and simpler. The business is run much better, too.

Wednesday at lunch I met with my good friend Ian Bremmer and Andrew Yang for a fast-paced 90 minutes. Any discussion with Ian is always full of fascinating insights, but Andy is just a powerhouse full of ideas. He has a new book called Forward: Notes on the Future of Our Democracy . He is quite passionate about developing an alternative to the two-party system, which will be an uphill battle, but frankly, a few additional choices might help. Interestingly, he wasn’t arguing for his own candidacy but rather that there needs to be a platform for others to run. I won’t mention the names he dropped, but they would make for an interesting, if not entertaining, 2024 race.

Wednesday night I had dinner with David Bahnsen and Sam Rines, Thursday meetings with potential clients and friends, and then dinner with a host of friends capping off an incredible five days in New York. As you read this, I will be back in Puerto Rico. You have a great week and spend some time with friends if you can.

Your getting ready to talk about economics and inflation analyst,

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

John Mauldin November 14th, 2021

Posted In: Thoughts from the Front Line