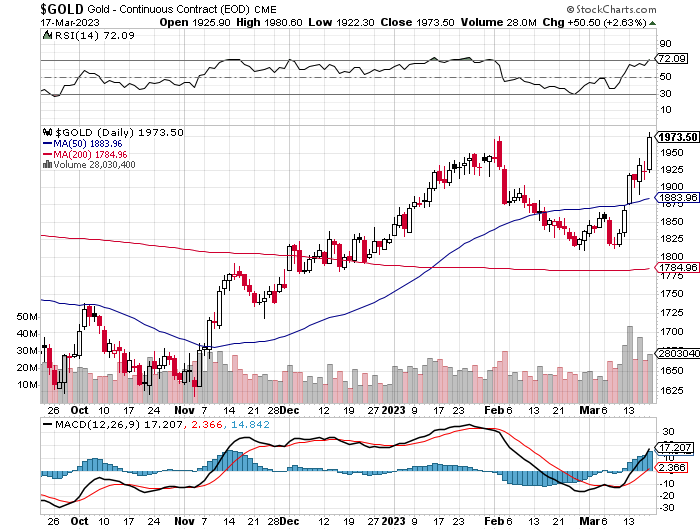

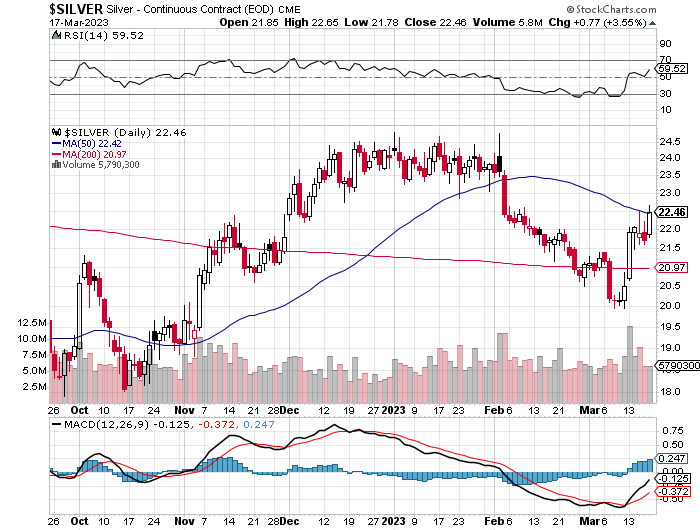

| According to Nick Laird’s data on his website, there has been a net 889,500 troy ounces of gold removed — and a net 32.70 million troy ounces of silver was also taken out of all the world’s known depositories, mutual funds and ETFs during the last four weeks. Despite the rallies over the last week and a bit, all gold ETFs and mutual funds, with the odd minor exception, have been shedding gold like mad over the last four weeks. This is particularly true of the COMEX…down 451,000 troy ounces, iShares/IAU…down 152,000 troy ounces — and UBS, down 255,000 troy ounces. In silver — the biggest drop was in SLV inventories, down a whopping 27.035 million troy ounces, followed by the COMEX, down 5.160 million troy ounces. After them came SIVR, down 1.816 million troy ounces…and 843,000 troy ounces out of iShares/SVR. Retail bullion sales have exploded around the world. Most the available inventory has vanished — and higher premiums have returned. I have a bit more about this in The Wrap. The physical shortage in silver at the wholesale level continues unabated and at an ever-increasing rate….as just pointed out above, with the 19 million ounces out of SLV over the last three days being the poster child for that. How much silver is left in these depositories that is available for sale at current prices is something that Ted has been going on about for a long while now — and he’s of the opinion that there isn’t a lot. Whatever that number is, we got a lot closer to it this week. The vast majority of precious metals being held in these depositories are by those who won’t be selling until the silver price is many multiples of what it is today. That’s particularly true of PSLV. Not only is there an obvious shortage in wholesale silver, but the fact that central bank gold demand exploded to 1,136 tonnes last year, means that there’s a lot less gold in good delivery form around too. That amount, plus the 551 tonnes that was reported being held by Russia’s sovereign wealth fund a month or so ago, most likely means that the wholesale physical market in gold is getting tight as well. It’s a good bet that it’s gotten a lot tighter in the last ten days because of the banking crisis. Turkey’s purchases of 68+ tonnes in January — and another 57+ tonnes in February, is an indication that the central banks of the world are still at it. I’ll certainly be interested in the next report that comes out of the World Gold Council. And as you’re more than aware, this extraordinary demand in both of these precious metals has not yet been allowed to manifest itself in their respective prices. The Big 4/8 commercial shorts still have them in their iron grip…but that iron grip slipped a lot yesterday. And there’s still this not so little matter of the 36.28 million shares currently sold short in SLV. That’s down only 1.78% as of the last published short report on March 9. Ted thinks that whoever is depositing silver into SLV recently, has to have leased it from JPMorgan…as they and their friends are the only ones that have that quantity of silver that they’re willing or able to part with, but with obvious strings attached. I know that he is going to have a lot to say about this in his weekly review this afternoon. The next short report is due out on Friday, March 24…for positions held at the close of business on Wednesday, March 15 — and when that shows up, we should learn more. But because of those big withdrawals in the last few days, Ted is of the opinion that whoever is short SLV, is short a lot more now, as there haven’t been any big deposits into SLV for awhile, so they’re shorting the shares in lieu of depositing physical metal. Then there’s that other little matter of the 1-billion ounce short position held by Bank of America…with JPMorgan & Friends on the long side. Ted says it hasn’t gone away — and as he pointed out, the latest OCC Report, for positions held at the end of September, shows that it’s still there, but now hidden by their market-neutral spread trades in gold. The latest OCC Report, for positions held at the end of Q4/2022 won’t appear for another week or so. |