ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

August 28, 2022 | QT at the Bank of Canada: Assets Down 24% from Peak. Spiraling Losses on Bonds, to Be Paid for by Canadians

Wolf Richter

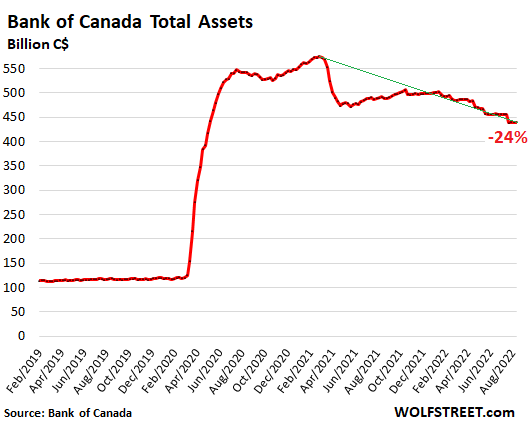

On the Bank of Canada’s balance sheet released Friday, total assets of C$439 billion were down by 24% from the peak in March 2021 (C$575 billion). By comparison, the Fed’s balance sheet peaked in April 2022. The BoC’s Quantitative Tightening (QT) started in essence in April 2021 and is way ahead of the Fed’s QT. We’ll get to the details and the funny-looking shape in a moment:

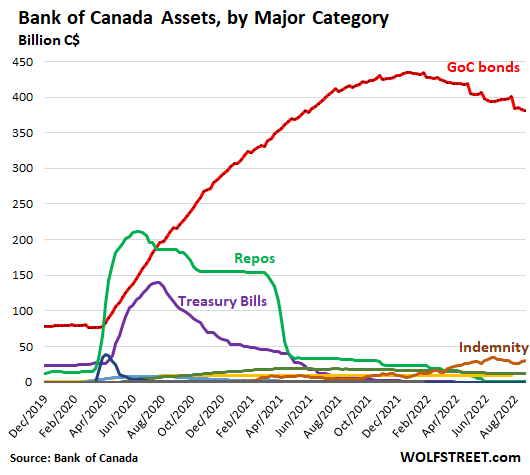

Biggest categories of QE assets, gone or rolling off:

Repos: The BoC’s repo holdings peaked in June 2020 at C$210 billion, and then started unwinding. Most of them were gone by June 2021, and by June 2022 nearly all of them were gone. Now just C$400 million are left over, waiting to mature (green line in the chart below).

Canada Treasury bills: The short-term Canada Treasury bills that the BoC started purchasing in March 2020 peaked in July 2020 at C$140 billion. At that point, the BoC started to let them roll off the balance sheet when they matured. In March 2021, it announced that it would let them and repos go to zero, citing “moral hazard” as reason. By September 2021, the Treasury bills were mostly gone. By April 2022, they were totally gone, and remain gone today (purple line).

MBS: The BoC never bought a lot of these “mortgage bonds” to begin with. They peaked at just under C$10 billion in late 2020. In October 2020, the BoC said it would end buying MBS entirely, worried about the Canadian housing bubble. They have since then diminished due to the pass-through principal payments and remain a very small item, down to C$9 billion (yellow line).

Government of Canada (GoC) bonds: This is the biggie, the prime QE tool. In October 2020, the BoC announced that it would reduce its purchases of GoC bonds from C$5 billion a week to C$4 billion a week – but don’t call it “tapering,” it said at the time, though it was plain-old tapering.

In April 2021, by which time it held 40% of the outstanding GoC bonds, it reduced its purchases of GoC bonds to C$3 billion, citing “signs of extrapolative expectations and speculative behavior” in the housing market. In July 2021, the BoC reduced its purchases to C$2 billion a week.

In October 2021, it put the hammer down. In a surprise move, with inflation surging, it announced that it would end its purchases of GoC bonds entirely, beginning November 1, 2021, and would allow maturing bonds to roll off without replacement. There are no “caps” on the GoC bonds that roll off. Whatever matures, rolls off. The surprise announcement caused yields to spike.

This was the beginning of its official QT though total assets had already dropped a bunch because repos and Treasury bills had mostly vanished.

The BoC’s holdings of GoC bonds peaked at the end of December 2021 at C$435 billion and have in the eight months since declined by 12.6%, or by $54 billion, to $C381 billion (red line).

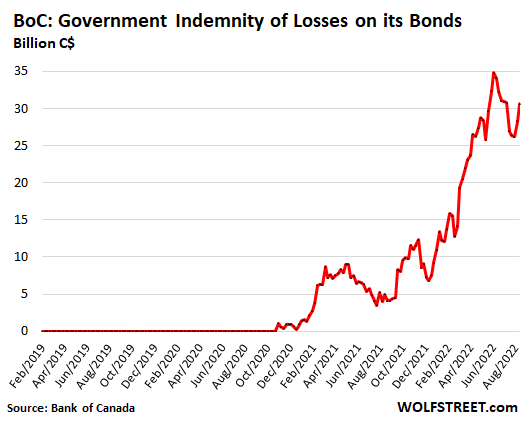

“Indemnity:” Losses on its securities holdings.

Note the brown line in the chart above – now the second-largest asset, “Indemnity.” This is the estimated value of the indemnity agreements between the federal government and the BoC. It represents the estimated losses from the securities holdings of the BoC if it were to sell them at current prices, which it would then be reimbursed for by the federal government.

As part of this QE craziness starting in March 2020, the federal government agreed to indemnify the BoC for any actual losses incurred on its bond portfolio. These losses were expected to pile up when bond yields begin to rise, as they’ve been doing since early 2021.

The BoC sets up the estimate of the losses as an asset on this balance sheet. If the BoC actually gets paid from the government for these losses, the amount is reduced by the reimbursement. This account is a form of a receivable, owed to the BoC by the federal government, for the losses on the bond holdings.

When yields rise, those losses rise. When yields fall, the losses decline (all bondholders experience that). During the bear-market summer rally that lasted in Canada, as well as in the US, from mid-June through mid-August, yields fell and bond prices rose.

But this rally ended in mid-August. Since then, yields have been rising and bond prices have been falling, and the estimated losses have also been rising again.

The chart below shows the detail of those estimated indemnities, based on the estimated losses. These indemnities peaked on the balance sheet dated June 15 at C$35 billion. Then, as yields fell and as losses fell, the value of the indemnities fell also, bottoming out at C$26 billion on the balance sheet dated August 10. Then they took off again. On the balance sheet dated August 24, released on Friday, they jumped back to C$31 billion:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter August 28th, 2022

Posted In: Wolf Street

Next: Bozo-dom’s Friday Frisson »