ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 8, 2022 | Used Vehicle Prices Finally Hit Resistance, at Ridiculous Levels

Wolf Richter

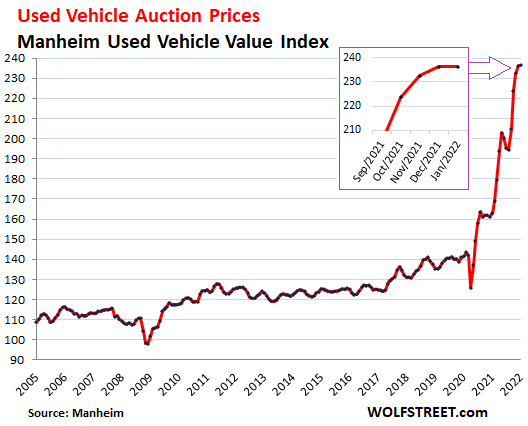

Used car and truck wholesale prices that had gone berserk last year were essentially flat in January, the first hesitation since August, at ridiculously high levels, as pricing resistance in face of this craziness is finally setting in.

Two months ago, I noted the first signs of softening of some of the beneath-the-surface pricing-dynamics. And a month ago, I noted how this softening beneath the surface expanded in December. And in January, the softening broke the surface just a tad with flat prices for the first time in months, halting the mind-boggling spike of the Manheim Used Vehicle Value Index.

There had already been indications last summer that these prices-gone-berserk had turned around and were heading south, but then the next leg of the spike set in.

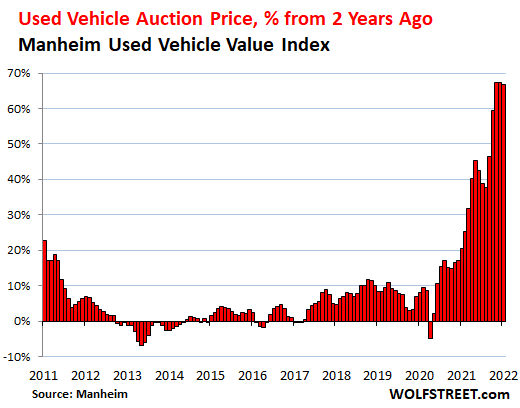

These wholesale auction prices, as tracked by Manheim’s seasonally adjusted and mileage-adjusted Used Vehicle Value Index, were still up by 45% from January 2021, and by 67% from January 2020.

This doesn’t mean that used vehicle prices will suddenly plunge. Prices are sticky on the way down. But it indicates that price resistance is setting in, amid plenty of supply and slightly lower sales at those ridiculous prices.

The underlying softening progressed further in January.

The Three-Year-Old Index declined 2.9% in January, according to Manheim, the largest auto auction operator in the US and a unit of Cox Automotive.

The average daily sales conversion rate at Manheim auctions declined to below-normal 50% in January. For example, in January 2019, the sales conversion rate averaged 51.5%.

“The lower conversion rate indicates that the month saw buyers with slightly more bargaining power for this time of year, and as a result, most vehicles showed price depreciation,” Manheim said.

“However, price patterns in the month varied by vehicle age and segment. Older vehicles were more likely to see price stability, while younger vehicles tended to see larger declines,” Manheim said.

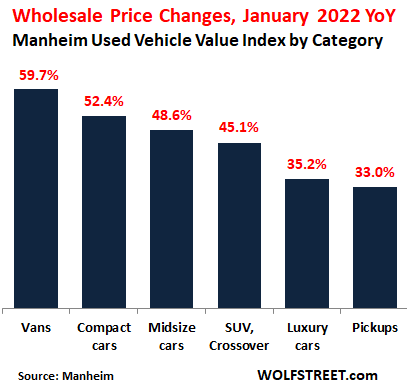

While month-to-month price declines were cropping up, the year-over-year price spikes remained enormous, and across all major vehicle categories, vans at the top with a price spike of nearly 60%, powered by super-hot demand for cargo vans on the used-vehicle market, driven by the boom in ecommerce delivery fleets.

The spike in van prices started when cargo vans — fleet sales in general — were deprioritized by automakers that got caught by the chip shortages and prioritized their high-margin retail sales. For example in January, fleet sales by automakers plunged by 48% from a year ago, sending fleets scrambling to the used vehicle market.

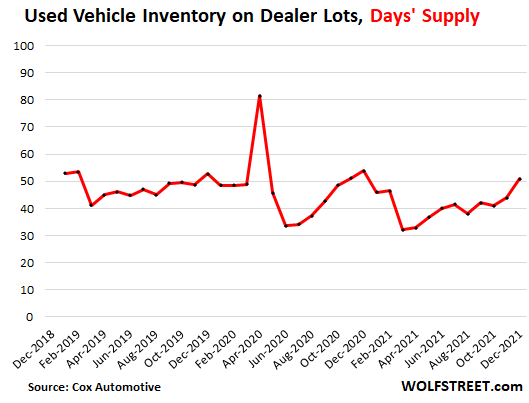

January started out with plenty of supply on retail lots and in the wholesale system, thereby reducing the pressure on dealers to purchase vehicles at auction at no-matter-what-prices, which is what we’re starting to see.

Supply at wholesale auctions at the beginning of January was 26 days, above the average of 23 days.

The number of used vehicles on dealer lots at the beginning of January reached 2.38 million vehicles, the highest since February 2021, which amounted to about 51 days of supply, compared to an average supply in 2019 of 48 days, according to data from Cox Automotive.

That there is plenty of supply at the current rate of sales simply means that dealers on average are not awash in inventory, and they’re not facing shortages either, though some hot models are hard to get.

And retail customers shopping for a vehicle will find choices – and ridiculously high prices.

The used-vehicle price spikes of last year are a historic and mind-boggling phenomenon without precedent in our lifetimes. How this gets worked out will make history: Whether prices ease off somewhat, only to consolidate and then start rising again but somewhere near the rate of CPI inflation; or whether prices drop sharply toward long-term trend; or whether prices suddenly take off again for that fourth leg of the even more ridiculous spike. The first scenario seems the most plausible; the third scenario seems unlikely, given where prices already are.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter February 8th, 2022

Posted In: Wolf Street