ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

October 16, 2021 | Banks Disclose Tidbits of Hidden Stock Market Leverage, as Known Stock Market Leverage Surges

Wolf Richter

No one knows how much total leverage there is in the stock market. Only fragments are reported. Margin loans are reported monthly, and they provide a general idea of the trend in stock market leverage. Some types of leverage are not disclosed at all until something implodes spectacularly, such as Archegos. Other types of leverage are reported in bits and pieces, if at all, by a few banks and broker-dealers in their quarterly financial statements, if they so choose. This includes “securities-based lending.”

Some banks & brokers report securities-based lending, others don’t.

On Thursday and today, some Wall Street banks and broker filed their Q3 earnings reports and supplemental information with the SEC, and a few of them included in their supplemental filings some tidbits about their securities-based lending (SBL).

Securities-based lending is hot; people who want to cash out some of the gains in their portfolios – thank you halleluiah, Fed – but didn’t want to sell, can use their portfolios as collateral for loans by the broker, the proceeds of which can be used for anything – buy more securities, buy a house or a new vehicle, or pay for a divorce settlement.

When asset prices fall enough, the borrowers get a margin call and either have to either come up with some cash and put it into the account, or they have to sell securities and pay down their SBL balances, thereby turning into forced sellers.

Goldman Sachs didn’t disclose anything about its SBL; they’re lumped into a larger loan category.

JPMorgan didn’t disclose the amounts either but only said that in its Asset & Wealth Management division, “loans continue to be strong, up 20% primarily driven by securities-based lending.”

Bank of America disclosed its securities-based lending in a footnote: SBL balances in Q3 jumped by 25% year-over-year to $49 billion.

Morgan Stanley also disclosed its SBL balances, in the category “Securities-based lending and other,” spread over two divisions, which combined jumped 23% year-over-year to $89 billion.

Charles Schwab didn’t separate out its SBL balances, but lumps them into the category of “Receivables from brokerage clients,” which nearly quadrupled year-over-year to $81 billion.

But Wells Fargo reported that “other consumer loans,” which are primarily SBLs, declined by 18% in Q3 to $27 billion. The decline might be a side effect of the sale of its asset management business to private-equity firms GTCR and Reverence Capital Partners, announced in February this year.

No one tracks the overall outstanding balances of SBL. Each bank knows individually its exposure, you’d hope. Many banks lump them in with other loans, and there is no overall summary figure, and so no one knows how much leverage there is in the stock market in terms of these securities-based loans. But we know it’s huge and ballooning, given the amounts that are disclosed by a few banks.

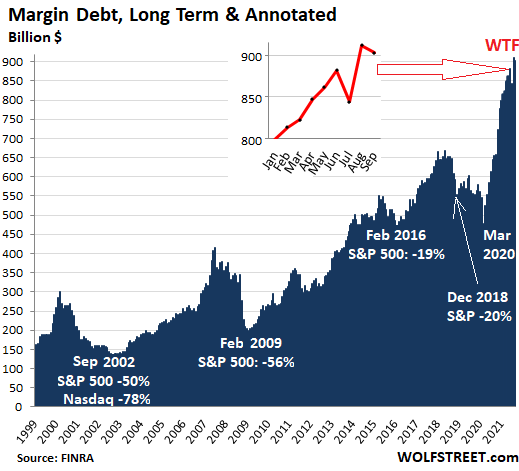

Margin Debt blows out, then dips.

Regular margin loans are reported by brokers to FINRA, which then reports them on a monthly basis, which it did today. They are the only measure of stock market leverage that is tracked. It’s an indicator of the trend in overall stock-market leverage. The tip of the iceberg.

Stock market margin debt, after spiking to another all-time high in August, ticked down in September, to $903 billion, up by 38% year-over-year, and by 61% from January 2020 before the sell-off started.

What’s important in a chart like this that spans over two decades is not the absolute level of leverage compared to back in the day, because the purchasing power of the dollar has diminished. What’s important are the trends and patterns – the steep increases before every stock market sell-off.

Spikes in margin debt don’t trigger sell-offs and they don’t predict sell-offs because they sometimes lag those sell-offs.

But leverage pumps up stock prices by creating buying pressure as borrowed money surges into the market; and when the market tanks, forced selling by leveraged investors creates selling pressure and amplifies the sell-off and triggers its own downward spiral.

The Fed has repressed interest rates to encourage borrowing, and it contributed to this spike in leverage, and to make it all work out, it inflated asset prices via $4.5 trillion in QE in 18 months as part of its official Wealth Effect policy. A few months ago, in its Financial Stability Report, while pointing at Archegos, it warned out of the other side of its mouth about the vast unknown parts of leverage among hedge funds and insurance companies.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter October 16th, 2021

Posted In: Wolf Street