ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 25, 2021 | Pay More, Get Less: Consumer Income & Spending Chewed Up by Red-Hot Inflation

Wolf Richter

You saw this coming after today’s release of the Personal Consumption Expenditure inflation index. “Core PCE” inflation, which excludes food and energy – the lowest lowball inflation index the US offers and which the Fed uses to track its inflation target – spiked by 6.4% annualized for the past three months. In May alone it rose by 0.5% from April.

Consumers got some remaining stimmies and extra unemployment checks and other stimulus funds from the government in May, which still puffed up their income, but less than in prior months. Consumers then spent this income in a heroic manner. But inflation ate a chunk out of their spending in May, and adjusted for inflation, it fell.

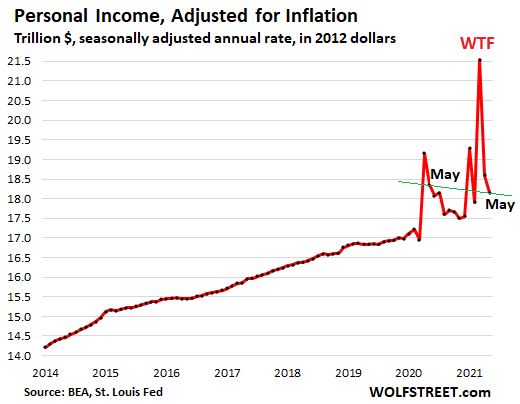

Adjusted for inflation, “real” consumer income from all sources fell 2.4% in May from April, and was down 1.1% from May last year, according to the Bureau of Economic Analysis today. Not adjusted for inflation, consumer income fell 2.0%. Each of the three waves of stimmies triggered a glorious WTF spike in income. Those stimmies are now petering out, but consumers are still receiving other payments from the federal government, including special unemployment benefits:

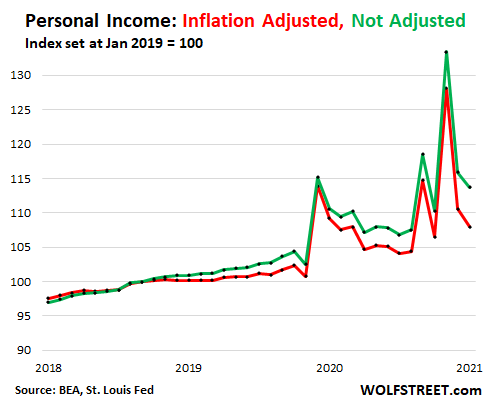

How this bout of inflation, the highest since the early 1980s, is starting to add up month by month, inexorably, and cumulatively, is depicted in the chart below. It tracks personal income from all sources, adjusted for inflation (red line) and not adjusted for inflation (green line), both expressed as an index set at 100 for January 2019. Note the sharply widening gap between the two lines. That’s the effect of inflation. I’m going track it that way going forward:

Inflation ate my homework?

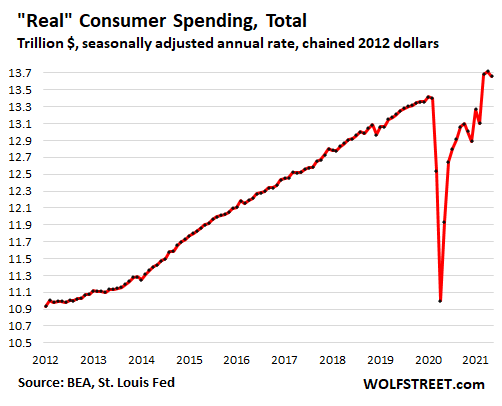

American consumers are still trying to spend heroic amounts of money as fast as they can – they just didn’t keep up with inflation.

Overall “real” spending on goods and services (adjusted for inflation) fell 0.4% in May from April, as “real” spending on goods declined and “real” spending on services barely edged up.

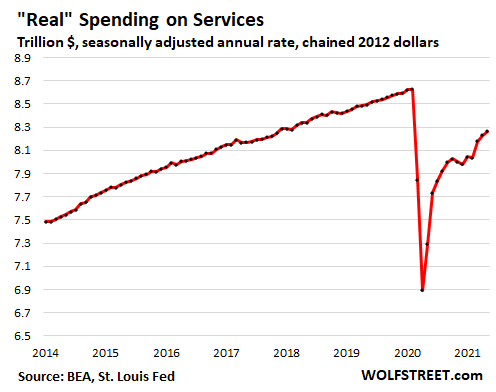

Real spending on services ticked up only a smidgen (0.4%), and was still roughly at the level of November 2018. Everyone expected the big shift from goods to services to commence finally. But not in May. Compared to May 2019, real spending on services was still down nearly 3%.

Services is roughly two-thirds of total consumer spending. It’s the biggie. But discretionary services took a massive hit – such as travel bookings, live entertainment, sports venues, movie theaters, etc. And they’re slow to recover. Movie theaters in particular, like many aspects of brick-and-mortar retail, may never fully recover.

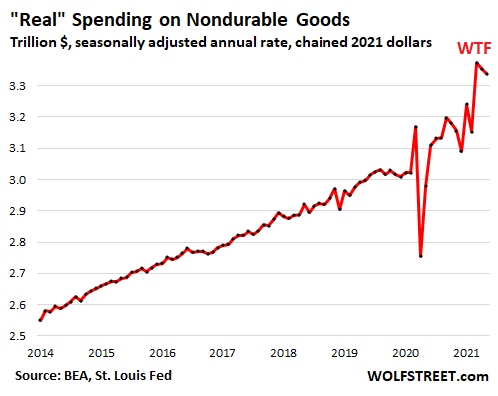

Real spending on nondurable goods fell for the second month in a row, but remained historically high. These goods are dominated by supermarket items, where spending during the Pandemic had spiked in an astounding fashion as consumption shifted from the workplace to the home after people lost their jobs or shifted to work-from-home:

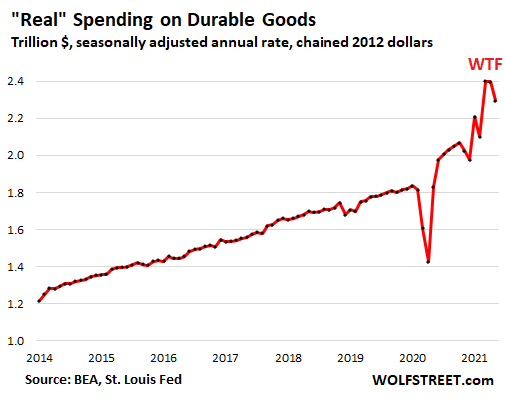

Real spending on durable goods fell 4.3% in May from the stimulus-powered WTF levels in March and April, but remained at red-hot levels as retailers are battling all kinds of supply chain issues, tight inventories, and shortages. This includes motor vehicles, where price increases have been particularly sharp.

Americans, still fortified from the stimulus payments, were out there spending with all their might. But they’re grappling with higher prices, and they are beginning to see significant inflation in the future.

In real life, this takes all forms as consumers are confronted with higher prices, smaller packages, or expensive but minor upgrades from an original item that no longer exists. And they’re willingly paying more as their entire mindset about inflation has changed for the first time in decades.

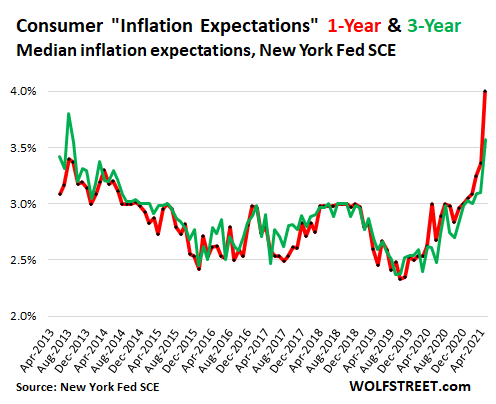

This is also starting to show up in consumer surveys, including in the New York Fed’s Survey of Consumer Expectations. Inflation expectations jumped to 4.0% for the 12-month outlook (red line), and to 3.6% for the three-year outlook (green line). They were a little slow in getting the drift, but they’re catching up:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter June 25th, 2021

Posted In: Wolf Street