ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 12, 2026 | Canadian Insolvencies on The Rise

Danielle Park

Last week, we learned that Canada lost 47,000 full-time jobs in April, while part-time employment edged up by 29,000. April’s loss means Canada has shed jobs in three of the first four months of 2026, for a total of 112,000 jobs lost since January. Nationally, the unemployment rate rose 0.2 percentage points to 6.9%.

Employment fell in Quebec (-43,000), Newfoundland and Labrador (-5,200), Saskatchewan (-4,000), and New Brunswick (-2,700), while Ontario gained 42,000 jobs. As students seek summer jobs, the unemployment rate among youth aged 15–24 rose to 14.3%.

Highly indebted households are starting to crack under the pressure of monthly payments and rising living expenses.

Many current homeowners bought during the 2019-2022 FOMO (fear-of-missing-out) frenzy. Some elders mortgaged their homes to give downpayments to children and grandchildren and co-signed on loans with family members. Some will need to delay retirement or return to work to make ends meet.

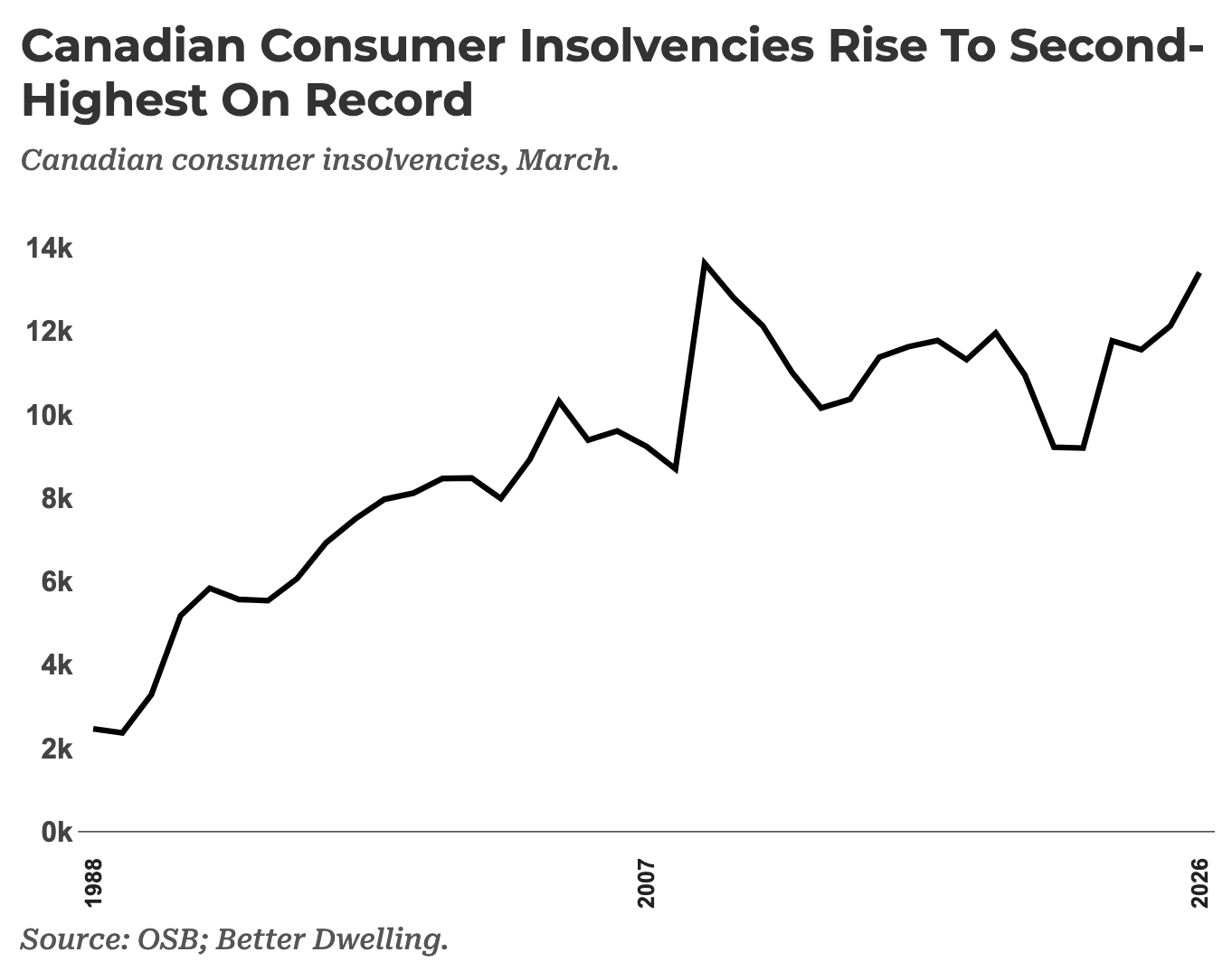

The latest Office of the Superintendent of Bankruptcy (OSB) data shows insolvencies have been consistently grinding higher over the past year. At a 17-year high in March, the volume was second only to the 2009 financial crisis (shown below since 1988).

The OSB received 143,353 insolvency filings in the 12 months ending in March, 4.2% higher than last year. That makes it the second-highest 12-month period ending in March on record, 4.5% behind the 2009 record. Insolvencies are just part of the story. See Canadian Consumer Insolvencies Approach 2009 Record Highs:

Insolvencies don’t capture all debt stress. Many failures stay buried on lender books as missed payments, restructurings, or loans quietly extended. It’s not uncommon to roll all consumer debt into a mortgage takeout or HELOC.

Then there’s the fact that 2009 was the peak of the global financial crisis. Today, we’re approaching that level while the economy is supposedly fine. We also have the benefit of knowing 2009 was the peak in hindsight. Today’s data doesn’t tell us whether this is the top or just another step to the top.

As of the first quarter of 2026, non-performing mortgage loans in Canada reached approximately $7.2 billion — an increase of about 150% since 2022. These are “Stage 3” loans, meaning they are more than 90 days overdue and considered in default. (source: JDL Realty).

Borrowers who secured mortgages in 2020–21 at rates under 2% are now seeing renewal offers in the 4–5% range. Equifax Canada has noted that non-mortgage delinquencies have reached levels not seen since 2009 — families juggling late car payments or credit card bills are in a weaker position when their mortgage comes up for renewal (source: Nesto).

Results from Bank of Canada stress testing suggest that the share of mortgages in arrears by at least 90 days could rise to a level comparable to, or higher than, levels reached during the 2008–09 global financial crisis under a prolonged trade war scenario (Bank of Canada).

The Greater Toronto and Vancouver Areas are the most at risk, along with regions with high exposure to tariffs, where job losses are most evident (CMHC). The major stress test for the Canadian mortgage market is 2026-27 as the pandemic-era renewal wave crests.

The Office of the Superintendent of Canadian Financial Institutions (OFSI) predicts that rising residential mortgage arrears and defaults are the number one threat to Canada’s financial system (OFSI 2026-27 annual risk outlook report, April 2026).

Not priced in — to the end of Q1, Canada’s Big Six banks had reported near-zero write-offs against their multitrillion-dollar loan book — and Canadian equity investors are heavily exposed to disappointment. Since the end of March, Canada’s finance sector shares have bouncd 13.6% and +7.7% year-to-date, and comprise a whopping 32.5% of the TSX index and all of the portfolios that track it.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Danielle Park May 12th, 2026

Posted In: Juggling Dynamite

Next: US Real Estate Remains Stale »

Is the tide going out?