ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

April 18, 2026 | Trading Desk Notes for April 18, 2026

Victor Adair

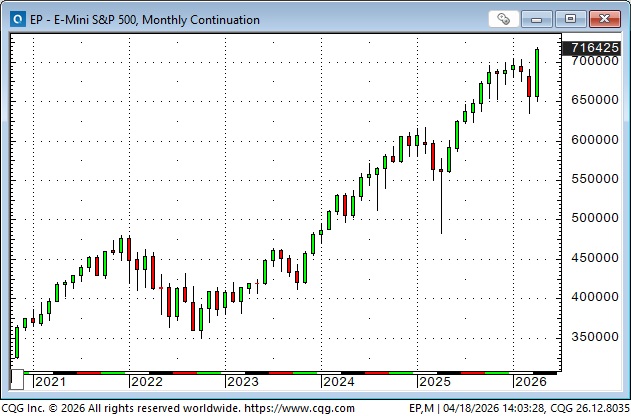

The leading stock indices surged to new record highs this week

S&P futures closed green for 14 of the past 15 trading days, rising ~13% to new all-time highs. Half of those gains came this week. The market gapped down 100 points on Sunday afternoon following “no agreement” at the Islamabad peace talks, but then soared for the rest of the week as “good news” kept coming every day, with Trump proclaiming on Friday that the Hormuz will be open forever! That sounded a bit like a bell ringing.

The three-week surge from Trump’s “End of Civilization in Iran” lows at the end of March, to his “Hormuz will be open forever” highs on Friday, appears to be the S&P’s biggest-ever three-week point gain.

The S&P has more than doubled from the October 2022 lows.

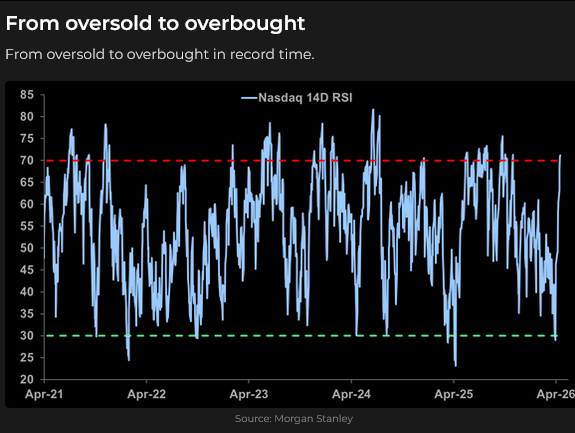

The NAZ has outperformed the S&P, up 17% in the last three weeks.

And up 156% from the October 2022 lows.

Across all markets, but especially in the equity markets, the moves over the last three weeks have been accelerated by the unwinding of positions. What began as short-covering in equities, as prices started to rise on Friday, March 31, before the announcement of a ceasefire, became a squeeze higher as shorts HAD to get out. Then that turned into a FOMO “get me in at any price” runaway rally. IT’S LIKE THE WAR NEVER HAPPENED! (If you don’t count the death and destruction.)

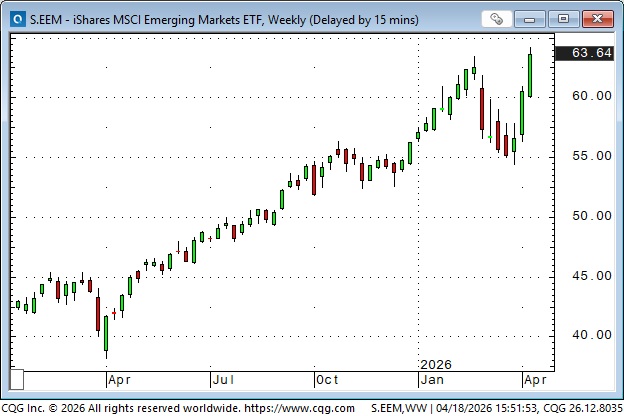

All of the leading global stock indices are above their pre-Iran war levels, with the S&P, Nasdaq, Russell, Nikkei, and emerging-market ETFs at new all-time highs.

Semis have replaced energy as the hottest market sector.

Spoiler alert: On Saturday morning, Iran claimed they have “Strict control” of the Strait, and it will not be fully open. This news may lead to the equity indices opening lower on Sunday afternoon, subject to a fresh headline countering the Iranian claim.

I’ve often wondered, especially since the death of the Ayatollah, who (if anyone) is “in charge” in Iran? Is there a chain of command, or are there conflicting forces? Could “moderates” make a “deal” with the US that “hardliners” would ignore? And then there’s the concern that the US and Israel may have different goals and objectives (especially relative to Hezbollah).

It seems as though the equity market rally has “priced in” an overabundance of “good news.” But that’s what stocks do, right? As Howard Marks says, “In the real world, things fluctuate between pretty good and not so bad, but in investor minds, they go from flawless to hopeless (and then back to flawless!)

Currencies

The DXY US Dollar Index rallied in March as the Iran war escalated, and then trended lower in April as traders began to anticipate an end to the war. In other words, the USDX moved inversely to the equity markets, but with much less velocity. The USDX traded on Friday at the same levels as before the war began.

The Chinese RMB (with a soft peg to the USD) has been rising against the Japanese Yen (gold line) and the Korean Won (blue line) since 2020, and is now at multi-year highs (as the USD is now near multi-year highs against the Yen and the Won).

Interest rates

Bond prices fell sharply during the first three weeks of the war, as oil prices surged higher (implying likely higher inflation ahead), then went sideways for a few days before drifting higher over the past two weeks (as oil prices fell from their highs).

The Japanese 10-year bond yield traded at a 29-year high this week, just below 2.5%.

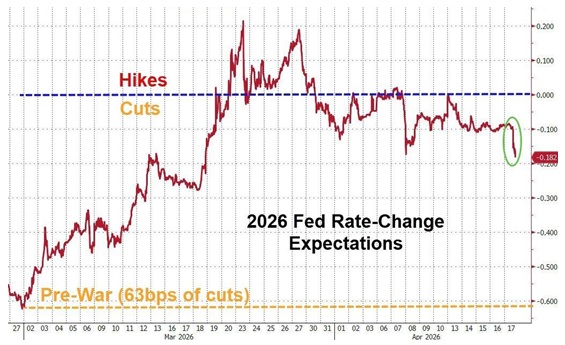

Short rates: before the war, the forward short rates market was pricing in ~60 bps of cuts from the Fed in 2026. That changed by late March, when oil prices were making their recent highs, to expecting ~20 bps of hikes. At the end of this week, markets were back to pricing about 20 bps of cuts this year.

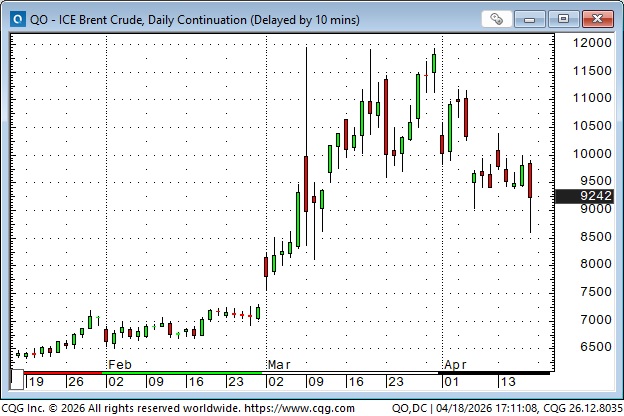

Crude oil

Front-month Brent futures rallied throughout March and have trended lower in April.

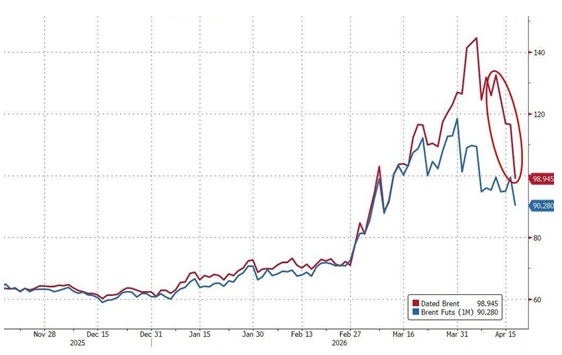

Dated Brent (that’s physical oil for delivery in the North Sea at a specific date) briefly traded above $140 in early March but dropped below $100 this week.

Key energy share prices rose in March and fell in April.

The FT Weekend Essay this week was titled “The coming global food crisis” and focused on the disruption of the flow of fertilizer chemicals through the Hormuz Strait. I didn’t know whether to treat the essay as another “Economist Magazine Cover” or to take it seriously. (For instance, for a story on a global food crisis, it didn’t say a word about the developing drought in key North American agricultural areas). I guess after all the “fake news” over the past six weeks, and all the market comments from instant-experts, I tend to believe in nothing, at least with respect to my short-term trading. (Thank you, JMP!)

On my radar

The American quarterly earnings report season has started, and the banks seem to be doing fine. The “energy price shock” has diminished, the private credit concerns don’t seem to be metastasizing, and the worries about AI have subsided (AI stocks are flying), so as Howard Marks might say, things look pretty good, or at least a lot better than they looked three weeks ago.

A $2 Trillion SpaceX IPO is apparently on the horizon. Bears think it could signal a market peak.

Trump plans to go to China to meet Xi about a month from now.

My short-term trading

I started this week short the Yen. I covered for a decent gain on Monday when the Yen didn’t fall on news that the “peace talks” had failed. Perhaps traders were shy to press the Yen lower on the news because of intervention worries, but when it didn’t fall on bearish news, I covered.

I bought the Yen later on Monday and was nicely ahead when it rallied along with most other currencies on Tuesday, but the gains were not sustained, so I covered for a tiny profit on Thursday (and missed Friday’s rally).

I shorted the S&P on Thursday and was quickly stopped for a slight loss. I reshorted the market about 100 points higher on Friday (near the day’s high) and stayed short into the weekend.

I had planned to write a longer Thoughts on Trading section today, but I wasted three frustrating hours with connectivity issues, and (as regular readers may have noticed) this week’s Notes have been briefer than usual.

Best wishes to all my readers for trading success.

Barney

Listen to Mike Campbell and me discuss markets

You can listen here to Mike and me discuss the wild rally in equity markets this week, as traders tried to front-run bullish news about the war.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair April 18th, 2026

Posted In: Victor Adair Blog