ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 16, 2026 | Trading Desk Notes for May 16, 2026

Victor Adair

The S&P has its biggest down day on Friday since late March

After rallying nearly 19% from the March lows to record highs on Thursday, the S&P slumped on Friday as bond yields soared, front-month Brent crude oil rose to ~$110, and Hormuz remained a Gordian knot.

The S&P has closed higher for seven consecutive weeks, but this week’s rally above 7500 was “trumped” by a sharp reversal on Friday.

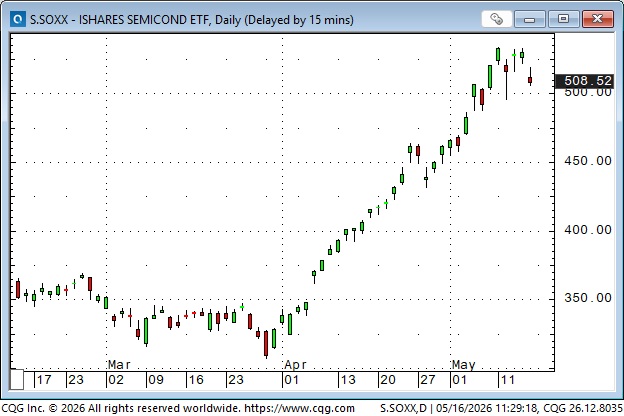

Semiconductors have been the strongest market sector since the March lows, up nearly 75% in the last seven weeks.

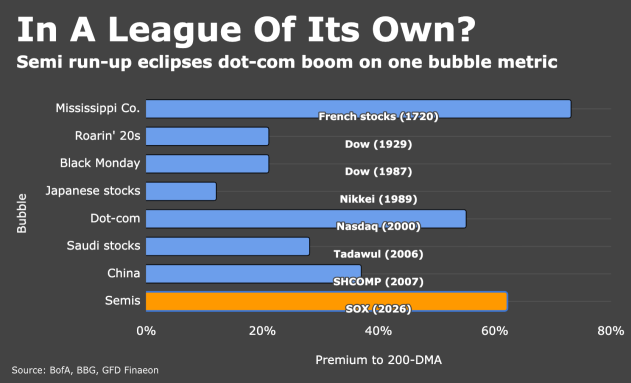

BoA research sees the run-up in the SOXX as the greatest bubble since 1720.

The “MAG 7” did $230 Billion of share buybacks in 2025.

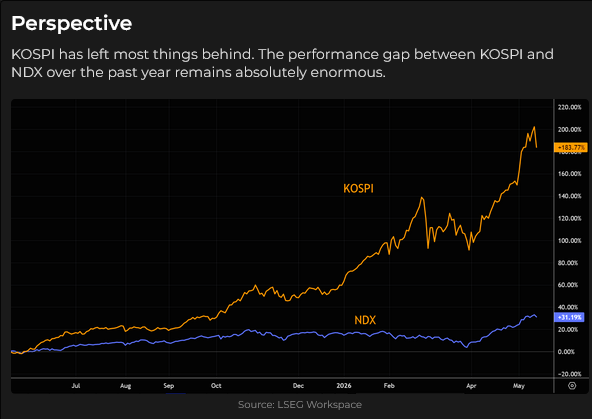

A “subset” of the semiconductor rally (and also a bellwether for the global manic FOMO chase) has been the Korean market (the KOSPI), where two companies, Samsung and SK Hynix, have driven it to a ~70% gain since late March. This week’s market correction hit the Korean market harder.

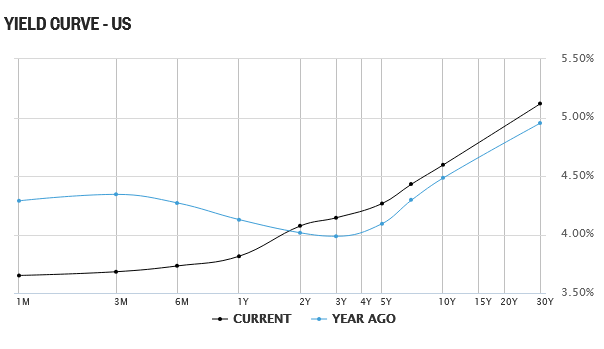

Global bond prices fell sharply this week

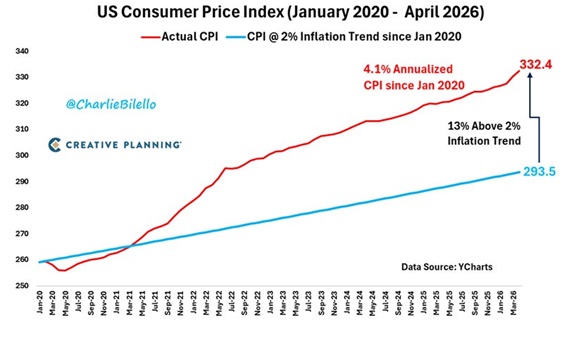

US ultra-long bond futures reversed lower at the beginning of the Iran War (blue ellipse). They took another leg lower this week as higher energy prices fed through to higher inflation reports (in the USA CPI at 3.8% yoy, PPI at 6% yoy) and as political/fiscal concerns rose in both the UK and Japan. (Global bond yields are “broadly” interconnected). The yield on the US 30-year is 5.12%. The 10-year is 4.6%.

Quote of the Week from Richard Privorotsky, Goldman Sachs

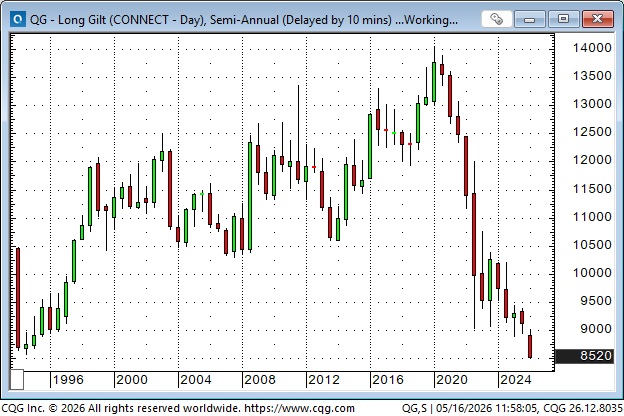

The long UK Gilts tumbled to the lowest levels since 1992, with yields on the 30-year now at 5.85%.

The yield on the Japanese 30-year bond, which was first issued in 1999, rose to a record high of 4% this week. This chart is from Marketwatch.

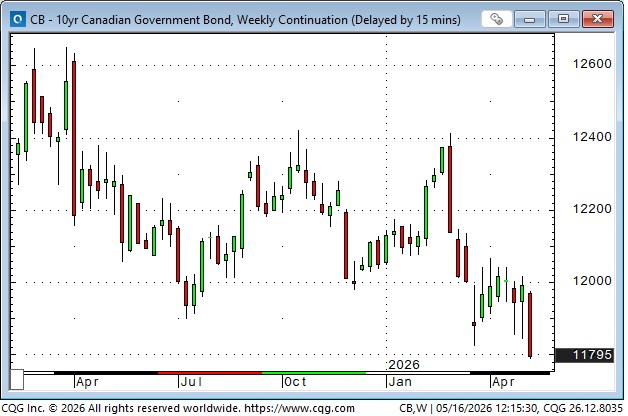

Futures on the Canadian 10-year bond exhibit a price pattern similar to those of American and British bonds. The yield on the Canadian 10-year is 3.7%. The 30-year is 4.02%.

In February, short-rate futures (Secured Overnight Funding Rates) in the US were pricing ~50 bps of cuts from the Fed before the end of 2026, but are now pricing ~25 bps increase.

Energy

July Brent futures closed this week at ~$109.50, up from last week’s low of ~$96. On his way home from China, Trump apparently told reporters that he “did not feel compelled to reopen the Hormuz Strait.”

Forward Brent futures are pricing the Hormuz Strait remaining closed longer than previously thought. This chart of December 2026 Brent closed at a record high this week. In March, when front-month Brent crude futures rallied to $120, December closed ~$75, a $45 discount to the front month, as the market priced a “short duration” war. That thinking has changed.

Futures contracts for Nymex wholesale gasoline closed at new weekly highs this week, up ~87% from January lows.

Nymex natural gas is slowly lifting from April’s lows, a break above $3.18 basis July could have some follow-through.

The oil refining business is going gangbusters, up ~100% YOY.

Kevin Warsh has his first day “on the job” as Fed Chair on Monday

Kevin has an impressive resume and previously served as a Governor at the Fed from 2006 to 2011, during Ben Bernanke’s tenure as Fed Chairman. Historically, the market has “tested” a new Fed Chair soon after he takes office.

Metals

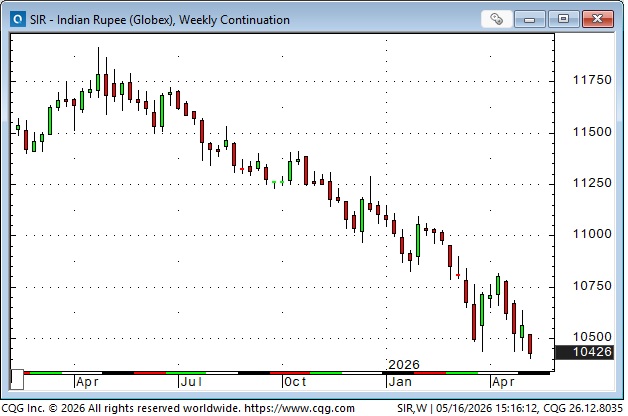

India increased the import duty on gold to 15% this week as the country struggles with a falling Rupee and a widening trade deficit amid soaring energy import costs. India is the world’s biggest gold market, after China, and the government is clearly trying to discourage citizens from buying gold.

My view is that gold prices rose after the Hamas attack on Israel in October 2023, driven by central bank and “debasement trade” buying, and were then “goosed” by retail FOMO buying in the 2nd half of 2025 and into the blow-off top in early 2026.

The conditions which drove CB and “debasement” gold buying remain intact (and may now be greater than ever), but the market is in the process of “clearing” speculative excesses, and that may take some time.

My view on silver is much the same as my view on gold, except that the speculative FOMO buying in silver was much more excessive than in gold, just like it was in 1979/80. Silver dropped from a 2-month high of ~$90 on Wednesday to ~$76 on Friday (as gold fell ~$200) amid selling across assets.

Comex copper futures soared to a record high this week near $6.65, more than double the 2022 lows, but could not sustain the advance, giving up the Monday-to-Thursday gains on Friday, a pattern similar to price gains and losses across several equity markets.

Currencies

The DXY US Dollar Index rallied from Tuesday to Friday as the USD rose against nearly all currencies (when markets turn risk-off, the USD tends to rise).

The British Pound was particularly weak amid speculation that PM Starmer may have to step down following severe Labour losses in recent elections. The weak GBP/Gilts market looks like a reprise of the Liz Truss fiasco.

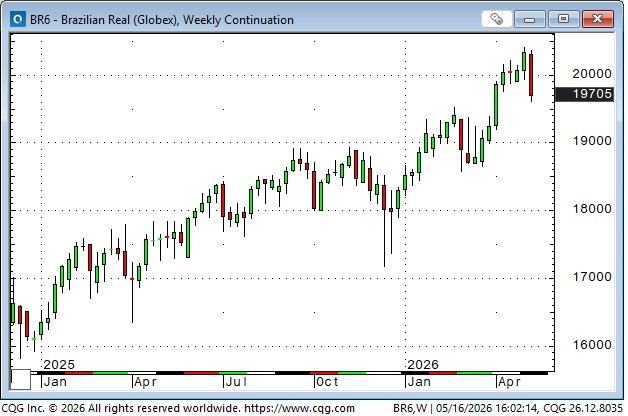

The Brazilian Real, which has soared ~25% against the USD since January 2025, fell sharply this week amid a political scandal that may undermine Flavio Bolsonaro’s chances of winning an election against Lula da Silva.

The Australian Dollar, which has rallied ~16% against the USD over the last 12 months and is also up relative to most other currencies, especially the Yen, had a sharp reversal this week. Speculators are heavily long the Aussie.

Cuba

Cuba may soon have some “affiliation” with the USA, like Venezuela, as the “Donroe Doctrine” rolls on. Estimates for undiscovered, technically recoverable offshore oil in Cuba’s North Cuba Basin range from 4.6 billion barrels (according to the U.S. Geological Survey) up to an estimated 20 billion barrels claimed by the Cuban government.

My short-term trading

I shorted the S&P on Tuesday, and the market dropped ~50 points in my favour before turning around and stopping me out for another slight loss.

I reshorted the market early in the Thursday overnight session and stayed with the trade into the weekend, with a ~90-point unrealized gain as the market tumbled and closed at its lows.

I’ve been anticipating a significant turn in the S&P for a couple of weeks, and I’ve lost a little money trying to position for the turn. If it looks like the turn is underway, I’ll try to add to my position.

I bought some OTM Yen calls on Tuesday in anticipation of a “Hawkish” comment from the BoJ, but the firming oil price and the USD rising across the FX spectrum pushed the Yen lower. I’ll abandon the position early next week if it doesn’t turn higher.

On my radar

NVDA, which nearly reached a $6 trillion market cap this week, reports on Wednesday after the close.

Mid-term elections are less than 6 months away, and Trump’s popularity is low. Will he reduce American exports of crude and products to keep domestic prices down?

Wall Street is anticipating massive IPOs from SpaceX, OpenAI and Anthropic, which may total $4 trillion. Yes, American stock market exceptionalism is back, but that much paper could swamp the market.

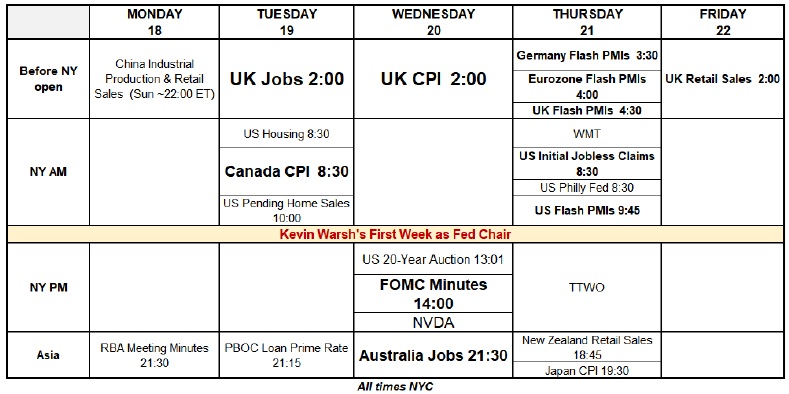

Here’s a calendar from Brent Donnelly for the week ahead.

Thoughts on trading

Here’s my side of a conversation I had with a Substack friend:

A few years ago, when gold broke its historical negative correlation with a higher USD and higher interest rates, it was a signal that “something new” was influencing the gold market. The “something new” turned out to be (previously opaque) aggressive central bank buying.

If the S&P’s historical negative correlation with geopolitical risks is breaking down (ie, the market “doesn’t care” about the Iran war), perhaps “something new” is influencing the S&P. Perhaps it is simply aggressive buying of anything/everything related to AI.

I used to view the S&P as the #1 global risk barometer; if it was soaring, it implied “no worries” and therefore FX carry trades and other “risk on” trades kept working. However, if aggressive AI buying has destroyed the functionality of the S&P as the #1 global risk barometer, then FX carry trades, and other “risk on” trades, including the S&P itself, may be exposed to a Willie E. Coyote moment.

The Barney report

Barney will chase after a thrown ball (and, most of the time, bring it back to me) until he just can’t run anymore and has to lie down for a rest. If we had audio on this blog, you’d hear him panting, but he’s just resting and will be ready to chase again in a minute or two.

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed how the soaring stock markets may be entering a “rough patch” amid surging bond yields. You can listen to the entire show here. My spot with Mike starts around the 1:02 mark. Be sure to listen to my friend Josef Schachter, a veteran oil analyst, share his thoughts on the oil market starting around the 6.47-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair May 16th, 2026

Posted In: Victor Adair Blog

Next: Shootout at the Inflation Corral »