ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 28, 2026 | Trading Desk Notes for February 28, 2026

Victor Adair

Here’s how markets were pricing tensions ahead of the attack on Iran

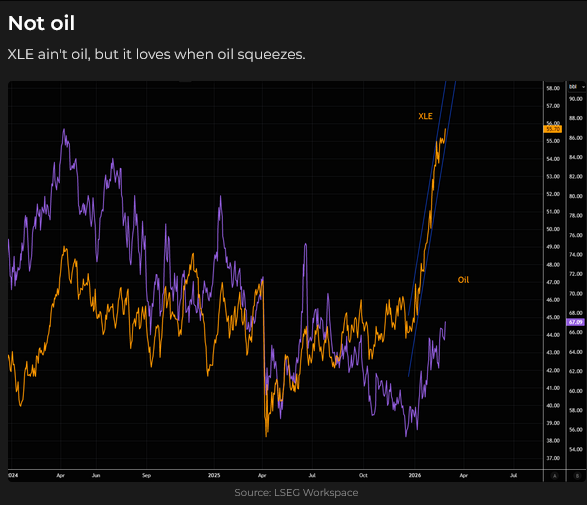

Nymex front-month WTI futures closed at a 7-month high of ~$67 on Friday, up ~23% from December’s $55 low. (WTI had trended lower from ~$95 in September 2023 to the December 2025 low, as supply appeared to grow faster than demand).

COT data shows that net speculative long positioning declined from ~270,000 contracts in July 2025 to ~70,000 in December 2025, the smallest net bullish positioning in over five years. Since the beginning of 2026, net speculative long positioning has ramped up from ~65,000 to ~217,000, as speculators bought a lot of oil amid rising tensions.

The XLE Energy Sector ETF drifted sideways from 2023 through the end of 2025, as WTI prices fell by over 40%, but then jumped ~22% YTD.

I wonder if the XLE’s outperformance relative to the declining price of WTI over the past couple of years was due to the massive flow of passive capital into US equities, with the energy sector getting its “share” of that new capital regardless of the oil price, or if the outperformance reflects technological improvements in the energy sector that allow for sustained profits even as crude oil prices fell.

Comex front-month gold futures closed Friday at an all-time weekly high of ~$5,300, up ~$1,000 YTD.

The GDX gold miners’ ETF nearly tripled in 2025 and surged to an all-time high close this week.

The DXY US Dollar Index fell to a 4-year low in late January (as precious metals and copper surged to record highs). It recovered modestly since then, but there was not a strong “buy the USD for safety” bid in the currency markets even as US/Iran tensions increased.

The Swiss Franc closed at an all-time high against the Euro on Friday, up ~3% from the January lows.

The Swiss Franc has been trading at an all-time high against the USD for the past five weeks (X a brief spike in 2011), up ~20% over the last 12 months.

Treasury bond futures have rallied over the past three weeks and closed this week at their best levels in 12 months. Bond prices rose as a haven from choppy price action in equities, concerns about private credit and worries about a potential conflict between the US and Iran.

The S&P 500 Index drifted sideways near all-time highs over the past three months, despite dramatic rotation across subsectors (and despite much stronger stock index performance in many countries outside the US). Equity index traders didn’t seem to be taking “defensive” action ahead of a possible conflict between the US and Iran. Forward EPS for the S&P for 2026 are estimated at ~$315, or ~22X.

Range of outcomes

Price action across markets when they reopen will depend upon the anticipated range of conflict outcomes and positioning. For instance, if there are immediate signals that Iran will offer to meet American demands in exchange for a ceasefire, I’d expect WTI prices to fall sharply, given the recent dramatic increase in speculative net long positioning. I’d also expect some weakness in precious metals, the Swiss Franc, and bonds, while stocks would rally (all else being equal!).

If the conflict appears to be intensifying or widening to include other countries, or will grind on for some time as both sides “dig in,” then I’d expect to see WTI, precious metals, the Swiss Franc, and bonds rally and stocks weaken.

Stocks

In addition to trying to “price in” the US/Iran conflict, equity markets are concerned with the changing AI narrative, private equity/credit issues and the flow of funds to foreign markets.

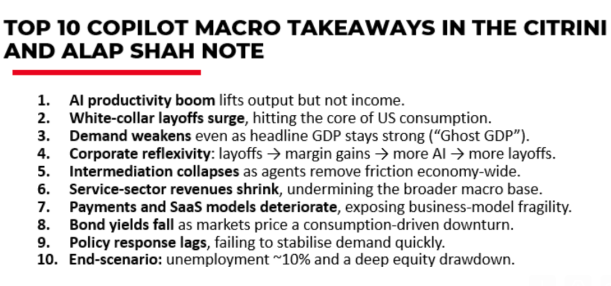

The AI narrative includes concerns about the ROI on massive capex, who will win and who will lose, and how it will impact employment and the economy. On Monday, a dystopian research piece from Citrini research caused a sharp drop in the S&P and NAZ. Here’s a 10-point summary of the Citrini piece:

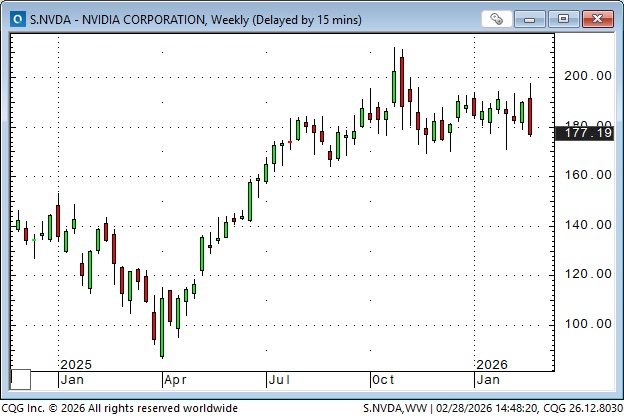

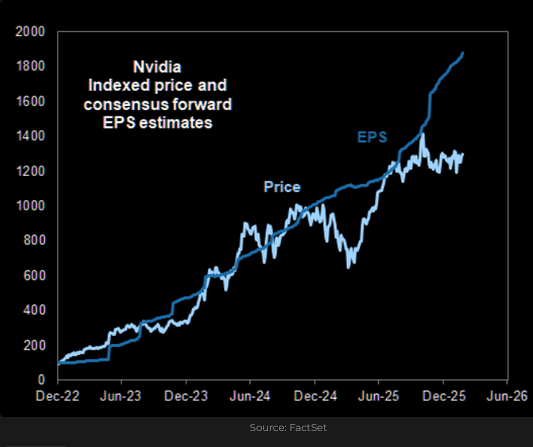

On Wednesday, the NVDA quarterly report beat expectations on virtually every front, and the share price rose above $200 in after-market trading. However, there was no follow-through, and NVDA suffered its lowest weekly close in nearly three months.

Private equity/credit worries have been a “fringe” concern for a long time, if only because there is no “mark-to-market” valuation of their assets and liabilities. Lately, markets have become increasingly concerned about some of the big PE names and the banks that finance them.

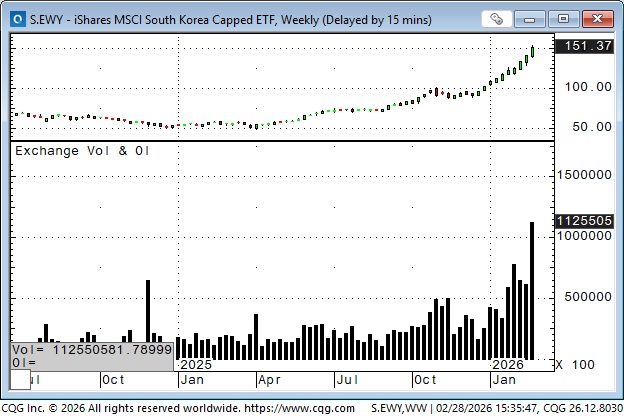

Foreign markets: while the S&P has been drifting sideways near record highs over the past three months, equity indices in many other countries have outperformed the American benchmarks. Asian markets, and especially Korea, have soared. The Japanese Nikkei is up ~100% from the April 2025 lows.

The Korean index has risen for ten consecutive weeks and is up over 200% from the April 2025 lows.

The recent parabolic rise in the Korean Index saw a massive increase in trading volume as Korean retail traders (referred to as “ants”) went full FOMO.

The Euro Stoxx 50 is a “European” version of the DJIA, up ~41% from April 2025 lows.

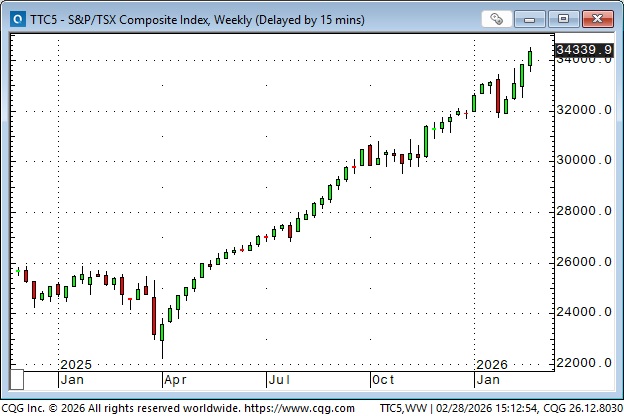

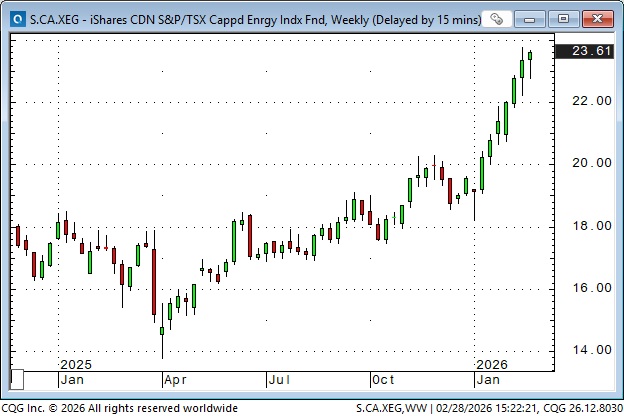

The Toronto Composite is up ~55% from the April 2025 lows, compared to a 44% gain for the S&P. The TSE outperformance is due to strong gains in the mining sector and, lately, the energy sector. I suspect that Canadian pension funds may have repatriated some capital from the US markets (“rebalancing” after a decade of outperformance by US equity and the US Dollar), helping to boost the TSE.

The Canadian energy sector.

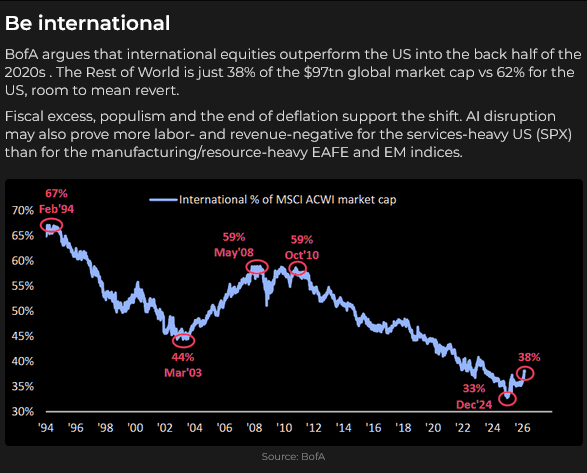

The American equity markets have outperformed the Rest Of The World for years, especially since the GFC, but BoA argues that will change over the next few years.

New capital continues to flow into equity markets, but BoA reports that only 20% of that flow is going into US markets, while 80% is going into markets outside the USA.

Currencies

Regular readers know that I’ve been intrigued by the long-term weakness of the Japanese Yen (down about 50% against both the USD and the Euro from record highs reached in 2012). For months, I’ve thought that if the Yen started to rise, it could be a multi-year move.

One of the reasons for the sustained weakness of the Yen is that all Asian currencies are undervalued as part of their mercantilist policies to facilitate exports. The Japanese authorities have demonstrated, through intervention, that they don’t want to see it weaken further (and Trump thinks it is too weak), but what would cause it to rise?

My best guess would be sustained capital repatriation. The Economist magazine (January 29, 2026) estimates that Japanese institutions hold ~$6 trillion in foreign securities, with about half of that in the US and another 20% in the Cayman Islands (a conduit for further US investments).

Why would those institutions repatriate capital? Well, the money was invested overseas because interest rates in Japan were very low (they’re starting to rise), the Yen was on a one-way road to lower levels, and domestic investment opportunities were not attractive. That may have changed now that Takaichi has a supermajority; she may be able to reinvigorate the economy, and if she does, that could trigger capital repatriation.

If capital repatriation began, it might start an unwinding of the Yen carry trade, which would give the Yen an additional boost.

I’ll be watching for opportunities to buy the Yen.

Thoughts on trading

When I say I’ll be watching for opportunities to buy the Yen, I don’t mean I’ll buy it because I think it may (or should) rise. If I think there is a possibility/probability it will rise, then I look for good risk/reward setups to buy it. If I don’t find those setups, I don’t buy it even if I remain bullish. Risk management trumps my desire to be right on my “call” that the Yen may rally.

My short-term trading

I shorted the S&P on Sunday afternoon when it opened below Friday’s strong close. I covered for a modest profit on Monday.

I bought the Yen on Sunday afternoon but was stopped for a modest loss on Tuesday.

I bought the S&P on Tuesday and held that into the NVDA quarterly report on Wednesday afternoon. I covered the trade for a decent win in the overnight market when there was no rally on the NVDA news.

I bought the CAD on Friday by mistake (I hadn’t cancelled a stop buy order placed last week when I was short CAD). I kept the trade into the weekend.

The Barney report

Barney built a fort in my bed. Are all dogs this clever?

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show (recorded yesterday before the attack on Iran), Mike and I discussed how the markets were pricing the risks of an attack on Iran. You can listen to the show here. My spot with Mike starts around the 52-minute mark.

Listen to Jim Goddard and I discuss markets

I recorded my monthly 30-minute interview with Jim Goddard yesterday before the attack on Iran. We discussed how markets were reacting to the risk of an attack on Iran, the big swings across different market sectors, NVDA, Private Credit, the rise in WTI, gold, and some highlights of my annual speech at the World Outlook Conference in Vancouver. You can listen to the interview here. My spot begins around the 10-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past five years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair February 28th, 2026

Posted In: Victor Adair Blog

Next: US & Israel vs Iran »