ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

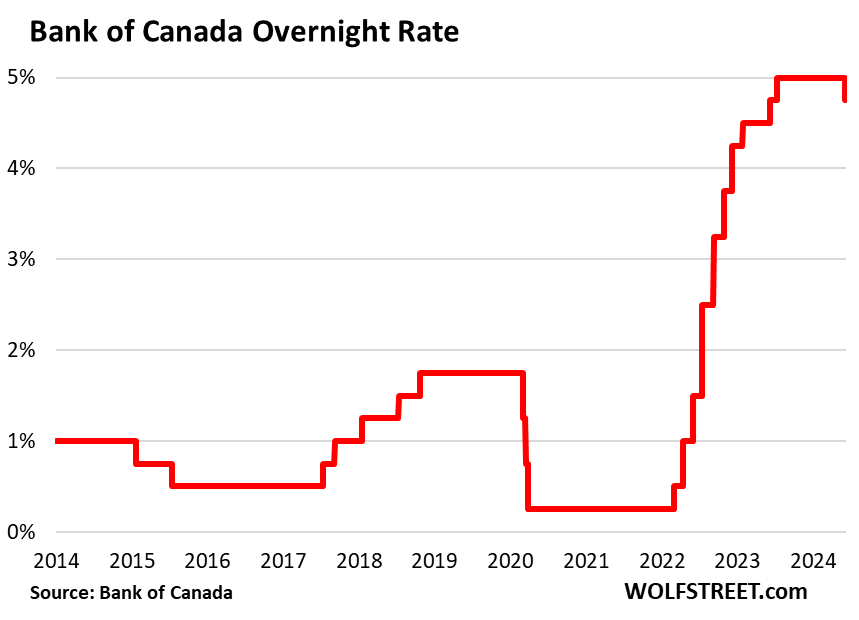

June 6, 2024 | Bank of Canada Cuts by 25 basis points, to 4.75% as Economy and Inflation Slowed. QT Continues

Wolf Richter

“With continued evidence that underlying inflation is easing,” the Bank of Canada said today that “monetary policy no longer needs to be as restrictive,” and it cut policy interest rates by 25 basis points, as widely expected.

But QT will continue, the statement said. The BOC has already shed 64% of the securities it had added during the pandemic.

It cut the target for its overnight rate to 4.75%; the Bank Rate to 5.0%, and the deposit rate to 4.75%.

“Recent data has increased our confidence that inflation will continue to move towards the 2% target,” it said in the statement today.

Employment “has been growing at a slower pace than the working-age population,” the statement said in a reference to the huge wave of immigrants that has flooded the labor market. “Wage pressures remain but look to be moderating gradually,” it said.

Due to the huge wave of immigrants, per-capita GDP declined in six quarters over the past seven quarters (the exception was a tiny uptick in Q1 2023), as economic growth stalled in the second half last year, and was too slow in the remaining quarters to keep up with population growth.

“However, shelter price inflation remains high,” the statement said. So there’s that. If it weren’t for rents. Rents spiked because that huge wave of immigrants needs rental housing, and no one was prepared for it.

“Risks to the inflation outlook remain,” the BOC said. It’s “closely watching the evolution of core inflation and remains particularly focused on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behavior.”

Two IFs for more cuts: “If inflation continues to ease (#1 IF), and our confidence that inflation is headed sustainably to the 2% target continues to increase (#2 IF), it is reasonable to expect further cuts to our policy interest rate,” BOC governor Tiff Macklem said at the press conference.

He outlined four risks to the lower-inflation outlook:

- “If global tensions escalate”

- “If house prices in Canada rise faster than expected” (house prices are down 14% from the peak in February 2022, but not all markets are the same: from Toronto heading south fast, to Calgary surging to new highs)

- “If wage growth remains high relative to productivity.”

“We don’t want monetary policy to be more restrictive than it needs to be to get inflation back to target. But if we lower our policy interest rate too quickly, we could jeopardize the progress we’ve made. Further progress in bringing down inflation is likely to be uneven and risks remain,” he said.

“We’ve come a long way in the fight against inflation. And our confidence that inflation will continue to move closer to the 2% target has increased over recent months,” he said.

He said that “indicators of underlying inflation increasingly point to a sustained easing” of inflation. He cited these four metrics:

- “CPI inflation has eased from 3.4% in December to 2.7% in April

- “Our preferred measures of core inflation have come down from about 3.5% last December to about 2.75% in April

- “The 3-month rates of core inflation slowed from about 3.5% in December to under 2% in March and April

- “The proportion of CPI components increasing faster than 3% is now close to its historical average, suggesting price increases are no longer unusually broad-based.”

“This all means restrictive monetary policy is working to relieve price pressures,” Macklem added. “And with further and more sustained evidence underlying inflation is easing, monetary policy no longer needs to be as restrictive. In other words, it is appropriate to lower our policy interest rate.”

Why higher rates may be more effective in Canada than in the US.

There has been a lot of discussion about why the rate hikes seem to have been more effective in Canada than in the US in slowing the economy and bringing down inflation.

Part of the reason may be how mortgages are structured in Canada. The dominant mortgage rates in Canada are either variable-rate mortgages whose rates adjust for existing borrowers as rates go up, or fixed-rate mortgages whose rates are fixed for shorter terms such as two years or five years, and borrowers are facing renewals at much higher rates. So it’s existing borrowers that face higher mortgage payments on homes that they’d living in for years, which puts a damper on spending for other stuff, thus slowing demand growth.

In the US, with the typical 30-year fixed rate mortgage, only new borrowers face higher mortgage rates, and existing borrowers with their 3% mortgages are laughing all the way to the bank.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter June 6th, 2024

Posted In: Wolf Street