ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 27, 2026 | Trading Desk Notes for June 27, 2026

Victor Adair

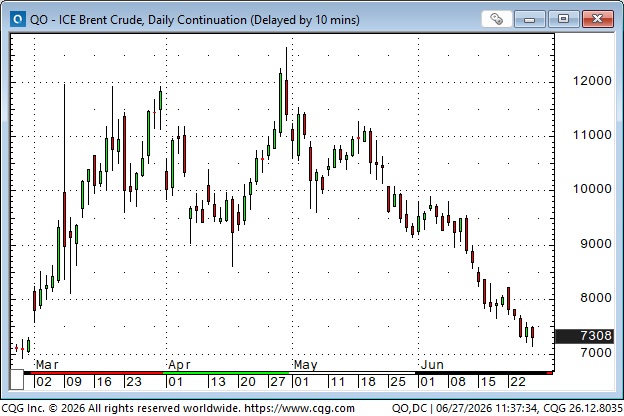

Brent crude oil futures return to pre-war levels

Front-month Brent futures traded between ~$71-~$73 on February 27 and closed this week at ~$73. Front-month WTI futures closed this week at ~$70, slightly above their February 27 range of ~$65 to ~$68. A “tit-for-tat” military exchange between the US and Iran on Friday/Saturday may impact oil prices this coming week.

Nymex July gasoline futures rallied by ~60% from February 27 to the May 18 highs, but have given back only ~50% of those gains at this week’s close. American refineries are working “flat-out,” but exports of refined products are at record highs.

Energy quote of the week:

“An important change following the Iran war: Energy security is now top of mind with many governments, not being green.” James Thorne, Chief Market Strategist, Wellington-altus.ca.

Interest rates

Bond futures prices (inverted in this chart) have generally tracked oil and gasoline futures since late February. (Bond yields rose as oil prices rose, and fell as oil prices fell).

The December 2026 SOFR 3-month futures have gone from pricing a ~3% rate on March 2 (blue ellipse) to pricing a ~4% rate on this week’s close (pink ellipse).

The market may be pricing short rates to be ~50 bps higher in December than they are now because 1) Warsh sounded more hawkish than expected at last week’s FOMC meeting, 2) lower energy costs may further stimulate strong economic growth, and 3) the AI “build out” is stimulating multiple areas of the economy, not just “computers” (the AI “build out” accounted for ~75% of US Q1 GDP growth). This coming week’s employment data will be important for short-term interest rate expectations.

Caterpillar doesn’t make chips or computers, but it does make power plants that generate electricity for data centers.

Thursday’s PCE data was about as expected, with YoY core at 3.4%, headline at 4.1%. Other metrics show inflation at much lower levels. 2-year real yields have risen from ~0.5% in mid-April to ~2% now.

Currencies – the US Dollar is rising

The DXY US Dollar Index has risen ~4% from January’s 4-year lows to this week’s 14-month highs. Favourable interest rate differentials and “American exceptionalism” help lift the USD. COT data shows very bullish net speculative positioning as of June 23. Volkswagen’s announcement this week of a planned layoff of 100,000 workers in Germany due to rapidly rising sales of imported Chinese cars in Europe was another disappointment for the Euro.

The Canadian Dollar traded to a 14-month low (~7040) this week amid widening interest rate spreads, as the USD rallied against virtually all FX. Falling oil prices didn’t help the CAD.

Metals

Gold traded below $4,000 this week, marking an 8-month low and down ~28% from the January highs. The net liquidation of speculative FOMO buying from July 2025 to March 2026 has weighed on gold prices, but the market feels oversold here.

The GDX closed this week ~35% below the record highs reached in early March.

Silver traded below $56 this week, down more than 50% from its January spike highs of $120.

Copper hit a record high of $6.70 in early June, and traded ~10% lower this week as gold and silver fell.

Stocks

New record highs this week for the DJIA (52,600), Nasdaq, Russell 2000, Nikkei, EuroStoxx 50 and Kospi. The S&P did not make new highs this week. GOOG was added to the DJIA, replacing VZ.

While NAZ futures reached a new record high this week, the index closed near its lows on Friday, generating a second weekly Key Reversal down in the last four weeks.

The S&P has also had two weekly Key Reversals down in the last four weeks.

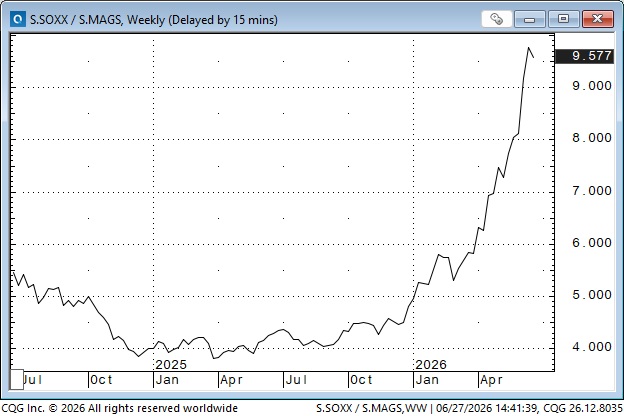

Semiconductors continue to lead, but there’s a lot of rotation between sectors/stocks and wicked s/t price volatility.

Here’s a chart of the Soxx/Mag7 ETFs showing the dramatic YTD outperformance of the semiconductor sector over the “Hyperscalers.” (Cheque cashers beating cheque writers.)

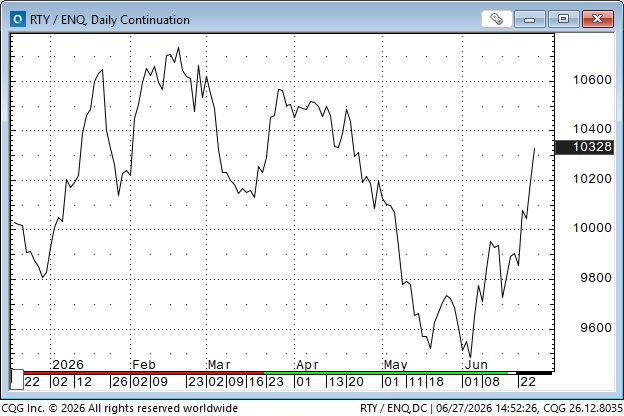

Another dramatic “rotation”: this chart shows the Russell 2000 gaining sharply vs the Nasdaq this month.

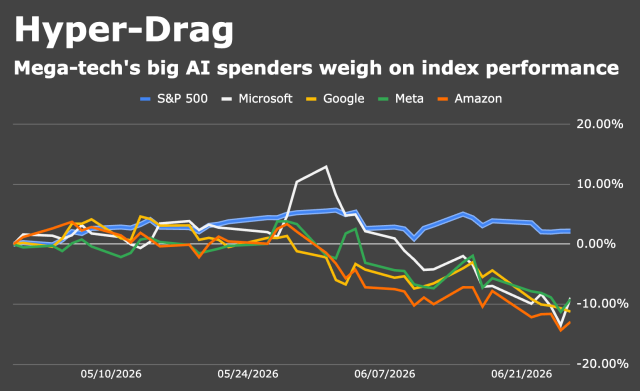

The S&P index has recently been outperforming the key Hyperscalers, a dramatic reversal from earlier this year.

SPCX began trading at $150 last week, rallied to ~$225, and then fell back below $150 mid-week.

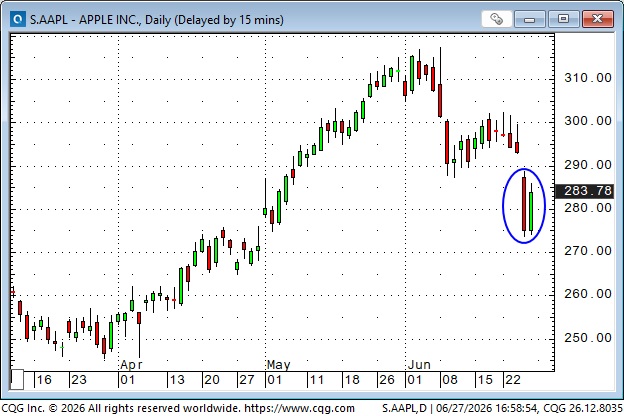

AAPL announced price increases on some products on Thursday, and the share price dropped (blue ellipse).

Risks

The S&P has risen over 100% from the 2022 lows, reaching new record highs in each of the last three months. The NAZ has tripled from the 2022 lows. The SOXX is up ~6X from the 2022 lows. Is a correction likely?

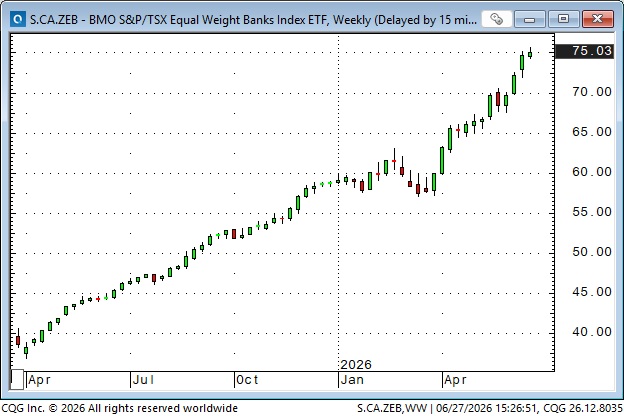

Canadian bank shares are up ~32% from the late-March lows, at new record highs (that’s 128% annualized for Canadian Bank shares, not junior miners!).

A zillion dollars is being spent on AI, and that spending has buoyed index prices. Will there be sufficient ROI? Will Chinese AI (nearly as good as American AI but way cheaper) be another DeepSeek shock, but on a grander scale?

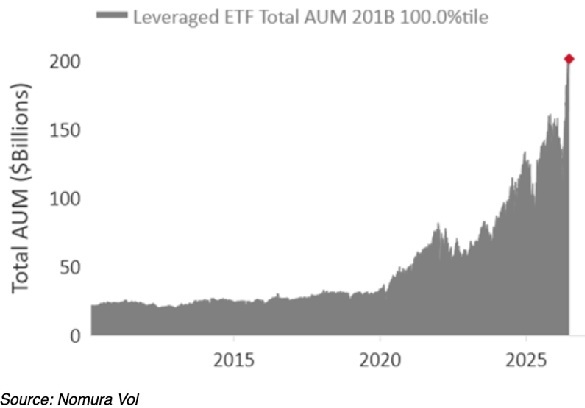

The biggest knowable (non-black-swan) risk may be overleveraged positioning.

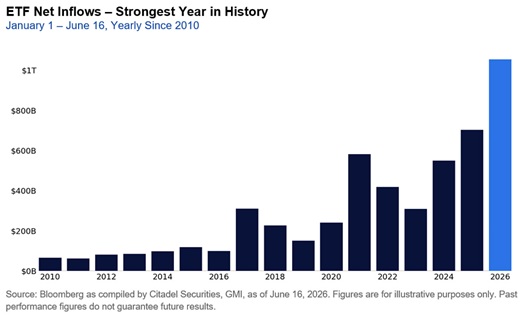

$200 billion in US leveraged ETF = ~$400 billion of market exposure.

Rebalancing: this coming week provides a month-end, quarter-end, and first-half-end rebalancing opportunity for institutional money. Most pension funds are more than “fully funded” to meet their actuarial future obligations. Will they decide to derisk?

Too much supply: Will the sale of more AI-related shares (IPOs and “insider” selling), together with more AI debt issuance, be too much for the market to handle?

Is there an asymmetrical positioning risk, with limited upside for a market priced for perfection?

Where there’s risk, there’s opportunity

For my short-term trading, I’m more inclined to be a seller than a buyer, BUT I’m very aware of the POWERFUL “Buy The Dip” mentality in the equity markets, so I pick my spots to get short, have stops in place, and trade modestly.

Grains

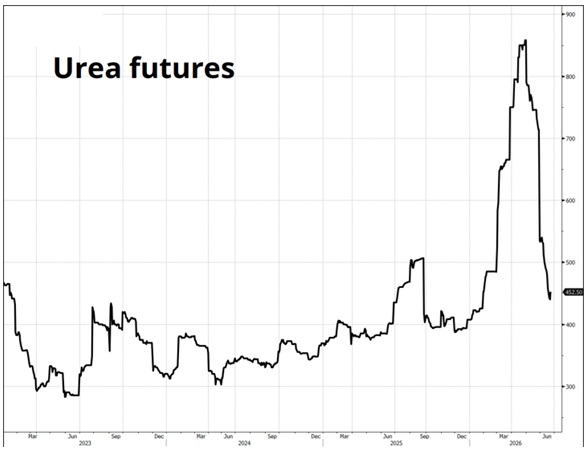

Remember the early days of the Strait of Hormuz closure? Instant experts predicted that not only would the world suffer a major energy crisis as 20% of oil supplies went offline, but people would also starve as fertilizer shortages caused crop shortages.

Here’s a chart of urea, the world’s most widely used nitrogen fertilizer:

Here’s a chart of December 2026 CBOT corn, with prices falling to life-of-contract lows this week:

My short-term trading

I started this week long August natural gas, a position I established on June 15. I’m still long, and the market has slowly inched in my favour.

I shorted and covered the S&P five times during the week and held a short position into the weekend. My S&P P&L for the week was a modest net gain.

My corporate trading account is 100% in USD and has had substantial unrealized FX gains over the last 8 weeks as the CAD tumbled. I bought CAD futures to hedge ~25% of those gains and may add more if CAD rallies.

The Barney report

Last week, I noted that Barney would have his first-ever haircut this week. I hoped the groomer could trim some of his undercoat to make life easier for him in the summer heat. The groomer did a great job, and Barney is happier than ever!

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed crude oil prices returning to pre-war levels, gold falling to an 8-month low and the wicked short-term price action in the equity markets. You can listen to the entire show here. My spot with Mike starts around the 58-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair June 27th, 2026

Posted In: Victor Adair Blog

Next: See You Next Month! »