ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 20, 2026 | Trading Desk Notes for June 20, 2026

Victor Adair

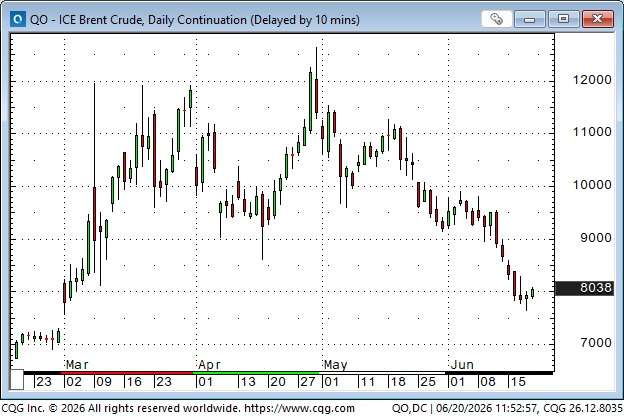

Crude oil prices spiked in March

Brent crude oil futures spiked in March as the US and Israel attacked Iran and as Iran retaliated. Prices rose in April as markets assessed that the war would last longer than initially thought, and amid concerns that the effective closure of Hormuz would cause physical shortages. In May, prices began to trend lower as shortages appeared less severe than expected and as the market began to price in a dampening of hostilities and a possible end of the war. This chart of front-month Brent futures shows prices are now back to levels seen in early March, as the “war risk premium” has substantially diminished.

This chart of front-month Nymex WTI differs from the Brent chart in some details, but the overall picture is the same: rising prices in March, slightly higher prices in April, followed by a decline in May/June back to the levels seen near the start of the war.

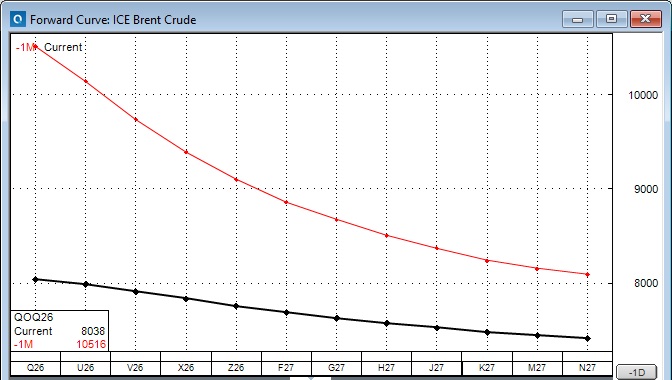

This chart of the forward Brent futures curve shows that the current backwardation (black line) is much less steep than it was one month ago (orange line) as the “war risk premium” has substantially diminished.

The MOU

The MOU signed by the US and Iran this week is a step toward ending the war. Traders are right to be skeptical that a definitive peace agreement will be reached anytime soon (Iran declared this morning that it was closing Hormuz again), and I will offer no opinion on who “won” the war. (I will try to stay focused on what markets are doing, not on what I think they should be doing!) Physical Dubai crude was reportedly trading this week at prices below pre-war levels.

Front-month wholesale gasoline futures rose sharply in March, rose further in April, and have declined somewhat over the last four weeks, but are still well above (~50%) where they were before the war started.

Higher energy prices resulting from the war in Iran have caused a sharp jump in inflation metrics, with CPI remaining above the Fed’s 2% target for over five years.

Warsh is the new Fed Chair

Warsh sounded hawkish in the presser following his first FOMC meeting as Fed Chair. He (repeatedly) stressed the need for the Fed to deliver price stability, and seemed genuinely disappointed that CPI inflation had remained above the Fed’s 2% target for over five years.

There has been a lot of “comment” about Warsh being “Trump’s guy,” and “everybody knows” Trump wants lower interest rates, so perhaps the market’s hawkish reaction (especially in credit and currency markets) was due to markets being “unprepared” for Warsh to sound SO hawkish.

Quote of the week on the Fed

“Veteran traders know to NEVER fade a genuine central bank surprise during the first 24 – 48 hours.” Stephen Innes, The Dark Side Of The Boom (I highly recommend traders check out Stephen’s Substack. I’m amazed at the quality and quantity of his market commentary.)

Interest rates

The December 3-month SOFR futures tanked in response to the FOMC policy announcement and fell further during Warsh’s presser (blue ellipse). The forward strip now prices a ~90% chance of a 25 bps hike in September, with another in December. As recently as early March (pink ellipse), the market was pricing ~50 bps of cuts by December. (So, a 100+ bps swing in market expectations for higher short rates). If (and it may be a big if) the decline in oil prices “feeds through” to lower CPI inflation, markets may cut back rate hike expectations.

While short rates were rising, bond yields fell on Wednesday and again on Thursday (blue ellipse). The bond market seems to like Warsh’s “tough on inflation” tone. Long bond prices have been trending higher since mid-May, in sync with falling oil prices.

Currencies

The DXY US Dollar Index rallied on Wednesday and reached 13-month highs on Thursday in a hawkish reaction to the Fed’s policy announcement and Warsh’s presser (blue ellipse). The idea of renewed “American exceptionalism” may also be supporting the USD as capital “comes to America” in search of opportunity in equity markets, and as the USA demonstrates energy independence. Interest rate differentials, a strong economy, strong employment and strong US corporate earnings also favour the USD.

Recent Commitments of Traders (COT) data showed that speculators in currency futures were heavily long the USD before the Fed meeting and likely added to that positioning on Wednesday/Thursday.

The Canadian Dollar has fallen ~3.5 cents against the USD since the beginning of May, with ~30% of that decline happening after the Fed meeting (blue ellipse). Interest rate differentials between the USA and Canada have moved sharply in favour of the USA over the last month, with the 2-year spread now ~140 bps.

The Euro also fell following the Fed meeting and Warsh’s presser, dropping to the low end of the range it has been in for the past 12 months.

The Japanese Yen has been in a relentless decline against the USD since the intervention spike(s) 6 weeks ago, and it appears to have traded to multi-decade lows following the Fed meeting (blue ellipse). There is obviously “intervention risk” at these levels, and COT data show speculators are “massively” short the Yen.

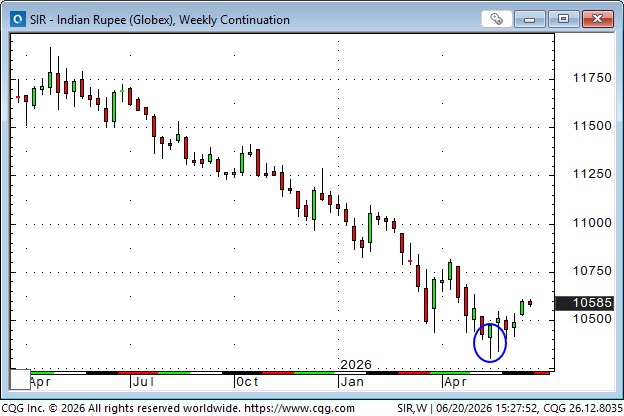

The Indian Rupee fell to record lows (blue ellipse) against the USD in May as higher oil prices (and oil shortages) added to India’s woes, but falling oil prices over the past few weeks have allowed the rupee to rally a bit, and it showed very little reaction to the Fed news.

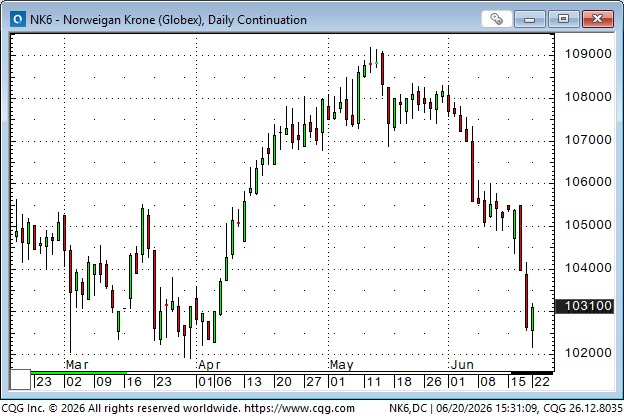

Higher oil prices rallied the Norwegian Krone in April/May, falling oil prices brought it back down in June.

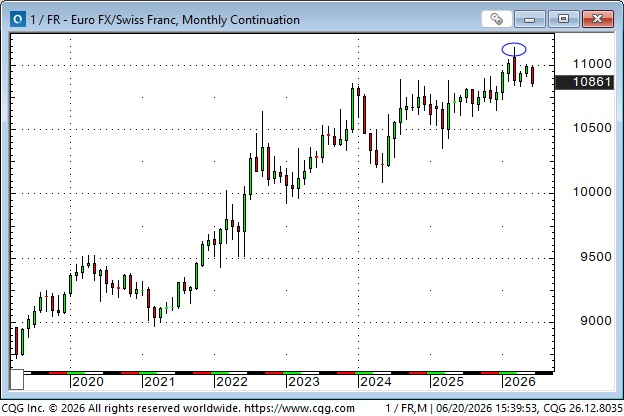

The legendary Swiss Franc traded at an all-time high (blue ellipse) against the Euro in January, gaining ~20% over the last 5 years.

Swisse has gained ~25% against the USD since 2022. The January high (blue ellipse) was effectively a record high, aside from a very brief spike in August of 2011 during the European Sovereign Debt Crisis.

Metals

Higher US interest rates and a stronger USD following the Fed meeting pressured gold this week (blue ellipse), with prices down ~$265 from Wednesday’s highs to Friday’s lows.

Friday’s Comex close was the lowest weekly close since early November 2025, with prices on the front-month Comex futures down ~$1,400 from January’s record highs.

Central Banks (with a long time horizon) continue to buy gold. However, I believe that FOMO speculative buying late last year and early this year is still in a net liquidation phase. If Warsh proves to be as “tough on inflation” as he sounded at his presser, that weakens the “debasement trade” thesis for buying precious metals.

Silver’s chart pattern over the last year or so is similar to gold’s, only much more dramatic (the silver price tripled from October 2025 to January, while gold rose “only” 38%, and silver fell nearly 50% from January’s highs to current levels, while gold is “only” down ~25%).

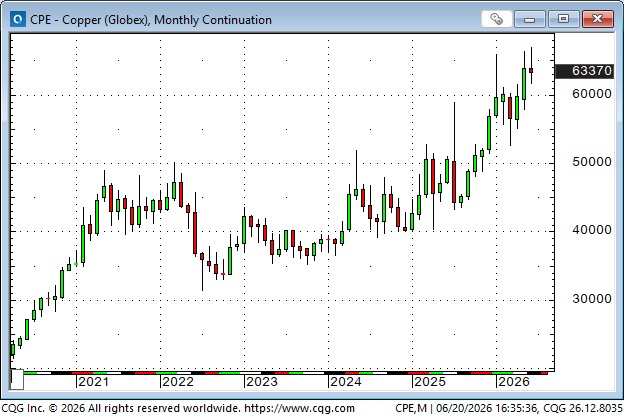

Comex copper prices have doubled in the last 4 years, reaching record highs this month.

Stocks

The leading global stock market indices remain at or near record highs. The S&P and Nasdaq futures dipped a bit on Wednesday (blue ellipse) following the Fed news, but recovered most of that on Thursday.

The TSE hit record highs on Wednesday ahead of the Fed news, but closed lower from Wednesday through Friday (blue ellipse).

The Nikkei didn’t blink on the Fed news, and closed the week at a new record high.

The South Korea ETF has become a “poster child” for tech/memory exuberance, and it closed the week at another record high.

One of my “below the radar” plays on the AI capex boom is CAT.

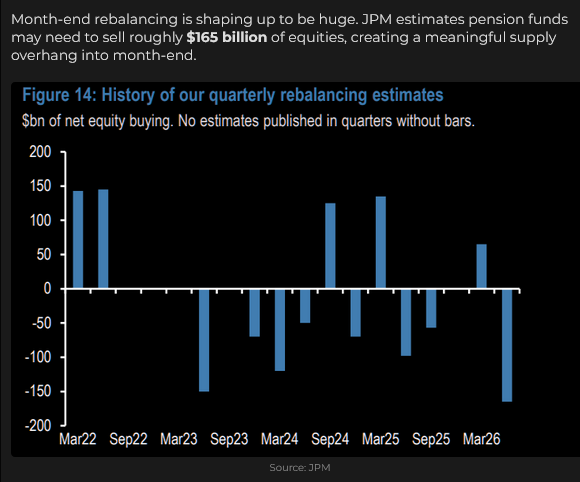

JPM thinks there could be a record-sized “rebalance” as equity markets approach the end of June.

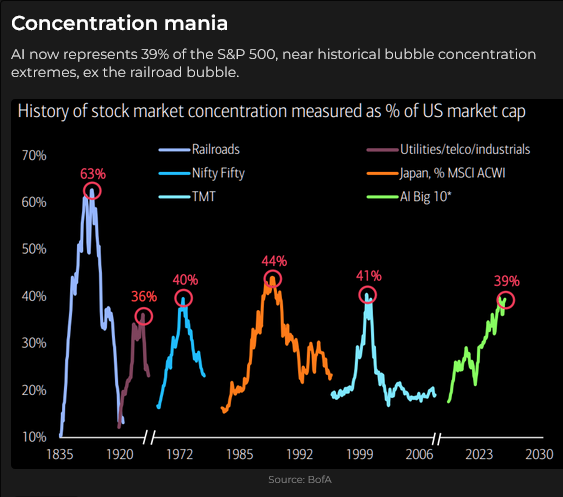

BoA is recommending caution.

Video clip of the week

Paul Tudor Jones: a 3-minute video on the possibility of mean reversion in the WAY over-leveraged stock market.

My recent short-term trading

I bought natural gas futures on Monday and held that trade into the weekend.

I bought WTI on Monday at 2-month lows after it gapped lower over the weekend, but stopped out early Tuesday as prices continued to fall.

I shorted the S&P on Tuesday when it reversed after failing to rally above Monday’s high and covered for a good gain on Wednesday when the market tumbled on the Fed news.

I re-shorted the S&P on Wednesday, thinking the price action in credit and currency markets was signalling a “big change” from the Fed, but I was stopped for a slight loss in the overnight market.

I feel like I’m back to trading again after “withdrawing” because of all the “noise” around “will they / won’t they” get a peace deal.

Quote of the week for traders

“If prices don’t validate a narrative, ignore the narrative.” Sir JJ, John Johnston, Alyosha writing Market Vibes on Substack. I’ve been reading JJ for the past two years (we both worked for Conti in the late 1970s/early 1980s) and I can’t recommend him strongly enough to traders – he is especially good on metals and oil.

Substack

I’ve been easing into Substack. I haven’t started posting the Trading Desk Notes there, but you can see some of the comments I make on the 41 different substacks I subscribe to.

The Barney report

The weather has turned hot here, and Barney is feeling the heat. I’m going to take him for his first haircut this week – hoping that losing some of that fur coat will make his life better. People who know about dogs tell me that Golden Retrievers should not get shaved, just a little trim, and my “groomer” agrees. I should have a photo of Barney with his new haircut for next week.

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed the market’s reaction to the MOU between the USA and Iran and the FOMC meeting with Warsh as Chairman for the first time. My spot with Mike starts around the 58-minute mark. You can listen to the entire show here. Don’t miss James Thorne, who regularly rocks my view on markets!

Listen to Jim Goddard and I discuss markets

I did my monthly 30-minute interview with Jim Goddard on today’s This Week In Money show. We discussed the MOU and what’s happened in energy markets recently, Kevin Warsh’s first FOMC meeting as Fed Chair, global equity markets at or near record highs, Gold and Silver under pressure, the surge higher in the US Dollar and how I’ve dealt with the wicked volatility in markets YTD. You can listen to the entire show here. My spot with Jim starts around the 9-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair June 20th, 2026

Posted In: Victor Adair Blog