ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

April 4, 2026 | Trading Desk Notes for April 4, 2026

Victor Adair

Bear market rally in the S&P?

The S&P closed at an 8-month low on Monday (blue ellipse), after closing lower for five consecutive weeks, and then rallied nearly 4% to Thursday’s close, even though Trump threatened to hit Iran very hard over the next 2 – 3 weeks in his Wednesday evening speech.

The nearly 300-point rally in the emini S&P futures (worth $15,000 per contract) from Monday’s overnight low to Wednesday’s day-session high (trend line) was fuelled in part by expectations (hopes) that Trump would announce some “winding up” of America’s war with Iran in his Wednesday evening speech. Short covering and month-end and quarter-end rebalancing may also have helped fuel the rally.

Trump’s speech (blue ellipse above) was not what the market wanted to hear, and the S&P gave back ~40% of the Monday-to-Wednesday rally ahead of the Thursday day-session opening. However, futures rallied sharply on Thursday morning and closed the week green for the first time in six weeks.

Trump’s 10-day “pause” expires this weekend; he posted a warning to Iran on Saturday morning, reminding them that they have 48 hours to reopen the Hormuz Strait (or make a deal) or Hell will rain down upon them.

Over the last few weeks, the S&P seemed to “de-risk” ahead of the weekends, yet this week the market closed near its highs despite Trump’s “beligerent” speech and the expiration of the 10-day pause. The S&P closed below the 200 DMA on March 19 for the first time since May 9, 2025, and has remained below it since then.

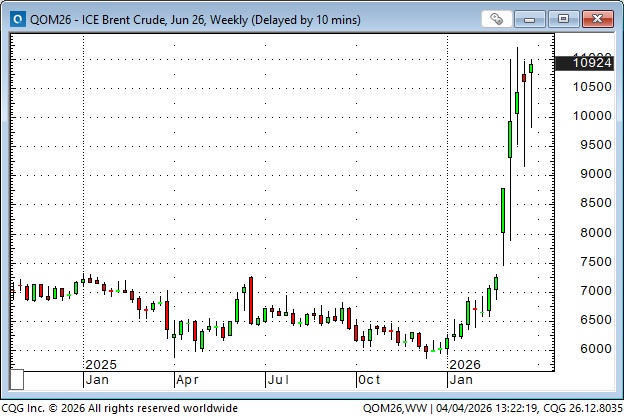

Crude oil was not as sanguine about the war’s prospects as the S&P, with both WTI and Brent front-month contracts closing at 4-year highs.

Richard Russell, the legendary publisher of the Dow Theory Letters, who died in 2015 at 91, often told his readers that “everybody loses money in a bear market.” People who are long the market obviously lose money as prices decline. Still, people who expect to make money by getting short in bear markets often lose money instead, because bear markets have lots of sharp short-covering rallies.

I suggest that this week’s S&P price action may be a short-covering rally because, despite the market “wanting” the war to wind down, the reality is that the US is continuing to expand their massive military presence in the Middle East in the face of Iranian intransigence, and the clock is ticking.

During the S&P’s 6-week decline from record highs, the weakest market sector was big-cap tech.

The soaring energy sector reversed hard this week after being the leading market sector YTD.

Before this week, the S&P closed lower for five consecutive weeks, while crude oil closed higher, yet this week, they both closed higher. Is the &P signalling that its decline from January’s record highs has “discounted” the Iran war, implying that a credible move towards “peace” in the Middle East would see the S&P soar? Or was this week’s S&P rally just a bear market rally, setting the market up for a sharp fall if the war escalates?

Crude oil is not fungible

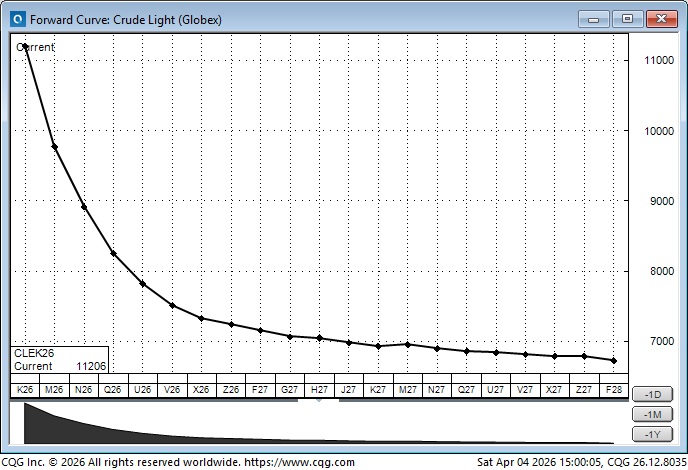

Market commentators often refer to “crude oil” as though it were a generic/fungible item, but in reality, there are many different kinds of crude oil, and prices currently vary dramatically depending on location, availability, and “when do you want it.” For instance, Nymex WTI for May delivery is ~$112, while December delivery is ~$72, implying that the market expects a substantial “standing down” of Middle Eastern tensions over the coming months.

Brent crude for June delivery on the London Intercontinental Exchange is ~$109, but if you want to buy actual barrels right now, Dated Brent is ~$140 in the Baltic. Check out www.Oilprice.com to see the many different types and prices of crude oil.

One reason commentators thought crude oil was “generic” was that the “arb” was pretty tight most of the time. n this chart, Brent traded at a $3.50 to $4.00 premium over WTI for most of the 15 months leading up to March. (The blue ellipse on the price spike in June 2025 was when the US and Israel briefly attacked Iran). The Brent premium over WTI rose dramatically in March as the difference in “location” suddenly became very important.

The “location factor” is very evident in natural gas, with domestic American prices near the lows of the past 15 months (after a spike on cold weather in January), while prices in Europe are substantially higher on worries of supply shortages.

Currencies

The DXY US Dollar Index fell to a 4-year low in late January as gold and silver reached record highs (and as Trump said he was unconcerned with the softer USD), but it has rallied 4-5% since then, as capital once again flows to the USA for safety and opportunity.

The Canadian dollar rose in the first few days of March after the US and Israel attacked Iran, but closed this week at a 4-month low, despite Canada being a net crude oil exporter. I think this decline has been driven by the CAD “realigning” with the weakness of other currencies vs the USD, and by a widening of the American forward short-term interest rate premium over Canadian rates. I don’t think the prospect of Alberta leaving Canada is weighing on the Loonie, but you never know!

Gold

Gold reached a record high in late January at ~$5,600, but was down by ~$1,200 two days later. It bounced back throughout February and nearly returned to record highs, but then fell again in March, even as war raged in the Middle East. The open interest in Comex gold has fallen to a 17-year low (silver OI is at a 13-year low), which may reflect the declining importance of the Comex in the world gold market, and/or the recent wild volatility may have caused participants to reduce their position sizing.

Credit

If the war were not leading the financial market news, the “troubles” in private credit would be front-page headlines. People invested in PC in the hopes of earning substantially more than T-bill yields, and were aware of the “locked-in” nature of the investment. PC was typically a “long-term” investment with leverage, so liquidity for redemptions was limited. The other “issue” was the (questionable) “valuation” (marks) that PC firms put on the investments. Once the redemptions started, they quickly turned into a flood, and PC firms had to restrict (gate) redemptions, exacerbating investor worries.

Quote of the week

“Victor, how can you trade wheat in Chicago if you don’t know the price of iron ore in China?” Jim Rogers, around 2010, when I was guest-hosting the Moneytalks radio show.

My short-term trading

I started this week with no open positions. I bought the CAD on Tuesday as it started to rally back from 4-month lows (and as the S&P was being aggressively bid higher from 8-month lows). The market rallied further on Wednesday, and I decided to take profits ahead of Trump’s speech that evening. I’m glad I did because the CAD fell like a stone on his speech. I was flat going into the long weekend.

The Barney report

Spring has finally arrived, and Barney and I are enjoying the warmer weather. Here’s a photo of him patiently waiting for me to finish writing so he can go back outside and run around in the warm sunlight. He’s my happy boy!

Listen to Mike Campbell and me discuss markets

We taped this morning’s Moneytalks interview on Thursday, ahead of the long weekend, and Mike and I discussed why I think we may have had a bear market rally in the S&P this week. You can listen to the entire show here. My spot with Mike starts around the 54-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair April 4th, 2026

Posted In: Victor Adair Blog

Next: