ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

August 30, 2025 | Trading Desk Notes for August 30, 2025

Victor Adair

The times they are a-changin’

August feels like the lull before the storm that strikes once we get past Labour Day. The meandering price action and low volatility we’ve seen may be replaced by strong directional moves and increased volatility. September is historically the worst month of the year for the stock market.

The leading American stock indices are near all-time highs, with the S&P up ~33% from the April lows, up ~9% YTD, with a ~23X forward PE. Corporate buybacks YTD are now over $1 trillion, with Wall Street banks expecting 2025 total buybacks to be in excess of $1.2 trillion, which would be a new record high.

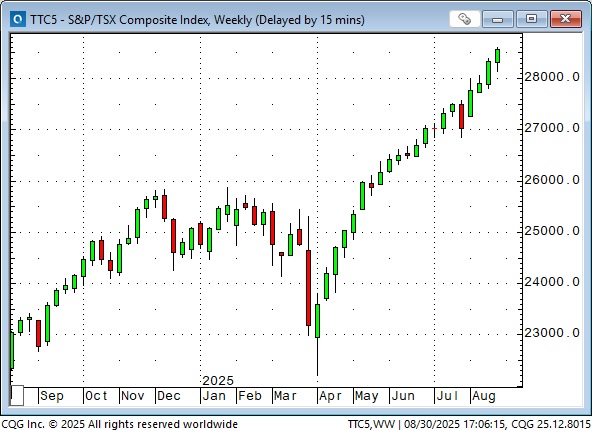

The TSE Composite index is up ~28% from the April lows, ~14% YTD, with an 18.5X forward PE.

NVDA had an astonishing run from the April lows, but has closed red for the past three weeks. The company’s earnings over the past three months have averaged about $750 million per business day.

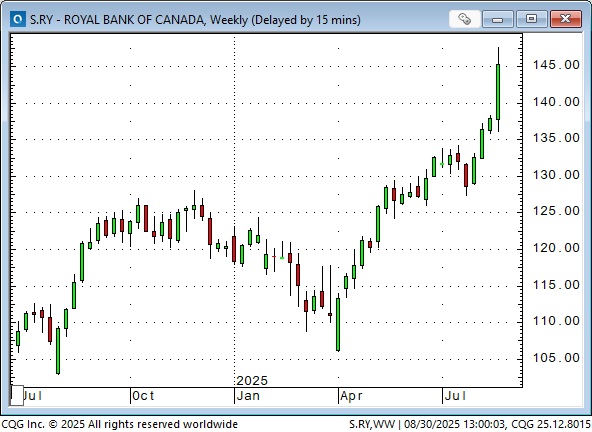

Leading North American bank shares have rallied to new all-time highs recently, perhaps invigorated by the prospect of lower short-term interest rates and a steeper yield curve.

Chinese stocks have “come alive” recently, after nine months of sideways price action, but the rally may be a “late-in-the-day” speculative surge. As Stephen Innes (a Canadian veteran trader living in Thailand) writes on Substack, “The true accelerant isn’t growth fundamentals, it’s leverage – margin debt sloshing in the tank like gasoline.”

Trump and the Fed

Trump has been pressuring Powell to cut interest rates aggressively. He apparently wants lower rates to reduce the cost of servicing US government debt and to stimulate the US economy. He may also expect lower interest rates to weaken the USD; he believes the “too-high” USD contributes to trade deficits.

Some commentators believe that Trump is “over-reaching” his authority by trying to control the Federal Reserve. These individuals also believe that undermining the Central Bank’s independence will lead to chaos in the financial markets and will erode the credibility of American monetary policy, both domestically and internationally.

If Trump gets a “compliant” Federal Reserve, some analysts expect lower short-term interest rates but higher long-term interest rates, as the Fed “goes soft” in its fight against inflation. Inflation is likely to rise if the US has both a stimulative fiscal and monetary policy. (No kidding!)

Higher bond yields could lead to the Fed instituting yield curve control (the Fed buys unlimited amounts of government bonds) to keep bond yields down. Additionally, lower short-term American interest rates may cause the USD to weaken against other currencies; however, different countries may also cut rates to prevent their currencies from appreciating, thereby initiating a “currency war.” There could be a wide range of “unintended consequences” if Trump effectively controls the Fed.

Market reaction to the Trump/Fed story has been relatively limited in August, at least compared to some analysts’ expectations. Currencies have gone sideways in a narrow range, bond yields are marginally higher, and the leading stock indices remain near all-time highs. Gold may be the outlier, rising to new record highs.

Quote of the week – relevant to the Trump/Fed story

“There are no solutions, only trade-offs.” Thomas Sowell

Listen to Mike Campbell and me discuss the Trump/Fed story on this morning’s Moneytalks show. You can listen to the entire show here. My 8-minute discussion with Mike starts around the 49-minute mark.

Bonds

US long bond prices spiked on the much weaker-than-expected employment report on August 1 (blue ellipse), but have drifted sideways in a relatively narrow range over the last three weeks.

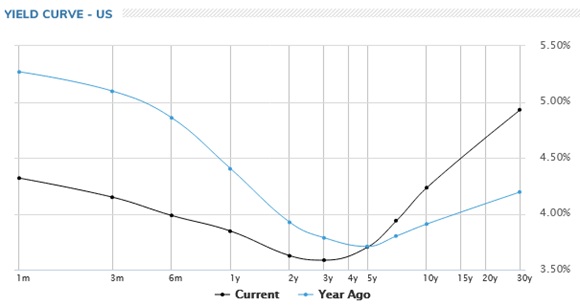

The US yield curve has steepened substantially over the past year, with long-term rates rising while short-term rates fell.

The September 5 employment report could jolt the bond market, but may be “difficult” to interpret given the recent leadership change at the BLS. A few days later, on September 9, the BLS is scheduled to release their annual benchmark revisions to the employment data for the April 2024 to March 2025 period, and that too may be challenging to interpret, but a substantial revision lower may cause markets to start pricing a 50 bps cut from the Fed on September 17. (See this Zerohedge article for a comprehensive review of BLS benchmark revisions.)

International bond markets have “some” correlation with one another, so it may be helpful to note that the yield on the British 30-year bond is near 29-year highs at ~5.6%. The 30-year US yield is currently at ~4.93%.

The Japanese 30-year yield is currently trading at ~3.19%, a record high.

Currencies

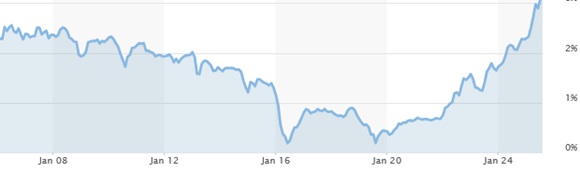

The DXY US Dollar Index was trading at 2-month highs at the beginning of August, but tumbled on the August 1 weaker-than-expected US employment report (blue ellipse) and has since moved sideways in a narrow range. August is often a quiet month for FX trading, as European markets are on vacation.

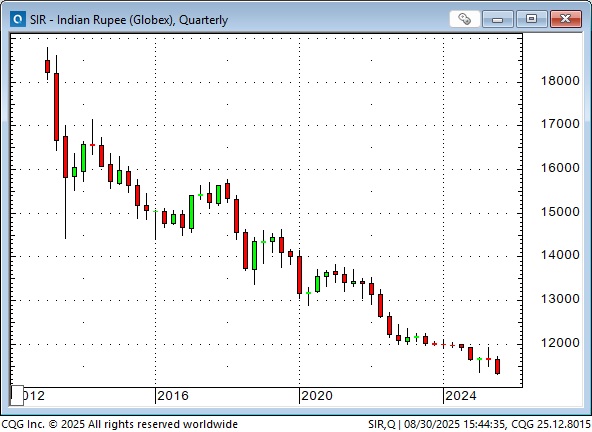

The Indian Rupee fell to an all-time low against the USD this week as tariff “issues” between the US and India pressure the currency. (One way for a country to reduce the “sting” from American tariffs is to devalue its currency.)

The Rupee has been trending lower since the 1980s, but especially since 2012, when Abe introduced his Three Arrows policies to stimulate the Japanese economy. These policies led to the Yen falling from all-time highs against the USD, and other Asian currencies broadly tracked the Yen lower. (Asian currencies, as a group, are grossly undervalued against the USD on a PPP basis.)

The open interest and volume in the Brazilian Real caught my eye this week. OI is at a record high, but trading volumes this week (~350,000 contracts) were higher than those of the Swiss franc, the Pound, the CAD, the AUD, the NZD, and the MXN. The record OI and the volume surge are related to the monthly roll, and the OI is almost exclusively in the front month (same as the MXN). I suspect carry trade traders are involved in the BRL, given its short-term interest rates of ~15%. However, I’ve never traded it, so I’ll have to keep an eye out for opportunities.

Precious Metals

Comex gold futures closed at a record high this week, with the December contract rising ~$100 from last Friday’s close. Weekly volume was modest. I’m unsure if gold experienced a technical rally, if people were buying due to the “Trump/Fed” effect, if the higher prices are attributed to rising speculative sentiment in China, or if there’s another reason.

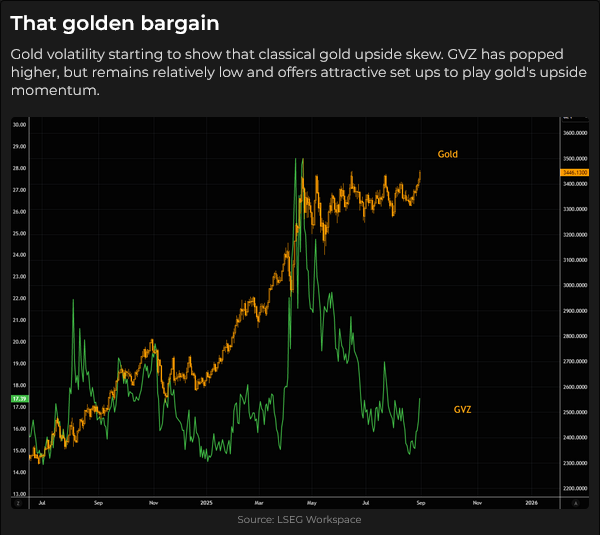

Gold option volatility typically rises when the gold price rises (S&P option volatility typically rises when the S&P falls.) In this chart, the green line represents gold VOL, and the gold line shows gold prices. Note the VOL spike as gold soared to record highs in March/April this year, and (VOL being a mean-reverting thing) how VOL collapsed as gold went sideways from May through July.

Comex silver also rallied with the front-month contract closing over $40 for the first time since 2011. The December contract closed this week $1.38 above last week’s close. Weekly volume was a 2-month high.

Energy

Natgas turned higher this week (a classic weekly Key reversal) after hitting multi-month lows last week.

My short-term trading

I started this week with a small short position on the S&P. I was stopped for another tiny loss when the algos spiked the market following the NVDA quarterly report.

It’s August, and I’ve been travelling to visit friends and family for the past two weeks, so I haven’t had any commitment to trading. I’ll start the post-Labour Day markets with a clean slate.

The Barney report

My wife tells me that Barney was sad when I was away, often waiting at the front door for me to come home. He is always happy to see me when I get home, and I’m delighted to see him! That boy loves a good stick!

The Archive

Readers can access any of the weekly Trading Desk Notes from the past eight years by clicking the Good Old Stuff-Archive button on the right side of this page.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair August 30th, 2025

Posted In: Victor Adair Blog

Next: The Cycle of War & Revolution »