ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

March 8, 2026 | Trading Desk Notes for March 7, 2026

Victor Adair

Let’s start with crude oil

Nymex front-month April WTI traded above $92.50 on Friday, up ~$25 (38%) on the week, the largest ever weekly price rise, on the highest ever weekly trading volume (over 14 million contracts at 1,000 barrels per contract = roughly the equivalent of 140 days’ worth of total global crude oil production traded on the Nymex this week).

$100 is a major psychological level. If WTI trades through $100, the impact on other markets will increase exponentially.

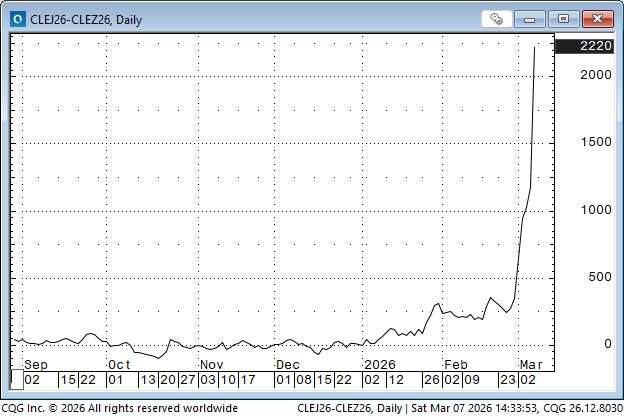

Here’s the daily chart:

Here’s the weekly chart: The RSI at ~88% appears to be the highest since October 1990 during the Kuwait war, indicating overbought conditions. WTI reached a high of ~$130 in early March 2022, following the Russian invasion of Ukraine.

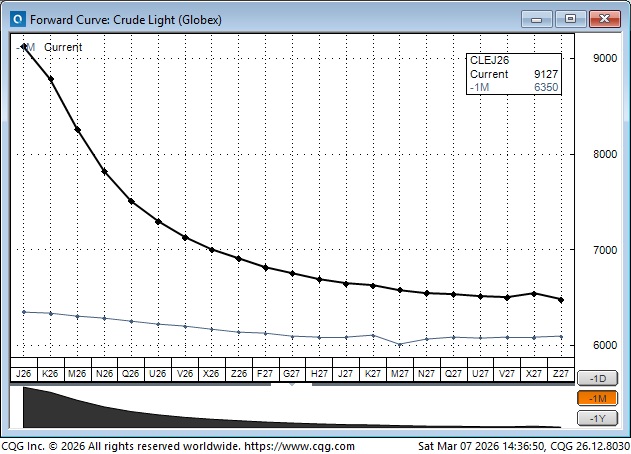

Price gains of nearby WTI contracts outperformed deferred months this week, with December 2026 rising only ~$5 on the week, closing at ~$69, about a $22 discount to April.

Here’s the April/December spread over the last 6 months. April and December were both trading ~$57 at the beginning of 2026; now, April is ~$22 premium to December. This dramatic steepening of the forward curve may be the market’s way of signalling that the current high risk premium in crude oil futures will be substantially reduced by year’s end.

Here’s how the forward curve is priced: Friday’s close is the strong black line, and the other line is what the curve looked like a month ago. That is a “wild” steepening of the curve in response to the Iran conflict.

Nymex WTI option VOL exploded higher this week, especially on Friday, when April options (10 DTE) were trading at 140 to 150% VOL. The gold line on this chart appears to be May (40 DTE) WTI option VOL. The blue line is the VIX.

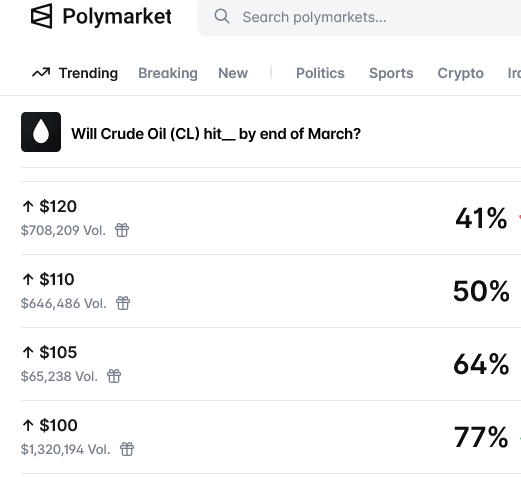

Here are Polymarket’s odds (as of March 7) for WTI’s price by the end of March.

Dutch TTF natural gas prices doubled this week after Qatar’s exports to Europe stopped. 100% stopped. And Putin is musing about not delivering any more natgas to Europe because they don’t show him “respect.” (No comment from me on EU and UK energy policies and how they got into this mess.)

The XLE Energy Sector ETF has closed higher for the last 11 consecutive weeks, up ~30% since mid-December. The energy sector has been the strongest S&P sector YTD.

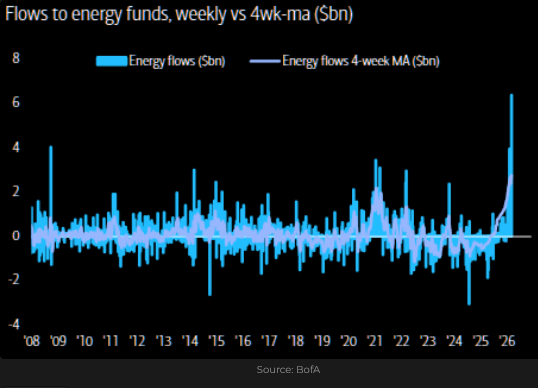

BoA shows strong flows to the energy sector YTD.

Duration is a huge factor in crude oil pricing

The longer Hormuz remains effectively closed, the higher prices will rise for crude, natural gas, refined products and chemicals; a function of “just in time” supply chain pricing, as well as the “shut-in” risk that grows as crude oil producers run out of storage capacity, and have to start shutting down producing wells (which will take weeks to restart if/when Hormuz reopens). Iraq and Kuwait are reportedly already shutting down some production.

The dramatic rise in crude oil prices on Friday may have been driven by a report from Natasha Kaneva at JPM, indicating that large-scale shutdowns may start within a couple of days, rather than the couple of weeks markets had previously been pricing in.

In a geopolitical sense, the question now becomes, “How resilient is Iran?” It may have limited ability to defend itself against aerial bombardment, but if it can (effectively) shut down Hormuz with cheap drones, oil prices may continue to rise.

One last thought on the Iran conflict. If either side starts hitting desalination plants, we will know this conflict is about total victory or total defeat.

Fertilizer

25 to 30% of global fertilizer raw materials pass through Hormuz. Share prices of fertilizer companies were sharply higher this week.

Chicago wheat prices closed this week at a two-year high. A possible supply shortage and/or higher-priced fertilizer may have contributed to the price rise.

One last thought on energy markets

Diesel engines require urea (DEF or AdBlue) to operate. It’s a tight “just-in-time” supply chain market, with between 30 and 50% of global demand supplied by Middle East exports. If Hormuz remains closed, millions of diesel engines will stop working. Unintended consequences?

Currencies – The USD and the CAD are petro-currencies

The DXY US Dollar Index traded at a 4-year low in late January, but rallied sharply early this week, up ~4.5% from the January lows. The USD is higher because 1) in “times of trouble,” capital flows to the USA for safety, 2) the US is a net energy exporter, 3) before the attack on Iran, trader positioning, especially in the Euro, was significantly net short the USD, and 4) the Fed is less likely to cut interest rates if rising energy prices lead to higher inflation.

The Euro plunged against the USD on Monday and Tuesday (the Eurozone is a net importer of energy, the USA is a net exporter), but steadied later in the week. The long “tails” on the Tuesday to Friday candlesticks (blue ellipse) may indicate that the Euro found support around the 116 level. There was “chatter” that the ECB may raise interest rates if rising energy prices push inflation higher.

While other G10 currencies were falling early in the week, the CAD stayed “even” with the USD, and on Friday, with WTI prices soaring, the CAD rallied hard, posting the highest weekly close since June 2025. The CAD is a true petro-currency! (Justin Trudeau must be weeping!)

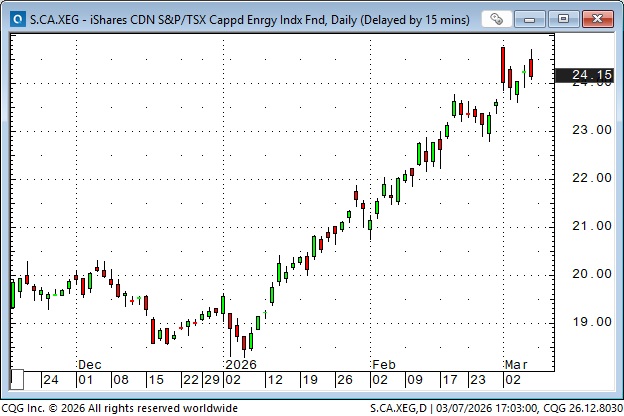

The XEG, a leading Canadian energy ETF, rallied to an 18-year high this week.

The Mexican and Brazilian currencies broke down early this week as the USD rallied. Those currencies had an extended run since early 2025 as carry trade “beneficiaries” (borrow Yen or Swiss francs at low rates, invest in Mexican or Brazilian high-yield s/t paper, and wear diamonds!), and complacency may have had a rude awakening this week.

Equities

The S&P opened lower on Monday in response to the weekend attack on Iran, but then rallied to close above Friday’s close (blue ellipse) as WTI gapped nearly $10 higher on Monday but then fell back ~$5.

On Monday, there seemed to be a “belief” in the markets that the conflict would be over quickly. The S&P chopped up and down for the rest of the week in virtual lock step with changes in the price of WTI. When WTI soared on Friday, the S&P fell hard, posting the lowest weekly close in nearly four months.

6800 has been support since November. An old-school technical rule is that once support is broken, it becomes resistance. It looks like support has been broken.

The VIX is ~30%, the highest it’s been since April of last year, when, you know, the Great Liberation Day event.

If the S&P trades lower again next week, I think there is a significant risk that “systematics” (CTAs and VOL control funds) will start selling, which may lead to broad market weakness, unless we hear that Trump has made a deal with Iran. (But: even if Trump says the war is over, the market has to believe that Iran won’t hit tankers in the Hormuz.)

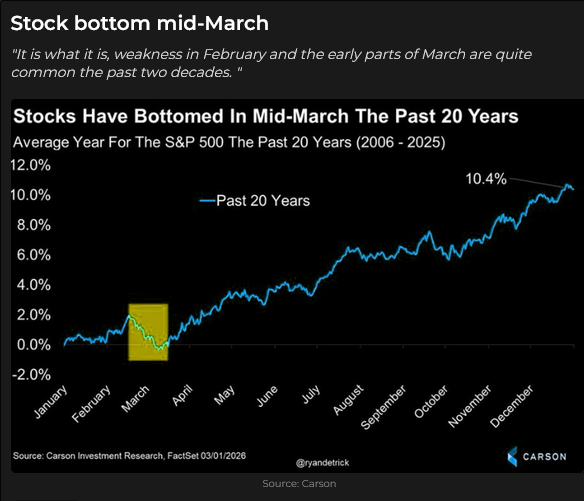

If you prefer to be bullish on equities, you might want to hold your breath for the next couple of weeks, and then hope the seasonals kick in.

Defence stocks rallied this week, with the ITA ETF reaching record highs, but closed the week lower. Perhaps the market was due for a correction after rallying nearly 100% from the April 2025 lows.

As reported here last week, the leading Korean ETF rallied nearly 200% from April 2025 lows to last week’s highs, but plunged ~22% to this week’s lows (on MASSIVE volume) as sharply rising crude oil prices hit high-flying risk assets. (Check Bob Farrell’s Rule #4: “Exponentially rising or falling markets usually go further than you think, but they do not correct by going sideways.”) Stock markets outside the USA were stronger than the S&P in January and February, but that ended on Monday, when “risk-on” shifted to “risk-off.”

Bonds

Bond prices gapped higher Sunday afternoon to 4-month highs, but reversed sharply and traded lower every day this week, posting the largest weekly decline since Liberation Day in April 2025. Surging energy prices are toxic for bond prices. War is inflationary. Friday’s NFP employment report was far worse than expected, and the bonds went bid for a few minutes, but it didn’t last, and prices made new lows for the week.

I remember when traders treated the monthly NFP report as the most important scheduled event of the month. Those days are long gone. The market no longer respects or trusts that report.

Gold

Rising real yields (and a rising USD) may be keeping a lid on the gold market.

Private credit

I wrote about emerging private credit concerns last week, and the news didn’t get any better this week with BlackRock restricting withdrawals. To quote my old friend, Dennis Gartman, “There’s never just one cockroach,” or, as my dear old Grandmother used to say, “It never rains, but it pours.” Private credit feels like it could become another meaningful problem.

My short-term trading

I bought the S&P a couple of times early this week (if the market won’t fall on soaring WTI, what will it do if the conflict ends?). I was money ahead each time, but I was stopped for small losses, and then I decided to stop trading for the week. I was puzzled by breakdowns in cross-asset correlations and decided to back away. I rediscovered this week that I’m more risk-averse than I thought! Thankfully, as my dear, departed friend, Peter Appleby, told me so many times, “There’s a rumour going around that the markets will be open again next week!”

Quote of the week

Markets always overstate the risk of geopolitical events. Marko Papic

Trader humor

There’s a rumour going around that Trump is doing a “beautiful deal” with Cuba. There will be direct flights to Havana from all major US airports, and they’re going to rename the place Margaritaville.

The Barney report

Barney is now four and a half years old. He’s 80 pounds of muscle and bone. He’s become much better at obeying my voice commands (sophisticated stuff like SIT and WAIT), unless he sees something that needs chasing, like a rabbit or a deer, and then all bets are off.

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed how the conflict with Iran was driving a sharp rise in crude oil prices, which was affecting all markets. You can listen to the entire show here. My spot with Mike starts around the 50-minute mark. I highly recommend that readers listen to the entire show – Mike has some brilliant insights, and my friends Lance Roberts and Andrew Ruhland also deliver valuable advice.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past five years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair March 8th, 2026

Posted In: Victor Adair Blog

Next: Has the Great Taking Begun? »