ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

March 21, 2026 | Trading Desk Notes for March 21, 2026

Victor Adair

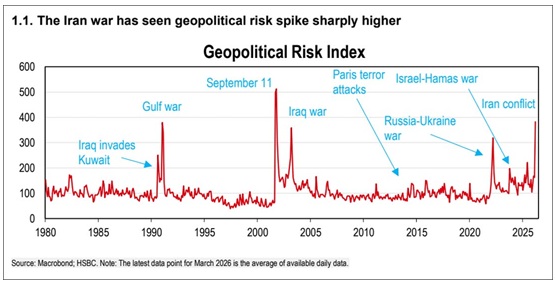

Certainty of energy supply is more important than price

Energy prices have soared since the initial attacks on Iran, with knock-on effects hitting all markets, but if the war continues, countries that rely on energy imports will have every reason to worry about physical supply, regardless of price.

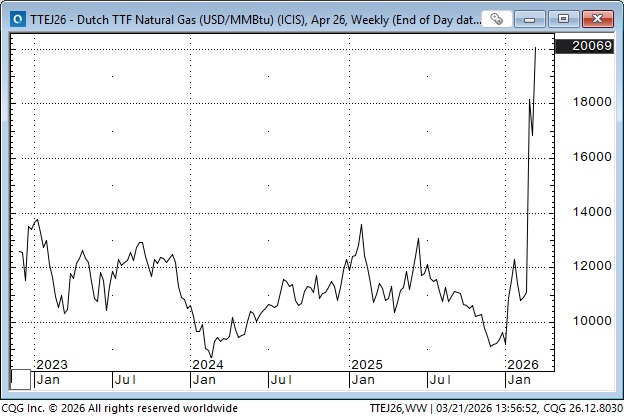

Natural gas prices in Europe have spiked following the start of the Iran war, even though Qatar provides less than 10% of European LNG imports (the USA delivers ~60% of those imports). Roughly speaking, European prices are ~$22 per MMBtu, while US prices are ~$3 per MMBtu.

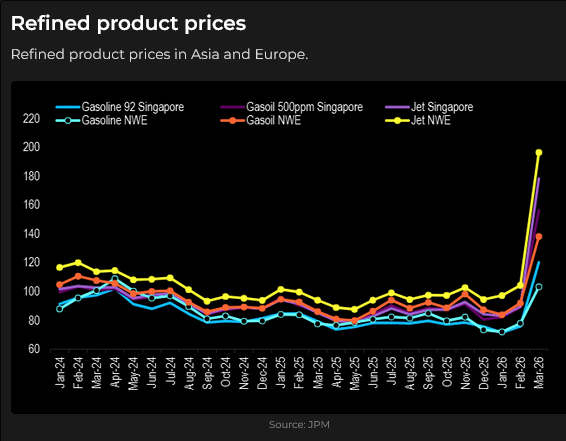

Prices of refined products (gasoline, diesel, jet fuel, etc.) have risen more sharply than crude oil prices. This chart shows prices in Singapore and NW Europe.

India imports ~90% of the crude oil it uses, with ~60% of that coming from Persian Gulf countries. About 50% of its natural gas usage is imported, with Qatar its primary supplier.

The Indian Rupee has been under pressure since the Iran war began, dropping to record lows on Friday.

New Zealand produces virtually zero crude oil and has no domestic refining capacity. They import 100% of their refined fuel demands. They consume 100% of their declining natural gas supply and have no facilities to import or export LNG. If the countries that export refined fuels to New Zealand (Japan, Korea, Singapore, Malaysia) decide to (need to) restrict exports, New Zealand will likely be forced to ration supplies. If the war continues, more and more countries that rely on imports will likely have to ration supplies.

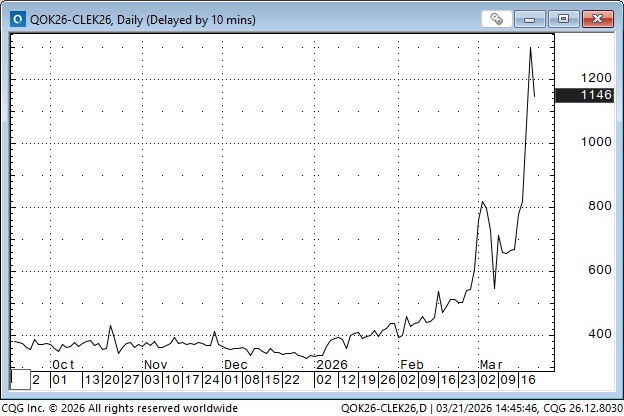

It is a bifurcated world: countries are either self-sufficient in energy or dependent upon increasingly fragile supply chains. As headlines about the war continue to drive volatility in oil prices (and other asset markets), Brent (international prices) has risen sharply relative to WTI (American prices), especially this week, as the escalation of targets (Iranian South Pars gas field / Qatar gas processing facilities) increased the risk of long-term supply shortages. This chart shows Brent prices rising sharply relative to WTI this week.

Central banks are worried that higher energy prices will lead to higher inflation

A dozen central banks held scheduled meetings this week. Australia raised rates as expected, but all of the CBs warned about likely higher inflation due to higher energy prices. Forward markets have gone from pricing 1 to 2 interest rate cuts from central banks this year to now pricing increases.

US short-rate futures for December 2026 have increased 85 bps since the start of the Iran war. (Falling prices on these charts mean higher interest rates).

Canadian short-rate futures for December 2026 have increased by ~90 bps.

Treasury bond futures closed this week at an 8-month low. The yield on the US 30-year bond was 4.95% at Friday’s close.

The drop in bond prices reflects the market’s concern that rising energy prices will drive higher inflation, but some folks might argue that, historically, higher oil prices have led to a weaker/recessionary economy, which would likely mean higher bond prices (unless there is stagflation). These same folks might also argue that there should be “safe haven” buying of US Treasuries during a war and when stocks are falling. They may be right, but in a world of soaring fiscal deficits, it’s hard to imagine a sustained bond rally.

The combination of uncertainty over the war, sharply higher energy prices, sharply higher interest rates and continuing worries about private credit added to the pressure on global stock markets

The S&P has been trending lower since the Iran war began, as US Treasury yields have been trending higher.

The S&P closed this week at a 6-month low, trading below the 200-day average for the first time since May 2025. Friday’s close was ~7% below January’s all-time high.

The DJIA reached a record high of ~50,500 in February, but has fallen more than 5,000 points (~10%) from the highs to this week’s lows, closing below its 200-day MA for the first time since June 2025.

The TSE reached a record high on March 2 (closing at a record high that day as energy stocks soared), but has since fallen ~10% (despite the energy share ETFs being up ~30% YTD).

The airline ETF, JETS, has been under pressure from the “double-wammy” of the DHS shutdown and sharply higher fuel prices.

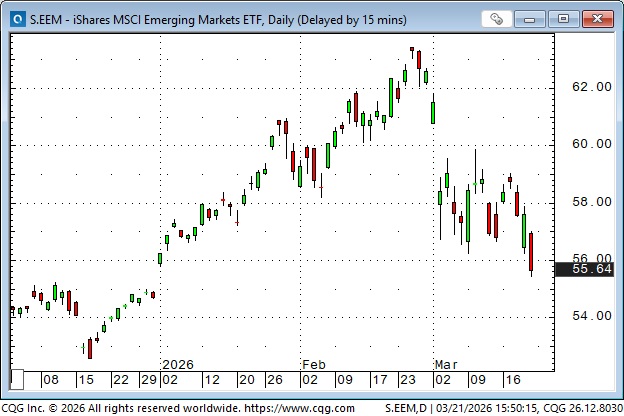

The emerging markets ETF, the EEM, soared ~65% from last April’s lows to an all-time high in late February, but has tumbled ~12% to new lows for 2026. I can’t think about people investing in emerging markets without also thinking about Donald Coxe’s famous line: “Emerging markets are markets you cannot emerge from in an emergency!”

Gold

Comex gold futures reached an all-time high of ~$5,600 at the end of January, but closed this week ~$1,100 (~20%) lower at ~$4,500. The market tumbled ~$500 from Wednesday’s high to Friday’s low on what appeared to be relentless liquidation. This week’s loss was the largest weekly (percentage) loss since February 1983, when, ironically, (according to Gemini) “The sharp drop in gold prices in February 1983 was primarily caused by large-scale selling by Middle Eastern oil-producing countries (OPEC members), who were forced to liquidate gold reserves to raise cash following a sharp drop in oil revenues.” This week, gold, silver, and copper all registered their lowest weekly closes of 2026 YTD.

In my January 31, 2026, TD Notes, I wrote that January’s price action in gold and silver reminded me of the price action in January 1980 when gold and silver spiked to record highs, and then fell dramatically, and did not make new highs for years (28 years for gold, 45 years for silver).

Currencies

The DXY US Dollar index fell to a 4-year low in January (as gold and silver were soaring to record highs), but rallied over 5% to last week’s 10-month highs, with half of those gains coming after the start of the Iran war, as the USD attracted safe-haven flows.

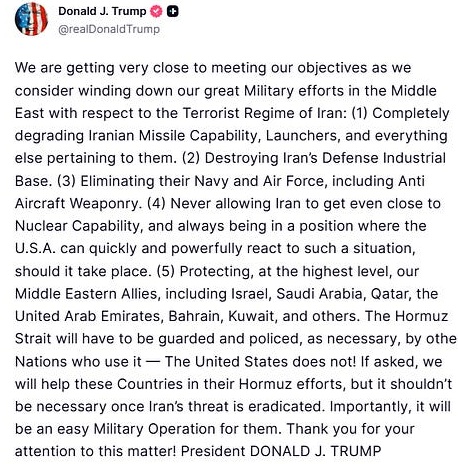

Did Trump change everything with his Friday afternoon post?

My first thought was that it was interesting that he waited until after the US markets were closed for the weekend to post his note. (Just like it was interesting that the first US and Israeli strikes against Iran happened when the US markets were closed for the weekend).

I think it is entirely possible (probably likely) that some of the selling in the gold market, in Treasuries and even the US equity market came from Middle Eastern countries. Trump would know, and he seems to be sensitive to what the markets are doing.

I’m not going to try to “second-guess” what motivated Trump to make his statement, but I think that gold, bonds and stocks will open higher Sunday afternoon as a result of his post, unless Israel and/or Iran decide on further escalation.

Cuba

Cuba has been ignored lately, with the focus on the Middle East. Still, two Russian ships (one carrying crude oil, the other refined fuel products) are en route to Cuba, with one expected to arrive within the next couple of days and the other a few days later. Trump has an effective embargo on Cuba. Will he let these ships pass?

Videos

If you don’t subscribe to Doomberg (or even if you do), I recommend watching this interview with him where he sets out his views about what may happen once the Iran war is over. (Hint: China is going to play a bigger role in the ME).

Jeff Currie is a veteran energy analyst. Check out this 10-minute Bloomberg video to learn why he has a great reputation.

Thoughts on trading – what are we trading?

It took me years, decades maybe, to learn enough about markets to ask, “What are we trading?” When I was younger, I was confident that I knew “what” was moving markets. Beans were up because there was too much rain in Illinois and Iowa. I didn’t even know that Brazil grew beans. These days, I’m confident that I don’t know “what” is moving markets, and I’m also confident that whatever it is, it probably is not whatever is most obvious. I try to follow the “news” with an open mind, but my motto is “trade the price, not the story.”

Mark Douglas died over 10 years ago, but his book “Trading In The Zone” is a classic trader’s book. Check out this great 10-minute video about how Mark taught serious traders how to get better.

My short-term trading

I started this week short OTM Treasury bond puts that I had sold last week. They were due to expire on Friday, and I closed them out for 4 ticks on Wednesday, thinking the risk/reward of holding them to expiry didn’t make sense. It was the right thing to do because the bonds tanked on Friday, and I would have had a substantial loss rather than a decent profit.

I sold two-week OTM bond puts right on the low close on Friday. Bonds had been falling like a rock, VOL was WAY up, and I decided the premium was large enough to warrant trying to pick a bottom.

I bought the S&P on Thursday when the market started to rally after falling ~200 ticks from Wednesday’s high, but I was stopped for a small loss in the O/N market, which was just as well, because the S&P plunged on Friday.

First quote of the week

Second quote of the week

I can’t tell you how many times I heard clients say something like this during my 45 years as a commodity broker:

“Let’s give it a couple more days. I’m sure this market is going to turn around.”

The Barney report

Barney and I were out on a long walk yesterday, the Spring Equinox, and the sun actually felt warm for the first time in months. Barney was having a great time racing around the forest trails, and then he jumped up on this boulder to get a good look around. He is a happy dog!

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed the possibilities of some countries having to ration energy products if the Iran War continues. You can listen to the entire show here. My spot with Mike starts around the 55-minute mark. Don’t miss my good friend Joseph Schachter, a world-class energy analyst, starting around the 6-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past five years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Victor Adair March 21st, 2026

Posted In: Victor Adair Blog

Next: