ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

August 18, 2022 | “Housing Recession”: Sales Plunge to Lockdown Levels, Active Listings Surge, Prices Begin to Dip as Price Reductions Spike, Investors Pull Back

Wolf Richter

Inventory and supply of previously-owned homes of all types – single-family houses, condos, co-ops, and townhouses – surged, and sales plunged, amid sky-high prices that have been made impossible by 5%-plus holy-moly mortgage rates. And so the red-hot housing market turns into a “housing recession,” as the National Association of Realtors called it today, after the National Association of Home Builders had already called it that on Monday.

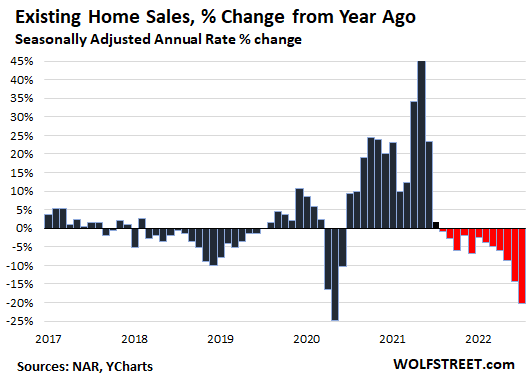

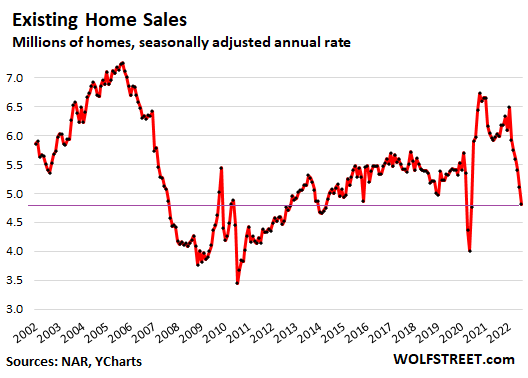

Sales plunged by 5.9% in July from June, the sixth month in a row of month-to-month declines, and by 20% from a year ago, the 12th month in a row of year-over-year declines, based on the seasonally adjusted annual rate of sales (historic data via YCharts):

Sales of single-family houses plunged by 19% year-over-year, and sales of condos and co-ops plunged by 30%, according to the National Association of Realtors in its report.

Sales dropped in all regions on a year-over-year basis:

- Northeast: -16.2% yoy.

- Midwest: -14.4% yoy.

- South: -19.6 yoy.

- West: -30.4% yoy.

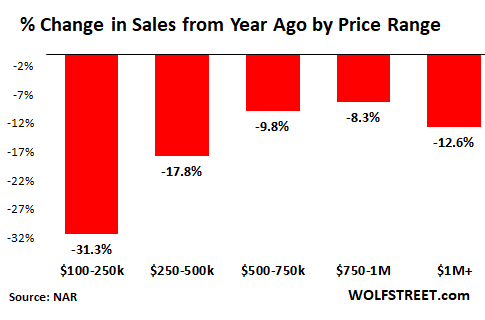

Sales dropped in all price ranges but dropped the most at the low end and at the very high end (over $1 million) for the first time in this cycle.

The drop at the high end is in part related to plunge in sales in the most expensive coastal markets in California, such as the San Francisco Bay Area (-37%), and Southern California (-37%), according to the California Association of Realtors.

Sellers and buyers too far apart on price.

“We’re witnessing a housing recession in terms of declining home sales and home building. However, it’s not a recession in home prices,” the NAR report said.

The fact that sales are plunging like this is an indication that sellers and buyers are too far apart on price, that buyers moseyed away from these sky-high prices, and these buyers are still out there, but a lot lower, while many sellers are still hanging on to their illusions, and deals aren’t happening. Sellers just pull their property off the market after a few weeks to wait for a better day.

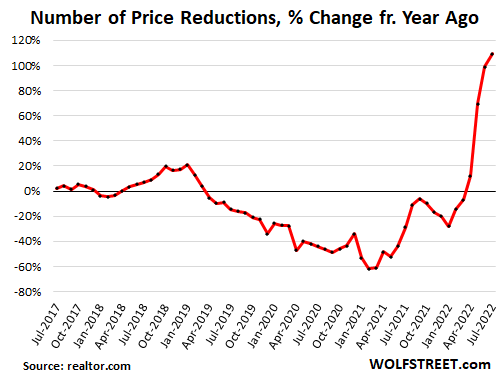

But some sellers are getting the message, and price cuts have been spiking. In July, the number of sellers that reduced prices of their properties on the market spiked by 31% from June, and more than doubled (+109%) from July last year, according to data from realtor.com. If pricing is realistic, a sale will happen, but pricing too often is not realistic yet, as documented by the plunge in sales:

Sales volume has plunged because of unrealistic pricing. But the deals that did get done, got done at still very high prices, which is why so few deals got done.

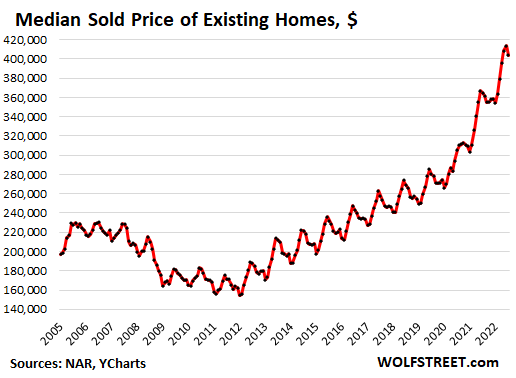

The median price dipped to $403,800 in July, which whittled down the year-over-year increase to 10.8%. As big as it sounds, it was the smallest year-over-year increase since July 2020, after having spiked by 25% last year (data via YCharts):

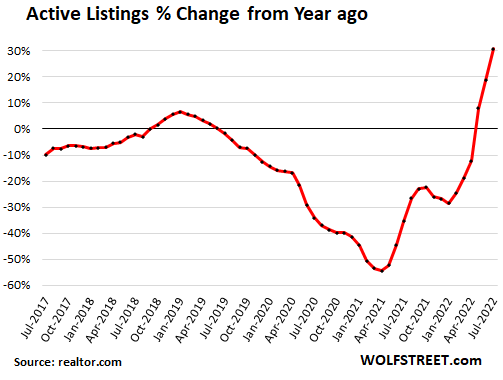

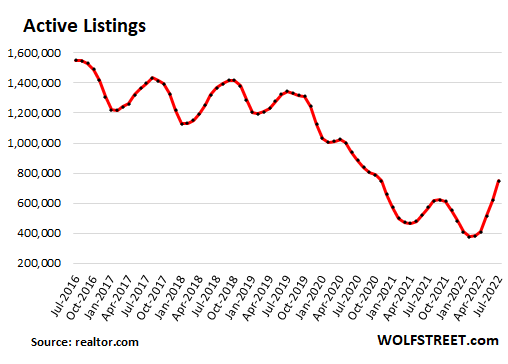

Inventory suddenly comes out of the woodwork.

Active listings – total inventory for sale minus the properties with pending sales – jumped in July by 20% from June and by 31% from July last year to 748,000 homes, the highest since November 2020, according to data from realtor.com:

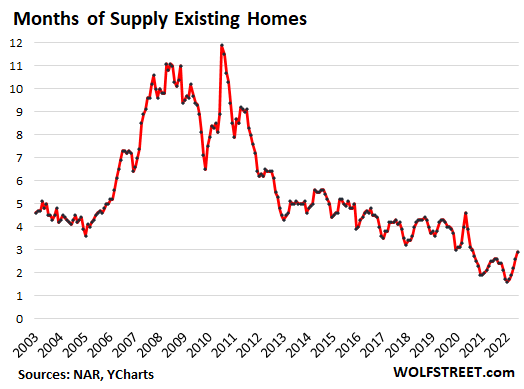

Supply of homes listed for sale, according to NAR data, jumped to 3.3 months at the current sales rate, the highest since June 2020, and up by 27% from a year ago, having more than doubled since January (data via YCharts):

Investors, second home buyers, all-cash buyers pull back.

Individual investors or second-home buyers purchased 14% of the homes in July, down from a share of 16% in June and May, from 17% in April, 18% in March, 19% in February, and 22% in January, according to NAR data. In other words, individual investors and second-home buyers are pulling back faster than others.

“All-cash” sales, which include many investors and second home buyers, dipped to 24% of total sales, down from a share of 25% in June and May, and down from a share of 26% in April.

Among the biggest institutional buyers of houses, American Homes 4 Rent has already laid out why it is pulling back from buying in this market where prices have started to drop in many cities where it is active amid a pile-up of inventories, particularly of new houses. “We need to be patient and allow the market to reset,” it said.

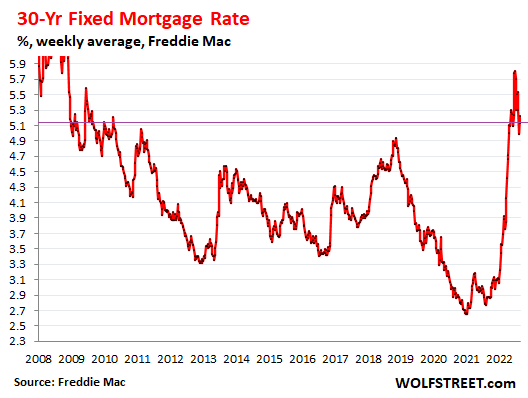

Holy-Moly Mortgage Rates don’t work with sky-high prices.

Mortgage rates – called “holy-moly” because of the sounds homebuyers make when they see the potential mortgage payment – have been between 5% and 6% since mid-April. The daily rate tracked by Mortgage News Daily today is 5.48% for the average 30-year fixed rate mortgage. The Mortgage Bankers Associations weekly measure, released yesterday, came in at 5.45%. Freddie Mac’s weekly measure, released today, ticked down to 5.13% for the most recent reporting week. These rates compare to 2.9% a year ago.

These 5%+ mortgage rates are still mind-bogglingly low, with CPI inflation at 8.5%, as the Fed is backing off years of interest rate repression. But home prices are mind-bogglingly sky-high, and the two don’t mix, and prices will have to come down to meet the buyers.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter August 18th, 2022

Posted In: Wolf Street

Next: Pelosi – Taiwan – China »