ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 6, 2022 | State of the American Debt Slaves: Borrowing More to Buy Less due to Raging Inflation

Wolf Richter

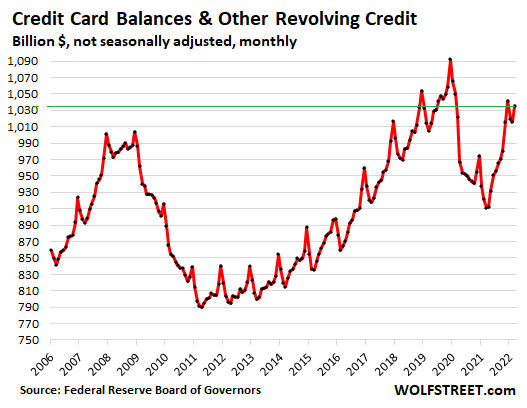

Credit card balances ticked up 1.9% in March from February, not seasonally adjusted, to $1.036 billion, according to the Federal Reserve today. Compared to three years ago, March 2019, the last March before the pandemic, this was up by only 3.0%.

In other words, credit card balances are now just 3% higher than there were three years ago, after three years of inflation, including raging inflation for the past 12 months that increased the prices of nearly everything that consumers buy with their credit cards.

Over the three years, during which credit card balances rose a total of 3%, CPI inflation jumped by 13%. In other words, even credit card borrowing cannot keep up with this raging inflation, LOL, and that their credit card debts, the most onerously expensive debt, is growing more slowly than inflation over the longer term is for once a good thing for the American debt slaves:

Note in the chart above how consumers paid down their credit cards and other revolving credit during the first 12 months of the pandemic, and then they started charging again, gradually getting back to where they’d been on a nominal basis, but never catching up with inflation and a “real” basis.

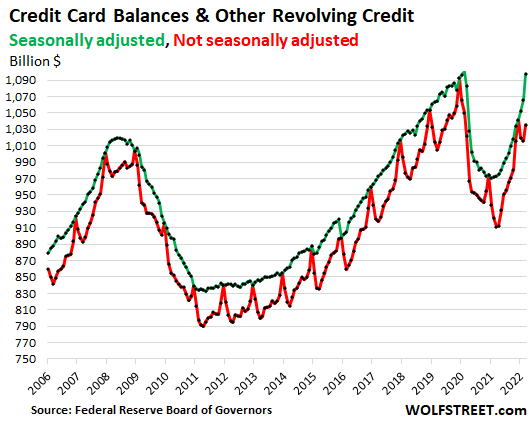

Seasonal adjustments galore.

Consumer spending is very seasonal, and so is the usage of credit cards. Balances peak in December every year, and fall off in January and February. Massive seasonal adjustments are used to smooth this out. In March, these seasonal adjustments added $62 billion to the revolving credit balance and pushed the figure up to $1.097 trillion, seasonally adjusted, up by 2.9% from February.

This chart shows the actual revolving credit balances (red line) and the seasonally adjusted revolving credit balances (green line):

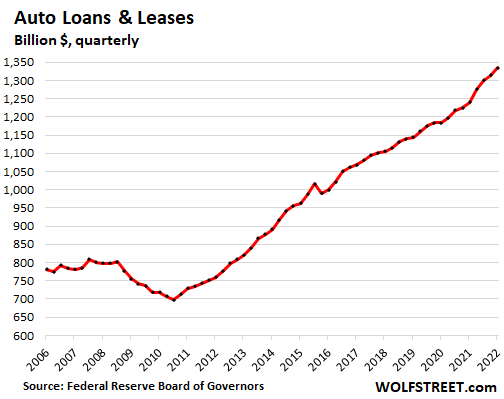

Auto loans and leases in the first quarter – this is quarterly data, not monthly – jumped by 1.6% from Q4 and by 7.6% year-over-year, to a record 1.34 trillion, according to the Federal Reserve today.

This increase in auto loans and leases came amid a plunge in purchases of new vehicles and a drop in purchases of used vehicles, accompanied by holy-moly price increases.

- The CPI for use vehicles in Q1 spiked by 35% year-over-year.

- The CPI for new vehicles jumped by 12.5%.

These ridiculous price increases had the bizarre effect that consumers cut way back on their purchases of vehicles but borrowed a lot more to finance them:

The majority of auto loan balances outstanding derive from the purchase of new vehicles, rather than used vehicles, due to their much higher prices – the average transaction price of new vehicles in Q1 was around $47,000.

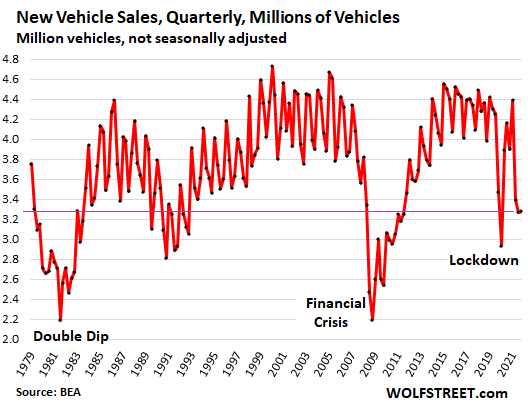

But new vehicle sales in Q1 plunged by 15.8% year-over-year and by 17.7% from Q1 2019, to 3.28 million vehicles, the worst Q1 since 2011, and right back where they’d been in 1979. This was due to semiconductor shortages, supply-chain chaos, production delays, inventory shortages, and nearly empty dealer lots.

The number of used vehicles sold retail by dealers in Q1 fell, including by 15% year-over-year in March.

So what you’re seeing reflected in the increase of the auto loan balances are two big factors, going in the opposite direction, with the ridiculous price increases winning the game:

- A plunge in the number of vehicles sold

- A ridiculous spike in vehicle prices.

So this is the status of the American debt slaves: They’re having to borrow a lot more to fund the purchases of a lot less because everything has gotten so much more expensive, thanks to this raging inflation.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter May 6th, 2022

Posted In: Wolf Street

Next: Zelensky & World War III »