ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 18, 2022 | Housing Bubble Getting Ready to Pop: Mortgage Applications Plunge amid Holy-Moly Mortgage Rates, Croaking Stocks, Ridiculous Home Prices

Wolf Richter

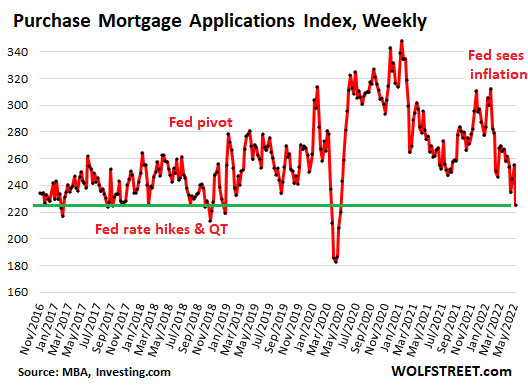

Pieces of evidence are lining up in increasing density. The number of potential future homebuyers that need a mortgage has been thinning out for months. Today, another milestone: Applications for mortgages to purchase a home dropped 12% from the prior week and were down 15% from a year ago.

In its report, the Mortgage Bankers Association today added that “prospective homebuyers have been put off by higher rates and worsening affordability conditions” – namely the ridiculous spike in home prices over the past 18 months, on top of the surge in prior years, combined with mortgage rates returning to what would have been still very low rates a couple of decades ago.

The MBA’s Purchase Mortgage Applications Index dropped to the lows of late 2018. Back then, the Fed had been hiking rates, and its QT had pushed mortgage rates to a hair over 5%, volume was drying up, and prices had started to wobble and were coming down in some markets. But inflation was below the Fed’s target, and Trump had been keelhauling Powell on a daily basis. Powell caved, mortgage rates dropped again, and volume and prices took off again. Now raging inflation is the dominant economic concern, and the Fed is determined to get it under control (data via Investing.com):

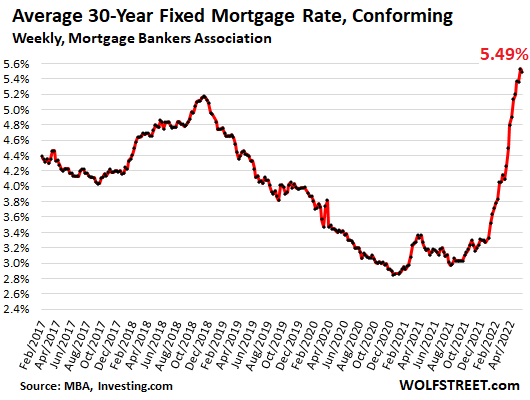

Holy-Moly Mortgage Rates.

The average 30-year fixed mortgage rate with conforming balances and 20% down this week eased a tiny bit to 5.49%, according to the MBA today, from the prior week’s 5.53%, both the highest holy-moly mortgage rates since 2009 (data via Investing.com):

Croaking stocks get blamed.

And it’s not just mortgage rates: The MBA added that “general uncertainty about the near-term economic outlook, as well as recent stock market volatility, may be causing some households to delay their home search.”

In this context, “volatility” always means sagging stock prices, because no one complains about upward volatility, and stocks are croaking. I mean, not every day, because we’ve had some sharp bear-market rallies, but they don’t last long, and then stocks skid to lower lows. It’s unnerving for people who’ve come to expect eternal and easy riches from stocks, and had built their whole future on this theory.

If you were going to borrow your down-payment by taking out a margin loan against your soaring stocks, you may now have second thoughts, that’s for sure. I mean, look at the sh*tshow going today, with the Nasdaq down 4% at the moment, subject to change.

Cryptos were not mentioned by the MBA, and that’s a good thing because they’re just gambling tokens. But some bigger cryptos have already collapsed to essentially zero. Others are on the way. Bitcoin has plunged about 58% from November, and is down 25% from a year ago.

And that’s not confidence-inspiring for people who’d expected to use their crypto gambling wins to buy a house with. Those that got out early, made it. And those that believe in HODL (“hold on for dear life”), well, they’re going to have to keep believing.

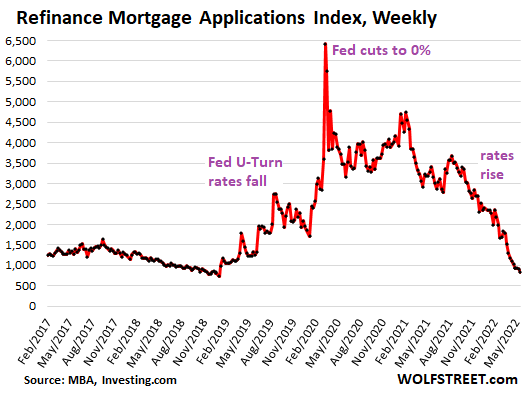

Refi applications have collapsed for months.

Applications for mortgages to refinance an existing mortgage dropped further, having plunged all year amid these holy-moly mortgage rates, with the MBA’s Refinance Mortgage Applications Index hitting the lowest point since the end of 2018.

Cash-Out Refi vs. No Cash-Out Refi.

But there is a split between cash-out refi, where needy homeowners are still feeding at the trough of the home-price spike, and no-cash-out refis, where homeowners are trying to lower their monthly payment by getting a new mortgage with a lower rate.

The AEI Housing Center tracks this split, using a different methodology than the MBA to account for mortgage applications.

Cash out refis are motivated by the need to take a big chunk of cash out of the home, and mortgage rates are a secondary issue. So cash out refis are continuing, but have dropped by 42% year-over-year, to the lows of early 2019, according to the AEI’s Housing Center.

The share of cash-out refi mortgages insured by the FHA – includes subprime mortgages and low down-payment mortgages – rose to 27% of all cash-out refi mortgages, up from a share of 10% at the beginning of the year.

“This indicates that higher risk borrowers are experiencing more stress due to inflation – not a healthy trend,” the AEI said. They’re doing cash-out refis with holy-moly mortgage rates to pay for inflation? Oh boy… Thank god that only the taxpayer is on the hook here from get-go, and not the banks, which means that the Fed can let this one rip.

No cash-out refis are motivated by lower mortgage rates to reduce the mortgage payment and save money every month. And those lower mortgage rates are now history. In the current reporting week, no cash-out refis have collapsed by 93% year-over year.

This means the end of the monthly savings from lower mortgage payments, and the end of these savings getting spent on goods and services, and thereby another pillar of support under consumer spending has been kicked out from under it.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter May 18th, 2022

Posted In: Wolf Street

Next: Bear Market Update »

You are missing the mark 1. Low Housing inventory. 2. 25% cash sales 3. Seller’s will not sale due having to attain a higher mortgage rate. For Housing prices to drop 20-30% it will probably take years.