ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

March 16, 2022 | Gazillion Miles Behind the Curve, the Fed Gets Hawkish: More Rate Hikes, “Faster and Much Sooner” Quantitative Tightening

Wolf Richter

Folks kept saying for many months that the Fed is “trapped,” that it can never raise interest rates, that it can never end QE, that it can never-ever shrink its balance sheet. And now the Fed has ended QE, and it has hiked its key policy rates by 25 basis points today, and it indicated that rate hikes are on the table at every meeting this year – seven more – and that there’s “certainly a possibility” that this might include 50-basis-point hikes, Powell said, and that the details of the balance sheet shrinkage (Quantitative Tightening) could be announced “as soon as” at the next FOMC meeting in May, Powell said, and that the balance-sheet shrinkage will be “faster and much sooner” than last time.

The Fed – the most reckless Fed ever – is a gazillion miles behind the curve. CPI inflation is raging at 7.9%, not including the effects of the recent spike in energy prices. But the Fed did move today, and it moved with hawkish twists, in terms of how many rate hikes this year and next year, and how soon QT would start.

The Fed today:

- Hiked by 25 basis points its target for the federal funds rate to a range between 0.25% and 0.50%. St. Louis Fed president Bullard voted against it; he wanted to hike by 50 basis points.

- Hiked the interest it pays the banks on reserves by 25 basis points, to 0.40%.

- Hiked the interest it charges on Repos by 25 basis points, to 0.50%.

- Hiked the interest it pays on Overnight Reverse Repos by 25 basis points, to 0.30%.

- Hiked the primary credit rate it charges banks by 25 basis points, to 0.50%.

- Confirmed end of QE: Decided to keep the level of assets on its balance sheet steady, and will only buy securities to replace maturing securities.

You’ve come a long way, baby, since the last meeting.

The median projections by the members of the FOMC have dramatically changed since their last meeting in December.

GDP growth projections got slashed, inflation projections got jacked up, and interest rate projections more than doubled for the end of 2022.

Today’s median projections vs. those from the December meeting:

- Growth in real GDP for 2020: now +2.8% (still above average growth); down from +4.0%

- PCE Inflation for 2022: now +4.3%; up from +2.6%

- Core PCE inflation for 2022: now +4.1%, up from 2.7%

- Federal funds rate by end of 2022: 1.9%, up from 0.9%

- Federal funds rate by end of 2023: 2.8%, up from 1.6%.

Hawks show up on the “Dot Plot.”

The “dot plot” is where members of the FOMC get to project their view of where the target range should be by the end of the year 2022, and in future years. On the dot plot today, the median projection for the federal funds rate was 1.9%, more than double from the last meeting of 0.9%.

But seven of the 16 members projected the federal funds rate to be above 2.13% by year-end, with 5 of them projecting a federal funds rate between 2.38% and 3.37%. That last one must have been Bullard.

“Every meeting is a live meeting,” Powell said several times during the post-meeting press conference, meaning that a rate hike is on the table at each meeting, and there are seven more meetings.

When asked if there could be a 50-basis point hikes among them, he said that it was “certainly a possibility” that the Fed “will move more quickly than projected now.”

Quantitative tightening coming soon.

The FOMC is now “finalizing details” about the balance sheet shrinkage, Powell said. More details will be outlined in the minutes, to be released in three weeks, he said. An announcement of the balance sheet shrinkage could come “as soon as” the meeting in May. But one thing is already clear: the shrinkage will be “faster and much sooner” than it was last time he said.

Last time was from late 2017 through mid-2019, which included a phase-in period and a $50 billion per-month cap on the pace of the asset shrinkage.

Inflation is now #1 priority, according to Powell.

It was a whole litany. Some tidbits from the press conference: “Price stability is an essential goal,” a “precondition for strong sustained labor market,” he said. “You cannot have maximum employment without price stability,” he said. “We have to restore price stability”

“We’ve had price stability for a long time and maybe come to have taken it for granted. Now we see the pain. I’m old enough to remember what high inflation is like,” he said.

“If we knew then what we know now, it would have been appropriate to move earlier” with rate hikes, he said. Which is funny; lots of people, including me the little guy, “knew then” – over a year ago – that inflation was developing into a massive problem very quickly.

Powell pointed out several times that the economy was strong, and that the labor market was historically tight, “too tight,” with 1.7 job openings for every unemployed person, as he kept pointing out, and that the economy and the labor market can “handle tighter monetary policy.” And I have long agreed with that. It was a huge series of massive policy errors to have waited this long.

“How far behind the curve?”

It’s funny how this went down at the press conference. Powell was asked several times in different ways how and why the Fed had gotten so “far behind the curve,” and why the Fed “made the choice to let inflation run longer above price stability” by not hiking rates sooner. There was some real pushback on Powell for having brushed off and ignored the inflation monster for over a year.

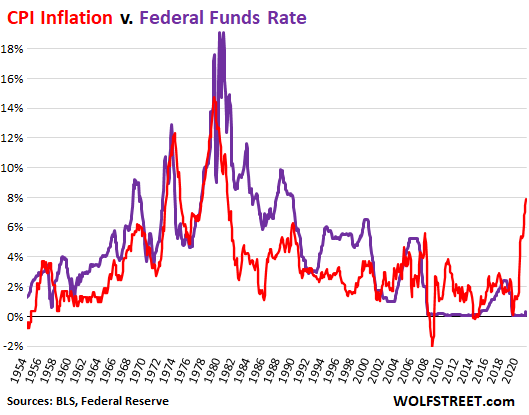

This pushback named explicitly the ridiculous negative “real” interest rates, with the effective federal funds (EFFR) rate at 0.08% before today, and CPI inflation raging at 7.9%, making it the most negative “real” EFFR ever, at -7.8% before today, and about -7.55% going forward.

In the data that goes back to the 1950s, there were only two occasions when CPI inflation shot through 7.9% on their way up: October 1973, when the EFFR was 10.8%; and August 1978, when the EFFR was 8.0%. After the rate hike today, the EFFR is going to be around 0.33%!

These record negative interest rates constitute a record amount of fuel that the Fed is still pumping on the raging inflation fire, and today’s rate hike was way too little, and way too late. Note the tiny uptick in the EFFR going forward, compared to the spike in CPI:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter March 16th, 2022

Posted In: Wolf Street