ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

October 17, 2021 | Not Getting Better: Relentless Retail Inventory Squeeze amid Shortages & Supply Chain Chaos

Wolf Richter

The holiday selling season is approaching, and a whole litany of weird shortages is ricocheting through the economy. Stuff suddenly gets hung up somewhere, on a ship, or in a port, and then ends up somewhere else, or it’s on backorder for months, as manufacturers are struggling with material shortages and in in Asia with Covid outbreaks that shut down factories for weeks at a time.

And stimulus-fueled demand in the US has been huge and relentless, while retailers are struggling with inventories, some more than others.

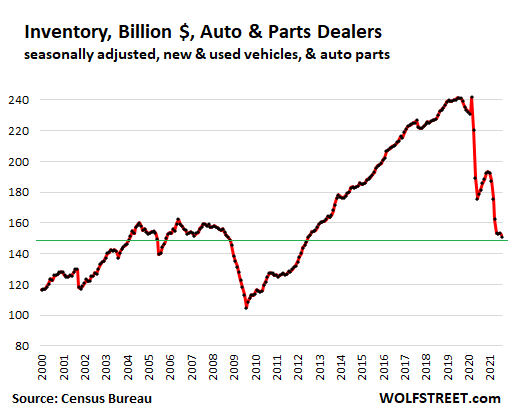

Catastrophic shortages at auto dealers got even worse.

Auto dealers, particularly new-vehicle dealers, are experiencing catastrophic shortages of popular models, as automakers have been getting blasted by semiconductor shortages that simply refuse to abate, leading to rotating shutdowns of assembly plants globally.

Auto dealers are the largest retailer segment, with their sales normally accounting for over 20% of total retail sales, and with their inventories normally accounting for 33% of total retail inventories.

Inventories at auto dealers, measured in dollars, declined to a new multi-year low of $151 billion in August, according to data released by the Commerce Department on Friday.

The long-term dollar-increase in inventory levels that you can see in the chart above is a reflection of higher costs per vehicle in inventory. But the number of vehicles in inventory has been in the same range for two decades, as unit sales have mostly been below the peak achieved in the year 2000.

It’s even worse during the current shortages: Inventory in dollars – though it collapsed – is being inflated by the shift to high-end models as automakers are prioritizing the biggest money makers.

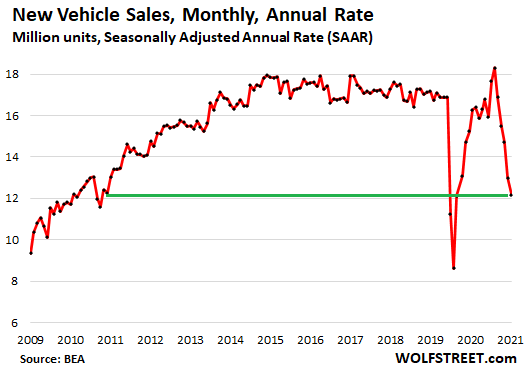

Sales of new and used vehicles also collapsed as there hasn’t been enough to sell. The industry-standard Seasonally Adjusted Annual Rate (SAAR) of sales plunged five months in a row and is down by 33% from May:

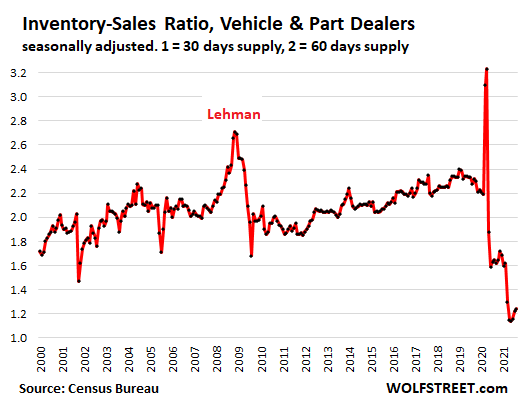

And so the inventory-sales ratio – inventories divided by sales, a standard metric of supply that cancels out the impact of price increases – has been ticking up over the past three months from the May low, which had been the lowest in the data going back to 1992. The upticks were driven by sales that collapsed even faster than inventories:

Following the Lehman bankruptcy, new vehicle sales plunged, and the US was suddenly drowning in inventory, and the inventory-sales ratio spiked.

During the pandemic, the opposite occurred: Fueled by huge amounts of fiscal and monetary stimulus, retail demand surged and collided with production woes due at first to Covid issues and then the semiconductor shortage. And prices have spiked, with many new vehicles being sold at prices well above sticker, which is nuts.

Tight inventories at food and beverage stores.

The empty-shelves syndrome of the spring 2020 is largely gone though there are surprising shortages of weird stuff here and there that you didn’t think a supermarket would ever run out of.

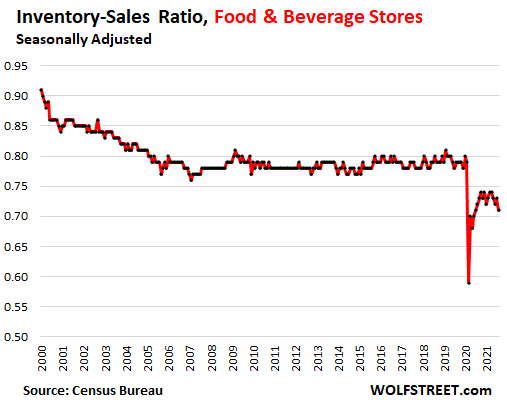

Retail sales at supermarkets remain at lofty levels, well above pre-pandemic levels, as consumption has shifted from the workplace and restaurants around the workplace to the supermarket. Food and beverage stores have increased their stocks, and prices have increased too, and in dollar terms, inventories rose to a record $54.5 billion in July and remained at the level in August.

But sales at Food and Beverage Stores in August and September were up 20% from two years ago while inventories in dollar terms were up only 6%. And the inventory-sales ratio fell further, to 0.71, the lowest since June 2020. This shows that supermarkets, while benefiting from the surge in sales, are having trouble with their supply chains as well:

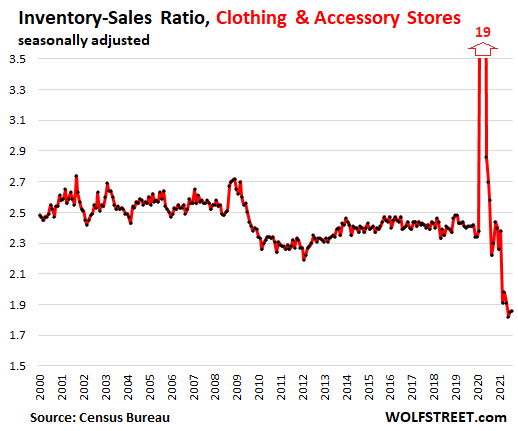

Clothing and accessory stores, record low supply.

When sales collapsed in March and April 2020, as many stores were locked down, unsold inventory piled up to a record $54 billion, and with few sales, the inventory-sales ratio spiked off the chart “literally” to 19 during that time.

But clothing sales recovered and then surged to new records, and were up 17% last month, from two years ago, and they ate up the excess inventory, and supply issues have worsened with some factories in Asia cycling through periodic shutdowns due to Covid.

In dollar terms, inventories have been stuck near the pandemic low, in August at $48 billion, same as in July. But the boom in sales caused the inventory-sales ratio and supply to plunge to record lows:

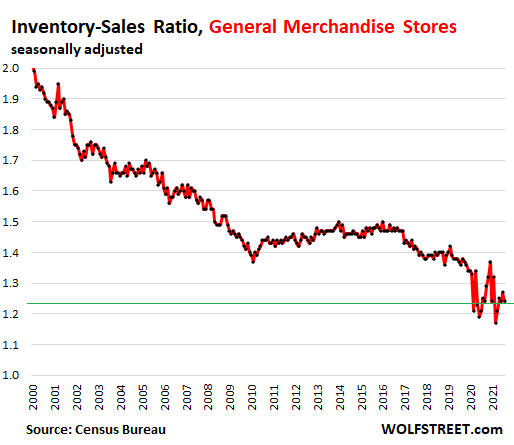

General merchandise stores, supply near record lows amid spike in sales.

Walmart, Costco, Target, Macy’s, etc. are in this category. Inventories in dollar terms, after the empty-shelves moment in the spring last year, rebounded and then continued to rise, and in August hit a new record of $87.2 billion, up 6% from two years ago.

But sales at these stores were up 23% from two years ago, which left the inventory-sales ratio near record lows.

Ever tighter inventory control and just-in-time delivery have slashed supply from 60 days in 2000 (inventory-sales ratio = 2) to about 42 days in 2018, 40 days in 2019. In August, supply was down to about 37 days:

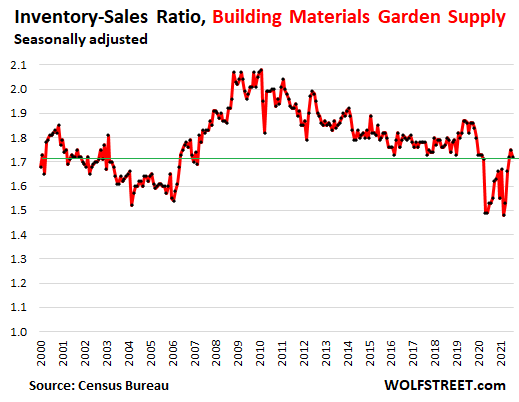

Building materials and garden supply stores.

In dollar terms, inventories spiked to a new record in July and remained roughly at that level in August, at $67 billion. Sales at these stores spiked during the pandemic, but in recent months has started to back off and in August and September were down 10% from March, but were still up by 23% from two years ago!

These gyrations in sales – the huge spike and now the drop-off to still very high levels – are part of what caused the inventory-sales ratio to move erratically. But in August, the ratio was nearly back in the normal-ish range:

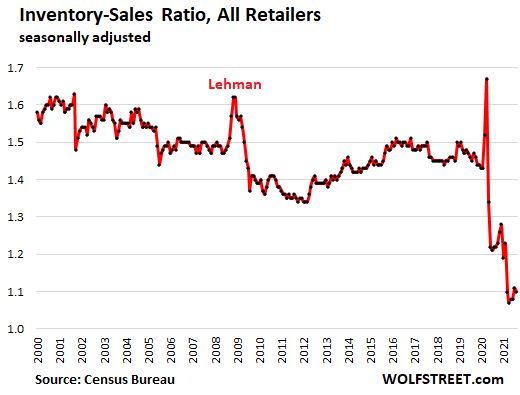

All retailers combined.

In dollar terms, inventories at all retailers in August, at $603 billion, were down 9.1% from two years ago, but total retail sales were up 18% over the same period. These far higher sales and lower inventories in dollar terms caused the inventory-sales ratio to plunge to 1.1 in August, roughly 33 days of supply, relentlessly stuck in the same range of all-time record lows:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter October 17th, 2021

Posted In: Wolf Street

Next: Living in a Potemkin World »