ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

May 16, 2021 | The Credit Card Hustle by the Banks & the Fed Hits Rough Spot

Wolf Richter

There has been a lot of commotion in banking and at the Fed about Americans having the temerity to pay down their credit cards – practically an abuse of stimulus, so to speak. In the five quarters since Q4 2019, Americans have paid down their credit card balances by $157 billion. “One of the most confounding changes in debt balances,” the New York Fed called it. Credit cards are immensely profitable for banks. The Fed has been repressing interest rates with all its might, but credit card interest has remained astonishingly high.

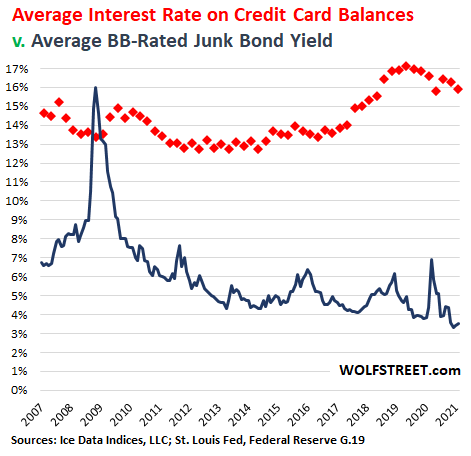

According to the most recent data from the Federal Reserve, banks charged on average 15.9% interest on credit card balances that were actually assessed interest. This is down 1.2 percentage points from the record in May 2019 (17.1%), but way above historic levels (red squares in the chart below).

By comparison, the average yield of BB-rated corporate bonds, the upper end of the junk-bond range (my cheat sheet for corporate credit ratings) has dropped to a record low of 3.2% in February, according to the ICE BofA BB US High Yield Index, and has barely ticked up since then (black line). In terms of making money off consumers that are in debt and that have run out of options, there is nothing like it out there:

Based on the average interest rate charged on credit card balances of 15.9%, that pay-down of $157 billion in credit card balances that consumers somehow engineered represents $25 billion a year in lost interest income for the banks!

That’s why banks are trying so hard to get consumers to borrow on their credit cards again. And that’s why the New York Fed, which is owned by the financial institutions in its district, finds that pay-down so “confounding.” We’re talking about $25 billion a year in banking income here.

The bank gets a fee from the merchant each time a consumer buys something with a credit card. The bank also collects interest from those consumers that carry balances on their credit cards and don’t pay them off every month. It’s this second part of the equation we’re talking about here.

The interest rate can be over 30% for consumers that cannot pay off their credit cards. If they had enough cash to pay off their credit cards at this rate, they would. But they’re stuck. Consumers that pay off their credit cards every month are often offered lower interest rates, but they don’t need to borrow on their credit cards. Banks also offer teaser rates of 0%, and then after a set period – after the consumer charged up the credit card and can no longer pay it off and is thereby stuck – the teaser rate switches to 29.9%.

Call it the credit card hustle.

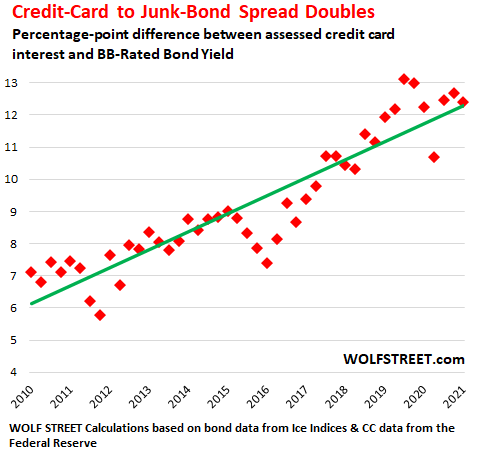

In the world of debt, “spreads” measure investor appetite for credit risk. The spread can be measured as the difference in yield between a category of corporate bonds, such as A-rated investment-grade bonds (relatively small risk of default) to Treasury securities of equivalent maturity (near-zero risk of default because the Fed can print the government out of trouble).

These spreads between higher-risk debts and lower-risk debts have narrowed and currently are near record lows. The exception is credit card interest.

For example, the spread between BB-rated junk bond yields (high-risk corporate debt) and credit card interest (high-risk consumer debt) has widened, and over the past decade has doubled, from a difference of around 6 percentage points on average in 2010/2011 to over 12 percentage points currently.

The average BB-rated bond yield has dropped from around 7% in 2010 to 3.3% on average in early 2021. The average credit cards interest rate on balances with assessed interest has risen over the same period from around 14% on average to 16%. Hence the widening spread:

Credit cards have been carefully shielded from the Fed’s interest rate repression. That profit center is just too important for the banks.

Using a credit card to get 2% cash back or accumulate frequent flyer miles or whatever is a smart thing to do, as long as you don’t have to pay interest on the balance.

But paying off those credit cards and not having to pay the usurious interest rates is a vastly smarter thing to do. Maybe Americans are finally getting smart about the credit card hustle – hence the $157 billion pay-down.

Credit card interest will always be higher than mortgage interest because credit card debt is unsecured debt, while mortgages are secured debt. So for banks, credit cards entail bigger risks, and interest needs to make up for that risk. But not the kind of interest being charged by banks for credit cards.

The credit card hustle entails this element: When a bank charges 25% interest on a credit card, the high interest expense increases the risk of default because the borrower is unlikely to not be able to pay for the interest. Charging 4% interest would cut the default risk by a huge amount. But that wouldn’t be part of the credit card hustle.

The irony is that the Fed has tried hard to repress yields on corporate debt. It is furiously repressing mortgage rates, including by buying mortgage-backed securities. It has forced down the interest rates that all types of borrowers have to pay. The Fed has moved heaven and earth to wipe out the income streams for savers and bond investors.

But at the same time, the Fed is flagellating its arms to get Americans to borrow more on their credit cards and pay this usurious interest. And instead of applying pressure to lower the interest rates banks charge on credit cards, the Fed gets upset when consumers are starting to react to the credit card hustle by paying down the amounts they owe. But for now the Fed is assuming that this is just temporary.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter May 16th, 2021

Posted In: Wolf Street