ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 2, 2020 | The Inevitable

Garth Turner

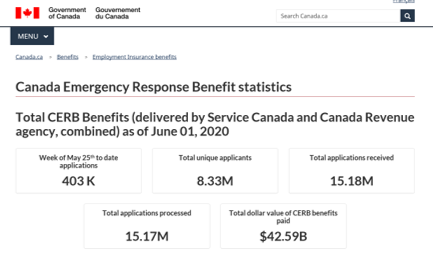

A year ago it looked like the guys running Canada would spend $20 billion more than they raised. Not good. Now that’s $252 billion more. Ooops, wait. We forgot the emergency money to cities, off-reservation native folks, pregnant women and… well… you know. Plus what happens when the CERB ends and a few million people are jobless but can’t live on their EI?

Odds are the deficit will be $300 billion, or six times the worst Harper year. That would increase the federal debt by half. In one year. A record. And still there’ll be an army of unemployed and many shuttered businesses. Revenues will fall. Social spending will rise. If the Trudeau gang decides we need a UBI, it all gets a lot worse. Meanwhile – OMG, Becky – look at this…

Where does it end?

With taxes, of course. The need for cash will be insatiable. And enduring. Some believe we’ve crossed the Rubicon, thanks to this virus. Now we all get a pony.

Well, this is a profound problem. These days four in ten households pay no net federal income tax, thanks to benefits like the cash-for-kids program. That leaves the other six to fund it all. But most of them (90%) earn less than $81,000. Hmm, so the top 10% of us – anybody earning $96,000 or more – currently bring in a little more than a third of all the income but already pay 54% of all the taxes.

Let me repeat. Ten per cent of Canadians pay 54% of the income tax. Of those, just a sliver are ‘rich’. The top 1% (earning $235,000 or more) number only 271,000. (Of those, 120,000 live in Ontario.)

This is why ‘taxing the rich’ won’t work. We don’t have enough to milk. Already the top tax bracket is 54% in a majority of provinces, while the few uber-wealthy families with billions have most of that money invested in businesses employing hundreds of thousands.

However most little beavers don’t know this. Or believe it. And now that the government just found $250 billion under the couch to give away during a crisis, there’s a giant expectation income support programs should stay in place, and ‘the working wealthy’ should finance them. In order to retain power, the prime minister (inheritor of a trust fund) and the finance guy (inheritor of a family business) plus his wife (inheritor of a food empire) agree. So bend over.

If you’re unfortunate enough to earn a few hundred thousand or have a couple of million in assets there will be an illicit group hug behind my bank building at four. Be there. Be strong. In the meantime, and in anticipation of what the next budget may well bring, consider this…

Capital gains. If there was ever an excuse for the feds to goose the inclusion rate, it came with the virus. Currently half the profit made on investment assets (properties as well as ETFs or stocks etc.) is taxed as income. That reduces the maximum capital gains tax to about 26%. T2 may give in to yet another NDP demand, and increase inclusion to 75%. The effective tax rate would be 40% – a huge jump.

Solution: you might wish to crystalize some accrued cap gains this year. Before the deluge.

Retained earnings. Despite all the yadda-yadda, we-love-small-biz talk from the feds, they actually hate you. Especially those entrepreneurs and professionals using corporations to earn income, distribute dividends and retain earnings in a lower-taxed environment. Two years ago Bill Morneau launched an attack on PCs, backed off under negative pressure, but is likely to reengage. So expect the threshold to fall on the amount of passive income a corp can earn before hitting the tax wall.

Solution: take salary, not dividends to max out RRSP contribution room. Repay after-tax shareholder loans, borrow money from the corporation, use the funds to expand or find other means to drain capital before fed fingers filch it.

New tax bracket: Remember when Trudeau created a special hoovering for people earning over $220,000? He said the money would pay for a middle-class tax cut equaling $8 per family (on average). It didn’t. But he will try again. Accountants that I skydive and luge with tell me they expect yet another bracket to emerge from the budget – somewhere around the $650,000 mark, which is what 0.01%ers average. Unfortunately there are only 27,000 of them, and they all read this blog.

Solution: Time to look at establishing a family trust and shifting investment income to less-taxed offspring. Also consider a hefty spousal loan, moving capital into the hands of a less-taxed partner so s/he can earn investment returns that won’t be attributed to you (plus deductible interest). Proper estate planning is a must, with secondary and tertiary wills if you have multiple assets (and your province permits them), proper beneficiary and successor-holder designations, a trust structure and an institutional executor.

Or, the Libs could just be fair about things and increase the GST. Tax spending rather than gutting income. Combine that with a flat tax and give everyone a condo. How is any of that hard?

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Garth Turner June 2nd, 2020

Posted In: The Greater Fool

Next: Conspiracies Behind the Curtain »